Caffeinated Memos: Extreme Networking

An "extreme" set-up in the Wi-Fi refresh cycle

Welcome back to the Caffeinated Memos series. Prior memos have a median 14% three-month return and 27% six-month return.

Previously we discussed Nokia and how it will be a beneficiary of rising data demand as traffic moves from within the data center to the edge. Today’s memo is on another company benefitting from this dynamic, but in a sleepier part of the networking space that the market is just now starting to appreciate.

That niche? Enterprise Wi-Fi.

Think of hospitals, universities, stadiums, and corporate campuses that rely on seamless and secure connectivity across their physical footprint.

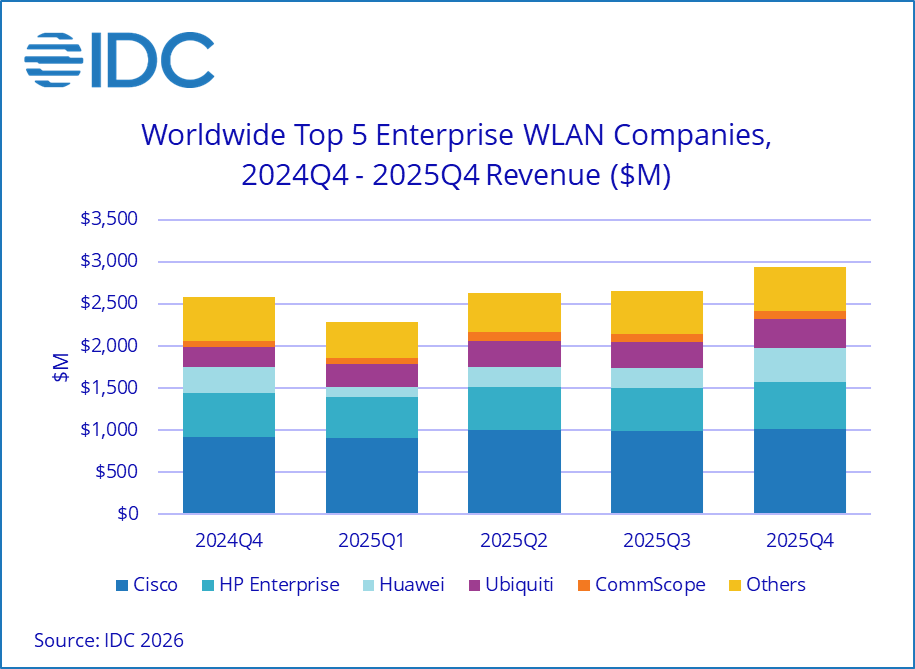

Cisco is the giant in the industry, with HPE Aruba as the distant second. Internationally, Huawei has a large presence.

Wi-Fi access points are typically seen as a commodity. Firms have built Wi-Fi into a profitable business by bundling it alongside Ethernet switches, support, and security in a platform strategy. Wi-Fi is seen as a cyclical profitable business but not exactly a “growth market.”

That’s starting to change. During its earnings call last week, Cisco reported its “highest ever wireless orders,” growing more than 40% year over year.

Within the wireless segment, Cisco disclosed that Wi-Fi was the key growth driver:

“Customers are upgrading to modern Wi-Fi evidenced by strong double digit sequential growth in orders for Wi-Fi 7 making up half of the wireless mix in Q3. Research conducted recently with around 3500 technology leaders across global enterprises confirms increased urgency to modernize campus and branch networks, with traffic across these networks expected to increase 3x over the next three years because of AI, 93% of respondents are accelerating their network modernization plans. These findings support our belief that we are still at the start of a multiyear, multibillion dollar campus refresh opportunity.” [CSCO Q3 26]

A multibillion dollar campus refresh opportunity driven by AI data demand? That sounds like a catalyst.

The problem is Cisco is an almost $500 billion company diversified across multiple segments, including networking, security, collaboration, and observability.

But what if there were a roughly $3 billion company much more directly exposed to enterprise campus networking and the Wi-Fi upgrade cycle?

