Caffeinated Memos #12: Nokia, AI at the Edge

Cell infra manufacturer Nokia is at the beginning of a cycle inflection with Nvidia investment and US-focused leadership

Welcome back to Caffeinated Memos, the financial newsletter covering short-term catalysts underappreciated by the market.

Today we’re covering Nokia (NYSE: $NOK). You may know Nokia as the Finnish tech giant that at one point made the world’s best selling phone.

Nokia today does not make any phones, having sold that business over a decade ago. Nokia instead operates in the telco infrastructure space, selling the radios, antennas, and signal processing that makes cell networks work. Nokia has thousands of patents for cell infrastructure, making it one of the most important companies worldwide for 5G infrastructure.

Nokia sells equipment to cell networks including T-Mobile (US), Telefonica (Europe), Softbank (Japan). The current industry expectation is that cell networks will slow spend on new equipment. Their 5G networks are mostly built out and 6G is years away with 6G standards not expected to be finalized until 2030.

Two near-term catalysts could disrupt the consensus narrative. An upcoming EU mandate will phase out existing Huawei equipment, boosting demand for 5G equipment in the short-term. Meanwhile, AI applications have the potential to dramatically increase data traffic on cellular networks, requiring 6G to be deployed ahead of schedule.

Nokia is well-positioned to be a leader in the 6G cycle with Nvidia backing ($1B investment), positioning towards US leadership, and a refocused business strategy under a fresh CEO.

Unlike other AI plays, Nokia is still an afterthought that is largely under-appreciated by the market and has plenty of room for earnings inflection.

Why is Nokia Relevant?

To compete in the cell infra space, there are significant barriers to entry. One has to have the patents for the radio frequencies and processing for effective cell equipment, in addition to network relationships and manufacturing.

Per congress,“To improve networks, operators purchase equipment from network equipment manufacturers. There are four major global network equipment makers: Chinese firm Huawei; Finnish firm Nokia; Swedish firm Ericsson; and Zhong Xing Telecommunication Equipment (ZTE), a Chinese firm that is partially state-owned.”

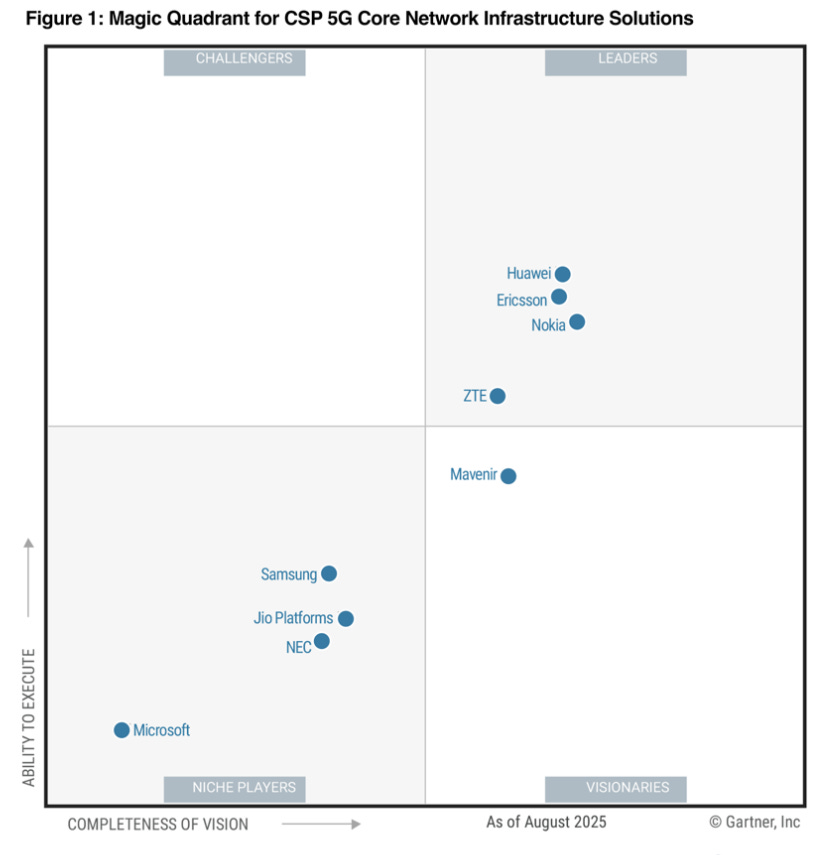

Huawei, Ericsson, and Nokia are near-parity for network solutions per Gartner.