And what if that company also had:

Double-digit revenue growth

60%+ gross margins

20%+ return on invested capital

A shift toward recurring revenue

Management claiming wins against Cisco, HPE Aruba, and Huawei;

And despite the recent move, is trading below 20x FY27E earnings?

Introducing Extreme Networks

Extreme Networks ($EXTR) is a small-cap that focuses exclusively on enterprise networking.

The company originally went public in 1999, near the peak of the original networking boom.

Today, Extreme sells two main types of access infrastructure products:

Universal switches: support traditional Ethernet networking or fabric-based networking

Universal Wi-Fi: Access points for campus and distributed deployments.

Sitting above the hardware layer, the Platform ONE subscription adds AI-driven network insights, asset management, usage analytics, and zero-trust security.

Financial Momentum

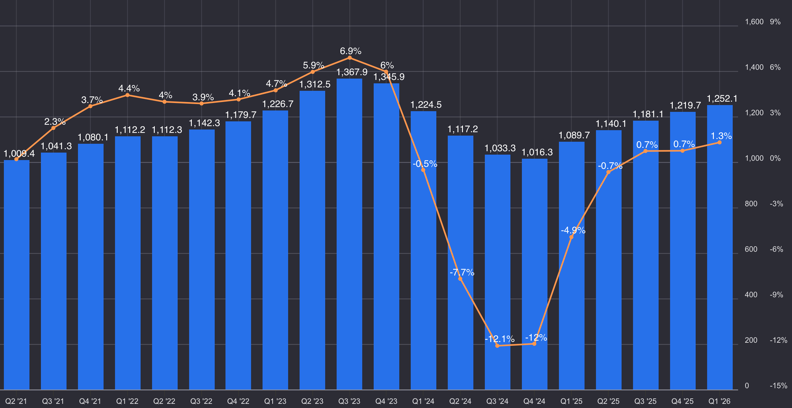

Extreme has delivered five consecutive quarters of double-digit year-over-year revenue growth.

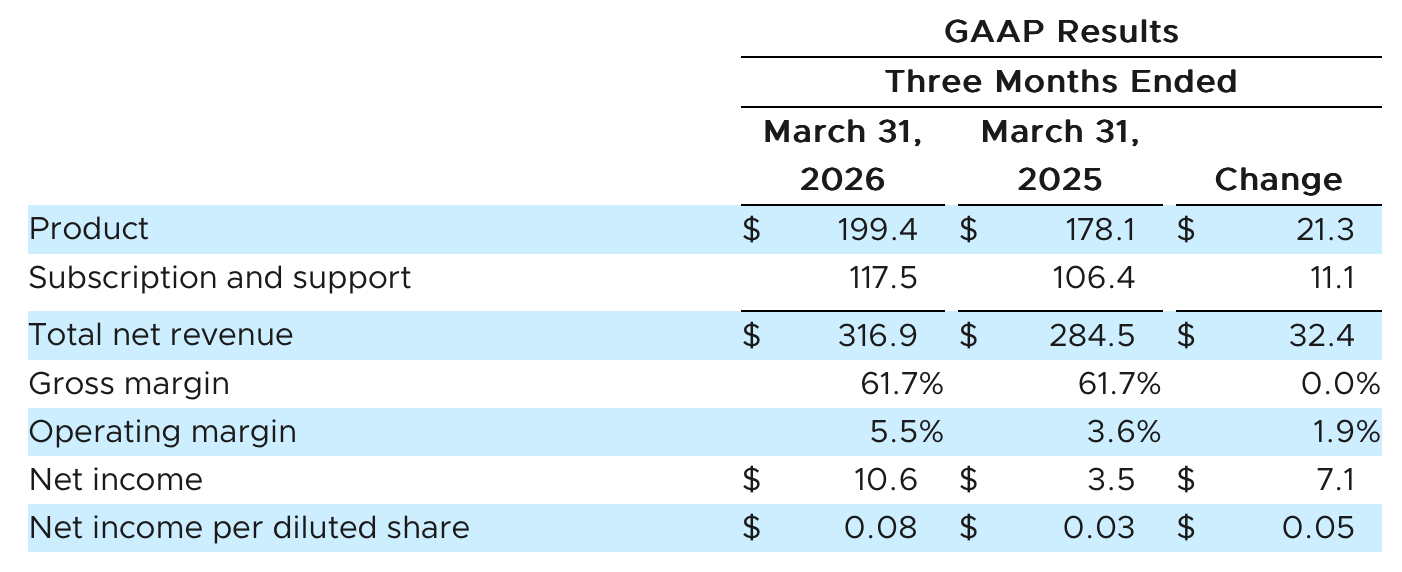

In Q3 earnings reported on 4/29, product revenue, the hardware side of the business grew 12% YoY. Subscription/support revenue grew 10%.

Gross margin held steady at 61.7%, while operating margin improved from 3.6% to 5.5%. Additionally, management is seeing progress in its license-to-SaaS transition. SaaS ARR was $236.4 million, up 28.6% year-over-year, outpacing the overall subscription/support segment’s 10% growth.

Revenue is growing double-digits, gross margins are stable, and operating margins are improving. The guide for next quarter points to further improvement.

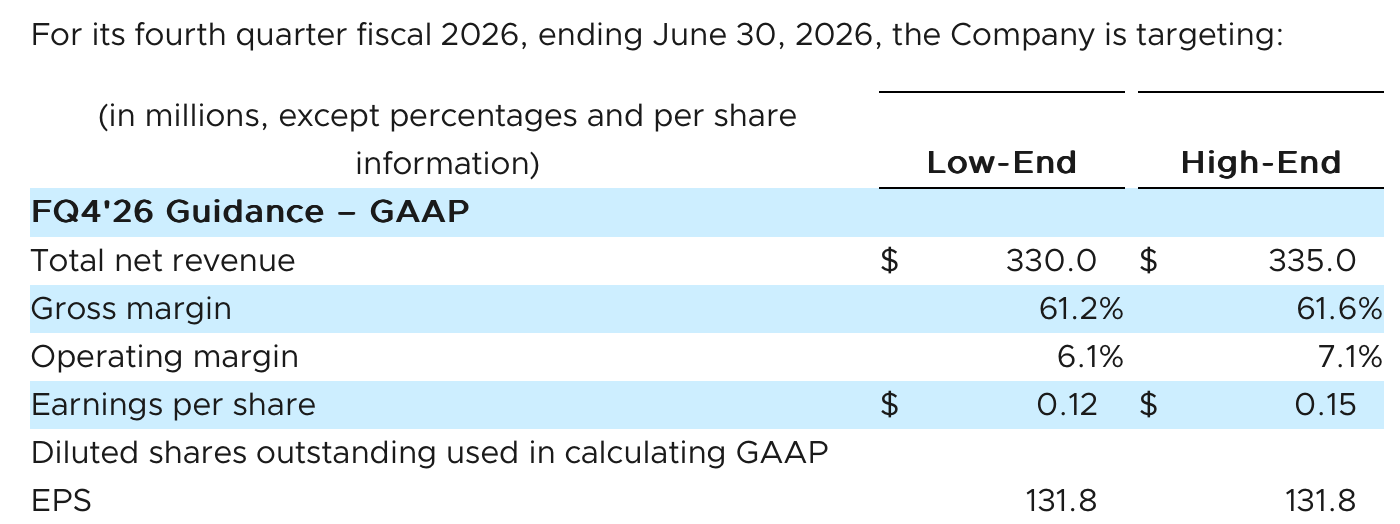

Management guided to $330–335 million of revenue, implying roughly 4–6% sequential growth, with operating margin improving further to 6.1–7.1%.

This is the financial setup investors want to see from a hybrid hardware/software vendor: product revenue is growing, recurring revenue is scaling, and operating margins are improving off a low base.

As hardware sales grow, Extreme also expands the future base for recurring revenue. Every new managed device creates an opportunity for additional software and support licenses, adding operating leverage into the business.