While Huawei is the largest infrastructure player globally, Western countries are aligned on avoiding Huawei equipment due to past incidents of Chinese spying through cell networks. Due to this dynamic, Ericsson and Nokia are now an effective duopoly for western telco infrastructure, with the two companies roughly equal in scale and patents. This also creates significant pricing power during telco cycles.

Has Telco Capex Peaked?

There have been 3 major investment cycles for Telco infrastructure over the past 20 years, corresponding to the 3G, 4G, and 5G standards.

How do these standards come about? The International Telecommunications Union, a UN agency outlines targets for the next generation. 3GPP, an international consortium of industry representatives turns the targets into formal technical requirements. For 5G, commercial standards were agreed upon by 2020, kicking off a telco infra cycle.

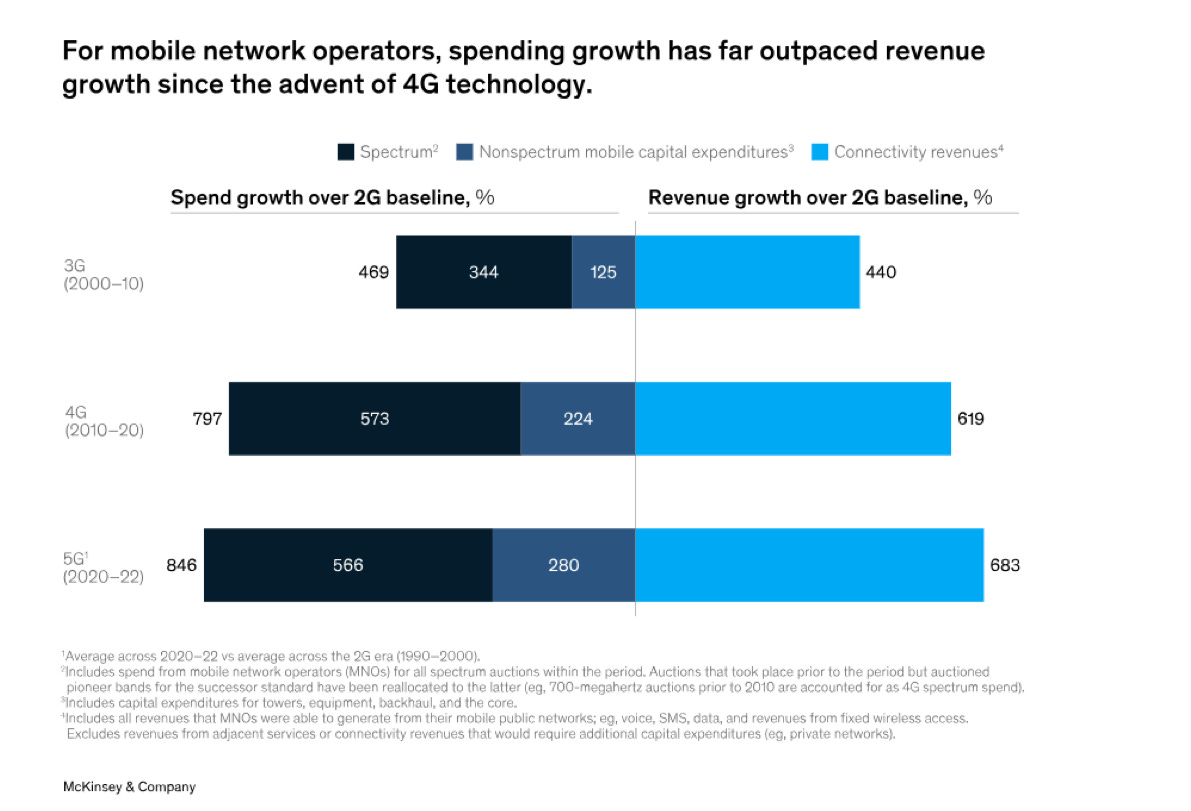

In each cycle, network operators have spent more than the previous one.

Network operators have built out most of their 5G coverage. 5G is now seen as “past the peak, but it is not falling off a cliff,” per the Dell ‘Oro group. Cell networks including Verizon are now boasting “continued CapEx efficiency”

Nokia is highly sensitive to these cycle dynamics.