So the key question is: why is a company that has been public since 1999 suddenly delivering consistent double-digit product growth?

It’s the same reason Cisco saw a 40% increase in wireless orders: Wi-Fi 7

The Wi-Fi 7 Demand is Real

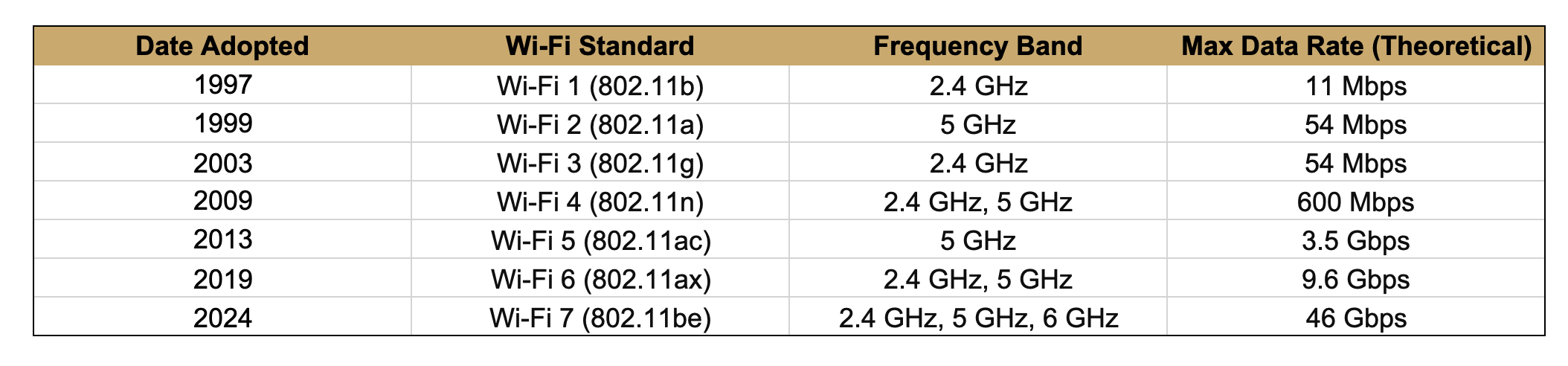

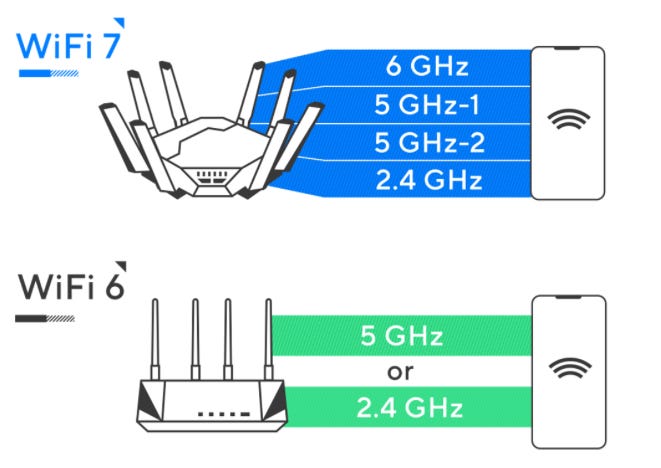

Wi-Fi 7 is the latest standard for wireless connectivity, adopted in 2024. Like the previous standards, it uses radio frequencies to support connections.

At a high level, Wi-Fi 7 can support theoretical speeds up to 46 Gbps, 4x the previous generation, and 320 MHz bandwidth, 2x the previous generation.

Wi-Fi 7 uses the 6 GHz band more effectively, enabling higher speed connections. But the real technical breakthrough is Multi-Link Operation.

In the prior Wi-Fi generations, a device connected to one band at a time: either the slower 2.4 GHz band or the faster 5 GHz band. Wi-Fi 7 allows devices to connect across multiple bands at once. This means devices can use multiple bands simultaneously for better reliability.