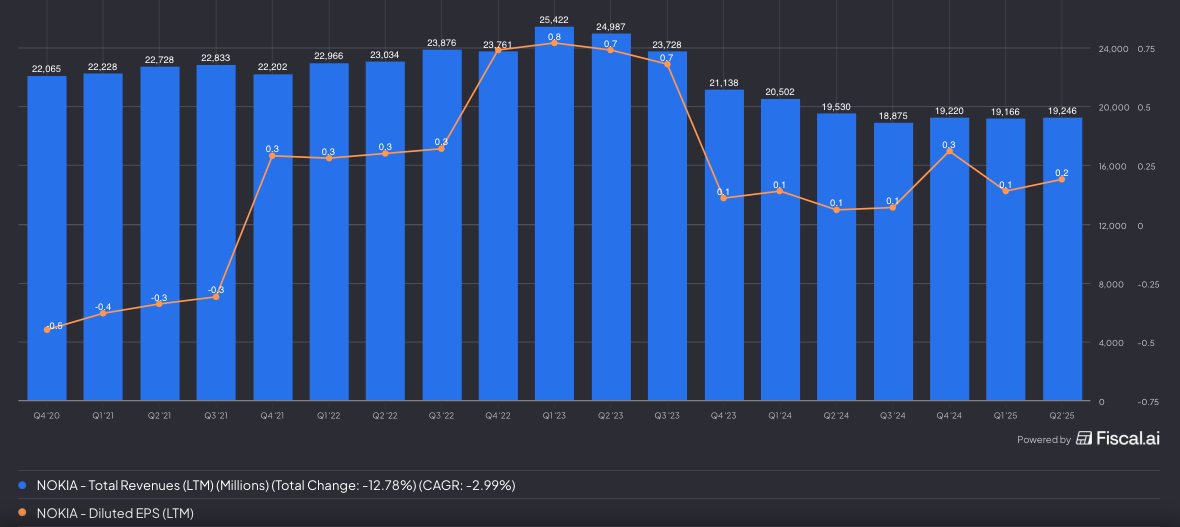

In the previous cycle, Nokia had peak TTM revenue of €25B and €0.8 EPS/share. Since then, revenue has declined to €19B with EPS in the €0.2 range.

This is also important from a valuation perspective. Nokia currently trades at 35x trailing earnings, which appears expensive until you realize this is through earnings. As each cell cycle is more capex intensive, Nokia can likely earn a peak €1 EPS, putting the stock at under 6x peak earnings potential.

So when does Capex inflect? Is it 5 years away? 2 years away? Deloitte is expecting telecoms through 2030 “to work to keep cutting costs, keep capital expenditures under control, monetize their past investments” as 5G matures. The consensus view is bearish on near-term capex.

Catalyst 1: EU Mandating Phase-Out of Chinese Equipment

On January 19th, the EU Commission proposed a new cybersecurity act (EU Cybersecurity Act 2.0). The initial proposal draft includes a full phase out of Chinese equipment.

While the EU initially recommended the removal of Huawei equipment in 2020, “only 13 of 27 [member countries] have so far acted on it, commission sources said. This marks the first time Brussels has attempted to make their removal mandatory.”

Under the proposal, EU countries would have 36 months to phase out their use of components provided by high-risk suppliers (China).

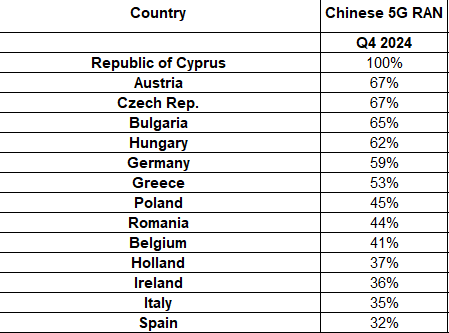

How big of a deal of this? Per Strand Consult, some of the largest EU countries were still buying Chinese 5G equipment in 2024. Countries like Germany, Italy, and Spain were buying 59%, 35%, and 32% of their 5G equipment from Chinese providers.

Now those same countries will have to tear out the existing Chinese equipment and replace it with Nokia or Ericsson.

This development is significant enough to disrupt the trajectory of the typical telco capex cycle and provide a material short-term boost to Nokia earnings.

Catalyst 2: AI Increasing Data Demand and Accelerating 6G Timeline

While the EU mandate provides near-term revenue improvements, AI is fundamentally changing the timeline and potential scale of the 6G investment cycle.

The Data Growth Debate

Cell network operators are currently expecting data growth to slow from the historical 30 percent to “10 percent across both fixed and mobile networks in the near future” (McKinsey). If data growth slows to 10%, there isn’t a huge incentive to launch a capex cycle before 2030.