The Wireless Broadband Alliance found Wi-Fi 7 delivered improved real-world performance:

At 6 GHz with 160 MHz channels, Wi-Fi 7 achieved nearly 2 Gbps downlink throughput at close range, maintaining over 1 Gbps up to 40 feet away. In high-density enterprise settings, where access points must support thousands of simultaneous connections, Wi-Fi 7’s enhanced spectral efficiency and Multi-Link Operation (MLO) provided more stable, reliable connectivity, mitigating network congestion even in heavily loaded conditions.

1 GBps+ speeds 40 feet away from the access point in real world usage is impressive.

Wi-Fi 7 is quickly becoming the main industry driver. IDC data found Wi-Fi 7 accounted for 39.7% of access point revenue in 4Q25 up from 10.25% a year earlier. The IDC also expects “Wi-Fi 7 adoption is likely to accelerate further […] as organizations pursue higher performance, greater automation, and tighter integration with AI-driven and distributed workloads.”

In addition to Cisco, HPE Aruba is seeing the demand: “The Wi-Fi 7 transition is ramping quickly. We saw more than 10x increase in Wi-Fi 7 access points sold” [HPE Q1 26].

Dell’Oro sees the same signals. The research firm predicts Wi-Fi 7 will be adopted by “over 90 percent of the market,” that “revenue growth will continue for another 3 years,” and the rate of adoption will be the fastest since “Wi-Fi 4 in 2013.” Importantly for Extreme’s narrative, “software revenues are expected to increase faster than the total market.”

Extreme is already seeing the cycle in its own results. On the Q3 call, management said Wi-Fi 7 represented “37% of total wireless unit shipments,” up from 27% last quarter and nearly half of wireless bookings came from Wi-Fi 7. Management said Wi-Fi 7 continues to “drive higher selling prices and gross margin” [EXTR Q3 26].

While the demand inflection is clear, there is also a supply-side wrinkle.

Dell’Oro has warned that the DDR4 memory shortage could carry over to access points:

The AI build-out has caused a shortage in DDR4 memory, required in most modern WLAN Access Points. We expect prices to rise as supply tightens, and if constraints deteriorate further, equipment lead times could grow and prices could escalate.

On its earnings call, Extreme management said it has “secured our supply chain, including our memory supply, through fiscal 2027 and beyond,” putting the company in a position to benefit if the component shortage worsens.

The Wi-Fi 7 demand signal is confirmed across Cisco, IDC, HPE Aruba, Dell’Oro, and Extreme’s own bookings. The cycle is real, but is Extreme ready to win?

Extreme’s Playbook: Real Customer Wins, Focused Positioning

Extreme is much smaller than Cisco or HPE Aruba. It does not have Cisco’s installed base, balance sheet, channel scale, or full-stack enterprise platform.

When asked who Extreme was winning against, CEO Ed Meyercord said:

In all of the examples that we put in our press releases, it really reflects wins against virtually all of our competitors. When we say that, obviously number one is Cisco […] Number two… being HPE Juniper. [EXTR Q3 2026]

The latest quarter included real customer examples:

“Extreme supported Lucas Oil Stadium in Indianapolis for the NCAA Men’s Final Four and rapidly modernized connectivity by removing legacy access points”

“Extreme continues to gain share within the UK National Health Service, with a new win at South London and Maudsley NHS Foundation Trust, where Extreme displaced a larger Chinese competitor.”

Other wins included London Business School, the Carolina Hurricanes, and Asiana Airlines, along with supporting “mission-critical systems” at the Kennedy Space Center during the Artemis II mission.

These are not random customers but name brand schools, stadiums, and government agencies. So why are customers choosing Extreme?

The answer is that Extreme has identified a wedge against Cisco and HPE Aruba: faster deployment, simpler operations, and the flexibility to modernize the campus network without forcing customers into a full-stack platform bundle.

Over the last year, Cisco debuted its Unified Edge Platform. Cisco describes the bundle as bringing together “compute, networking, security, storage, and software to run AI applications at the edge.”

That pitch will resonate with some customers. But not every customer is looking to buy compute, storage, security, and software as part of a campus refresh or wants Cisco to own the entire stack. Some just want the Wi-Fi 7 upgrade.