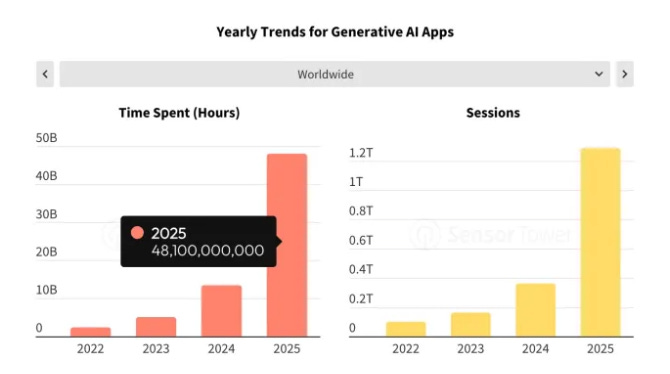

Cell equipment providers believe the 30% growth continues: Ciena CEO Gary Smith stated “Traffic growth has been between 20% and 40% per year very consistently for the last two decades” and AI investments ultimately translate to data usage: "It has to come out of the data center and onto the network.” Consumers spent 48 billion hours in AI apps in 2025 per SensorTower data.

Why AI Will Drive Cellular Traffic

Some analysts claim AI, despite clear usage trends, won’t drive capex growth: “many gen AI use cases for both consumer and enterprise markets are not exactly bandwidth hogs: In 2025, they tend to be text-based (so small file sizes) and users may expect answers in seconds rather than milliseconds”

But AI use cases are rapidly evolving past simple text. Low-latency voice mode, AI-generated video, and file uploads are becoming more popular and are far more intensive on cell networks.

More importantly, AI is expanding beyond phones. As Nvidia’s Ronnie Vasishta testified to congress: “Traditionally, telecommunications networks delivered voice, data, and video. In the future, mobile networks will also be called upon to support a new kind of traffic—AI traffic. AI traffic will include the delivery of AI services to the edge, or inferencing at the edge. Mobile networks will support applications such as autonomous vehicles, smart glasses, generative AI services on phones or devices, holographic communication services, collaborative robots, and many more applications that we haven’t thought about yet”

Why 6G is required

While it would be easy to dismiss Vasishta’s statement as hype, Nvidia is legitimately worried about a potential cellular bottleneck in AI adoption. Last October, Nvidia invested $1B in Nokia at $6.01 USD/share to develop “the AI platform for 6G”

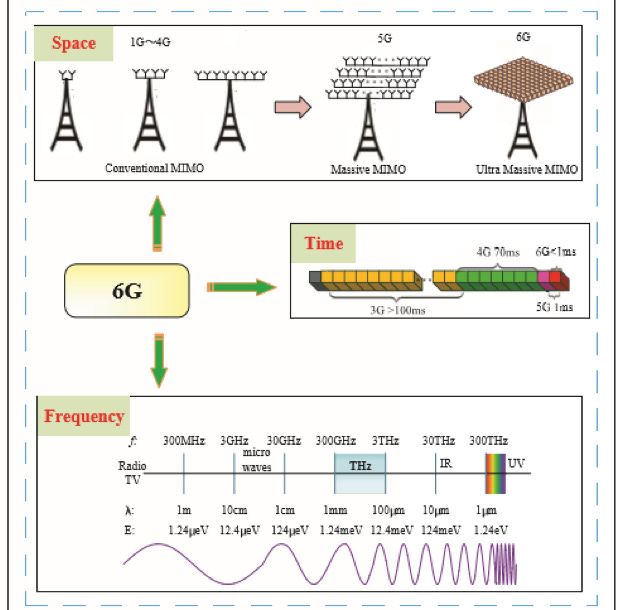

What is 6G ? At higher frequencies, it is possible to transmit data faster. As 5G moved up the frequency spectrum through massive radio antenna arrays, 6G will move even further up the spectrum with even larger antenna arrays.

At this scale the amount of data that has to be processed likely requires a GPU locally in the tower itself. Nvidia’s own data specs propose 6G will be a 20-100x improvement in data rate for the end user with speeds of up to 1 GB/s.

Nokia’s 6G Positioning and Accelerated Timeline

Nvidia has chosen Nokia as its core partner in 6G infrastructure before the 3GPP finalizes standards. Nvidia noted 6G standards are “quite far in the standardization process.” T-Mobile is already working with Nokia and Nvidia on a 6G trial implementation: “T-Mobile is one carrier that has recognized that and is working with Nokia and us on an AI-native implementation for 6G.”

It’s not just T-Mobile, with Softbank having extended an official partnership with Nokia.

With trials underway in 2026, and Nvidia pushing for U.S. 6G leadership with Nokia as its core network infra partner, we could see a 6G cycle develop in advance of official 6G standards, moving the capex cycle inflection from 2030-2031 to 2027-2028, pulling forward Nokia’s earnings inflection 2-3 years before consensus.

Improving Business Strategy and Focus

Beyond the two catalysts, new CEO Justin Hotard has been positioning the company to capitalize on the 6G cycle and AI while reducing non-core assets. Hotard, who became CEO in April 2025, brings a deep understanding of AI from his time as an executive VP at Hewlett Packard Enterprise where he delivered the “world’s first exascale supercomputer” for their HPC & AI lab.

Streamlining Operations

Hotard has reorganized Nokia under two core business units: Mobile Infrastructure (radio, software, and licensing) and Network Infrastructure (optical and broadband).

As part of this refocus, Nokia is divesting several non-core assets including Fixed Wireless Access CPE, Site Implementation and Outside Plant, Enterprise Campus Edge (currently in Cloud and Network Services), Microwave Radio (currently in Mobile Networks). These units generated EUR 0.9 billion in net sales with an operating loss of EUR 0.1 billion. Exiting these businesses will reduce operating expenses by €200 million by 2028.

US-Aligned Positioning

Perhaps most strategically, Hotard is positioning Nokia as the American-aligned infrastructure partner for the 6G era. Nokia is investing $500M in manufacturing and R&D across Texas, New Jersey, and Pennsylvania in addition to its already active broadband manufacturing in Wisconsin. The February 2025 acquisition of Infinera, an optical networking player with US manufacturing facilities, further solidifies this positioning and has already prompted analyst upgrades. Nokia also powers US military operations with private 5G infrastructure.

Combined with the Nvidia partnership, this US focus likely gives Nokia a competitive edge over Ericsson in winning American telecom business as the 6G cycle accelerates. As Hotard stated at Nokia’s Capital Markets Day: “As the trusted western provider of secure and advanced connectivity, our technology is powering the AI supercycle.” Hotard is uniquely positioned as an American CEO of a European company to win business on both sides of the Atlantic.

Financial Targets

Nokia is targeting €2.7-3.2 billion in comparable operating profit by 2028, up from €2.0 billion currently. The company expects 6-8% revenue growth in Network Infrastructure (with 10-12% growth in Optical and IP Networks specifically) and aims to expand Mobile Infrastructure gross margins to 48-50% by 2028. These targets reflect both the streamlined cost structure and Nokia’s positioning to capture growth in AI-driven infrastructure and the coming 6G cycle under Hotard’s technically focused leadership.

Price Target/Summary:

Nokia (NYSE: NOK) closed at $6.77 on Friday, January 25th. After initially running to $8+ following the Nvidia partnership announcement, the stock has pulled back and consolidated, creating an attractive entry point.

With peak earnings potential of €1+ per share, Nokia trades at under 6x normalized earnings power, a significant discount that reflects market skepticism about the telecom capex cycle. Nokia trades at 1.1x sales versus peer Ericsson at 1.3x, despite comparable positioning in the Western infrastructure duopoly and improving business momentum (Ericsson reported strong results last week).

The investment case rests on two distinct catalysts with different timeframes:

Near-Term (Next 3-6 months): The EU Cybersecurity Act 2.0, proposed January 19th, will move through the legislative process in 2026 and mandate removal of Chinese equipment from European networks. This will provide near-term revenue visibility and earnings support on forced replacement spending during what was expected to be a capex trough.

-Long-term (2-3 years): The Nvidia partnership and AI-driven data growth could accelerate 6G deployment from 2030-2031 to 2027-2028, pulling forward Nokia’s next major earnings cycle. With trials already underway and Nokia positioned as the US-aligned infrastructure partner, this represents the significant upside case.

Nokia reports Q4 earnings on January 29th. These catalysts support a price target of $9 (+30%) over the next 6-12 months as EU mandate clarity emerges, with further upside to $12 (+80%) as 6G deployment accelerates in 2027-2028.

Key risks:

Execution: While Hotard has proven his ability to strike partnerships, cutting out $200M in non-core expenses is a different skillset

Competitive dynamics with Ericsson: Ericsson is a formidable competitor. It’s not obvious who has the patent lead for 6G or if a third entrant is able to break through in the 6G environment (Samsung)

Geopolitical factors: The EU could re-welcome Huawei/ZTE under Beijing pressure as they’ve done for BYD subsidies. However, it is in the EU’s best interest to support Nokia and Ericsson as tech leaders

AI data use: AI could remain predominately a text-driven application, causing data use to grow below historical norms

Disclosure: Author is long NOK shares. Not investment advice - just ideas that seemed brilliant at 2am. Do your own research.

This piece really made me thnk, AI edge compute is wild.