Extreme CEO Ed Meyercord argued in the call:

“Cisco continues to grow and expand outside the networking market, and I would say, you know, simply focus on other things. That opens the door for us. The new comp plan for partners require them to jump through hoops and sell things that they normally don’t sell.” [EXTR Q3]

Extreme’s proposition is simpler. Customers come to Extreme for the campus networking problem they actually need solved. Then customers adopt subscriptions on their own merits rather than being pushed into a bundle at the start.

Customers can choose public cloud, private cloud, or on-premise management. Customers can also buy licenses in ways that fit their procurement model from buying an initial pool of licenses at a fixed price or subscription tiers with the ability to grow over time.

Extreme also highlights license portability: “one portable management license for any device and for any type of management.” For a customer, that means subscription billing is straightforward.

This is a classic focused competitor strategy. As Michael Porter wrote in Competitive Advantage, “the focuser selects a segment or group of segments in the industry and tailors its strategy to serving them to the exclusion of others.”

Extreme is not trying to win every customer. It is trying to win the customers who want campus networking simplicity rather than a full-stack bundle.

Over the years, Extreme has acquired legacy IP assets from Avaya (formerly Nortel), Brocade (Broadcom), and Zebra Technologies. So while it does not have the same R&D budget as a Cisco or HPE, Extreme has been able to stay close to the technical frontier as far as access points go.

Valuation, Price Target, and Risks:

The business momentum is too obvious for the market ignore at this point. It is unsurprising that the Extreme is up 50% YTD and 35% over the last month.

This is not a “cheap on current earnings” pitch. Extreme is currently at a ~200 trailing PE. This is a bit misleading as it is coming off a cyclical low

Still, even with a recovery to the 2023 peak, Extreme is at 34x that level of earnings, which is not cheap.

So why is it still attractive?

The cycle may be underestimated

For Extreme Networks to work, this cycle would have to be better than the last one. Why would it not be?

The prior cycle was driven by supply chain shortages, not demand. As IDC described the industry dynamic at the time:

Recent quarters in the WLAN industry have seen outsized growth rates, driven by vendors drawing down a record high backlog of product orders as supply chain and product availabilities normalize.

Customers had ordered too much during COVID, calibrated to hybrid and remote work demand. Due to supply chain constraints for networking equipment, those orders were not fully fulfilled until 2023. Vendors like Extreme showed strong growth but it was the result of clearing their backlogs.

This cycle is different. Demand is driving it, with the Wi-Fi 7 refresh leading the way. Extreme is already approaching its prior revenue high, but the cycle appears closer to its beginning than its end. Dell’Oro said WLAN revenue growth can continue for “another three years.” IDC expects Wi-Fi 7 adoption to “accelerate further.” Cisco called campus refresh a “multiyear opportunity.”

If those forecasts are directionally right, FY27 consensus may not represent peak earnings. The true peak could be closer to FY29.

Share gain narrative still has room

Extreme has won name-brand customers, but many of the visible examples so far are in education, healthcare, sports, and public-sector environments. These wins matter, but the next validation step would be a large Fortune 1000 enterprise campus win that more directly proves management’s claim that Extreme is taking share from Cisco and HPE Aruba.

At Extreme’s scale, even a handful of large enterprise campus wins can move the model. A $5–10 million deployment is immaterial to Cisco, but can move revenue by over 1% for Extreme. Kroger is already a customer with 10,000 access points, though not in a traditional enterprise setting.

By the time those share gains show up cleanly in industry-wide data, the stock may already have rerated further.

Platform ONE is becoming an AI software story

Extreme has already had “AI analytics” inside its cloud platform. The May 5th announcement of Extreme Agent ONE pushes the software story further.

Agent ONE Operator will execute tasks independently within defined governance boundaries, responding to events in real time and monitoring networks: “even when IT teams are not actively engaged.” By automating IT labor (or just night shifts), Extreme has room to increase the importance of its value-added services.

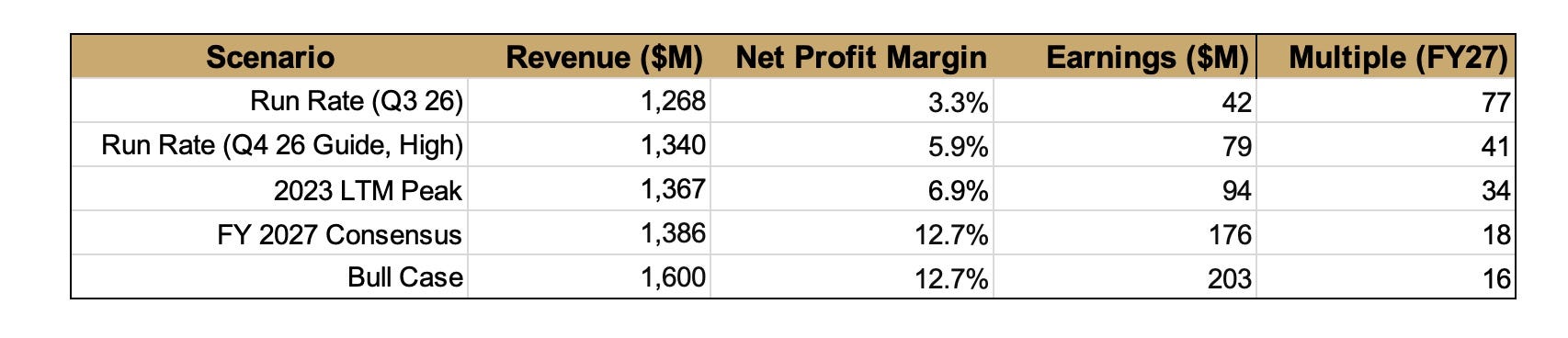

Price target: $31.50-34.25, based on a 23–25x multiple on FY27E GAAP EPS of $1.37. At ~$25, EXTR trades around 18x FY27E GAAP EPS.

The path to the target is straightforward but requires execution. Revenue needs to move past the 2023 high of roughly $1.3B, operating leverage needs to continue, and the market needs to view FY27 earnings as a base rather than a peak. Management is already guiding to further margin expansion next quarter, and continued SaaS improvement gives the business a chance to be treated as stickier than a pure hardware-cycle name.

A 23–25x multiple is a modest premium to the market for a double-digit grower, but getting there requires share gains to continue and for Platform ONE / Agent ONE to drive further recurring revenue.

Timeline: Cisco’s earnings call already kicked off the narrative last week, driving an 8% gain for EXTR last Thursday. Management will aim to keep the momentum going as it presents at JPM this morning at 11:45am ET. After that, B. Riley (May 20), Evercore (June 2), and BofA (June 3) will give management three more opportunities to drive the narrative over the next three weeks. Look for next quarter’s earnings for additional confirmation of the thesis.

Risks:

The cycle proves shorter than expected. Dell'Oro, IDC, and Cisco all point to a multi-year refresh, but demand could still be front-loaded.

Share gains remain anecdotal. Extreme has a clear strategy and real customer wins, but it has not meaningfully dented Cisco’s market share in industry-wide data.

SaaS growth slows. The bull case depends on hardware refreshes increasing the base for recurring software/support revenue. If growth slows, the business remains more cyclical.

Agent ONE disappoints. Agent ONE could remain more press release than product adoption. If it does not become part of IT workflows, Extreme will not get credit for a stickier AI software layer.

Supply chain reemerges as a constraint. Management says memory supply is secured through FY2027 and “beyond.” If shortages persist longer than management’s secured supply window, lead times or margins could become an issue. Extreme may be positioned if competitors are more exposed to tightening component supply.

Valuation is less forgiving after the move. The stock is already up sharply YTD. If FY27 estimates prove too high and earnings settle closer to prior-cycle levels, the stock could quickly look expensive again.

Disclosure: Author is long EXTR shares. Not investment advice - just ideas that seemed brilliant at 2am. Do your own research. Past results are not indicative of future results.