Caffeinated Memos: Ultimate Precision

The company enabling the next generation of neurosurgery

Welcome back to the Caffeinated Memos series. Prior memos have a median 10% three-month return and 20% six-month return.

Today’s memo is on ClearPoint Neuro ($CLPT), a $500M medical device company that is enabling a new generation of neurological surgeries for direct-to-brain drug delivery. A recent FDA reversal involving one of its partners may have implications for ClearPoint’s broader platform that the market is not fully pricing in.

Over the last couple decades, one of the most important medical breakthroughs has been the rise of stem cell treatments. In 2023, the FDA approved the first stem cell treatments for sickle cell disease. More interestingly, scientists have figured out how to turn stem cells into brain cells. Given neurological disorders such as Parkinson’s typically involve the death of a specific neuron, finding a way to put fresh neurons back into the brain could improve symptoms. Only there’s a problem. Delivering these treatments to the right part of the brain requires getting past the blood-brain barrier.

That is where ClearPoint comes in. ClearPoint has developed the Neuro cannula, a very sharp needle to deliver drugs into the brain while remaining MRI-safe to allow detailed imaging and targeting. ClearPoint also has a full set of products around the cannula including MRI-guided navigation, software, infusion tools, procedure support, and training to ensure the needle gets the right spot. The margin for error is very low when inserting something sharp into the brain.

Over the past year, ClearPoint’s fortunes have been tied to UniQure, a biotech aiming for a treatment of Huntington’s disease (AMT-130) using ClearPoint’s cannula and navigation systems. When UniQure had good news, it was good news for ClearPoint. When UniQure had bad news, it was bad news for ClearPoint.

Recently UniQure had very good news. After a recent FDA leadership turnover, UniQure said the agency would allow it to use existing three-year Phase 1/2 data as the basis for an accelerated-approval filing. Since the announcement on June 17th, UniQure’s shares are up ~70% and ClearPoint’s shares are up ~35%.

The market has priced ClearPoint primarily as a UniQure proxy. The opportunity is that the FDA’s new posture may increase the value of ClearPoint’s broader platform beyond AMT-130.

ClearPoint’s Business Model: Volume-Based Surgery Disposables

Why did ClearPoint become a UniQure proxy trade in the first place? UniQure is not the first therapy to use ClearPoint’s platform. That was KEBILIDI , an FDA-approved treatment for ultra-rare AADC deficiency. But Huntington’s is a far larger and better-known disease market.

ClearPoint’s model is built around procedure volume. As therapies using its platform move from trials into commercial use, CLPT can sell recurring disposables such as cannulas and navigation grids. ClearPoint is currently on pace for $50M of 2026 revenue at ~60% gross margins, with disposables making up the majority of the revenues.

AADC deficiency is a very rare disease, affecting around 135 people worldwide. For a disposables business, this does not move the needle. While Huntington’s disease is still rare, it affects 40,000 Americans and over 200,000 Americans are at risk of inheriting the disease. So an approval on a Huntington’s treatment, especially one showing a “75% slowing of clinical progression” over 3 years is a more meaningful inflection business-wise for ClearPoint.

FDA Pivot on UniQure Eases Path for New Trials

UniQure had a rollercoaster-like path to the recent announcement. UniQure’s phase 1/2 trials involved 26 patients and was comped against an external benchmark (a population benchmark outside the study). The reason for the external benchmark is it is hard to get patients in these conditions to sign up for the risk of a receiving a placebo treatment.

The FDA under the previous leadership, “stated that it cannot agree that data from the Phase I/II studies, compared to an external control, are sufficient to provide the primary evidence of effectiveness required to support a marketing application for AMT-130. The FDA strongly recommended uniQure conduct a prospective, randomized, double-blind, sham surgery-controlled study.”

With the FDA now confirming the phase 1/2 data is sufficient for “accelerated approval,” this opens the door for other trials using external controls. ClearPoint benefits as much as anyone from the FDA’s pivot.

Former FDA Commissioner Peter Pitts told BioSpace, “I think 2026 is divided into two pieces with a very specific reason, and that reason is the departure of Vinay Prasad. I think with Dr. Prasad’s departure, FDA has returned to its senses as being a partner in innovation rather than a critic of innovation.”

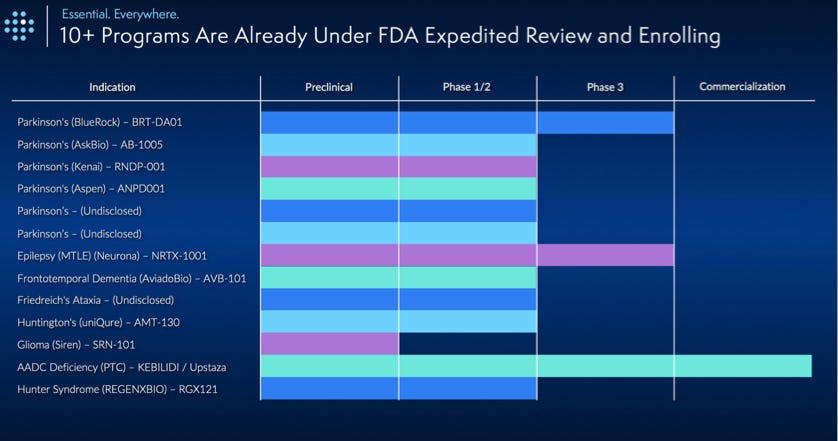

ClearPoint identifies 11 expedited-review programs in its ecosystem. Nine are in Phase 1/2 and two are in Phase 3. These candidates have the potential to drive revenues beyond AMT-130.

NRTX-1001 is a drug candidate focusing on Epilepsy, which affects 2.9 million US adults. Nearly 1 in 3 epilepsy patients are considered drug resistant, not controllable with medication. Neurona Therapeutics is developing a therapy NRTX-1001 for drug-resistant epilepsy using ClearPoint’s navigation system & cannula. The data for NRTX-1001 shows a “89% median reduction in disabling seizures” in months “7-12” for certain cohorts. Neurona Therapeutics was recently acquired by UCB for $1.15B, an indication that strategics are valuing the category.

Six of the 11 expedited-review programs listed by ClearPoint involve Parkinson’s. Parkinson's affects 1.1 million people in the US. AskBio’s AB-1005 is currently enrolling a phase 2 trial of 127 participants and has received a “pioneering regenerative medical product designation in” in Japan.

The market is focused on UniQure because AMT-130 is the most immediate bridge to commercial procedure volume, but larger indications like Parkinson’s are the real upside from a business perspective.

Valuation

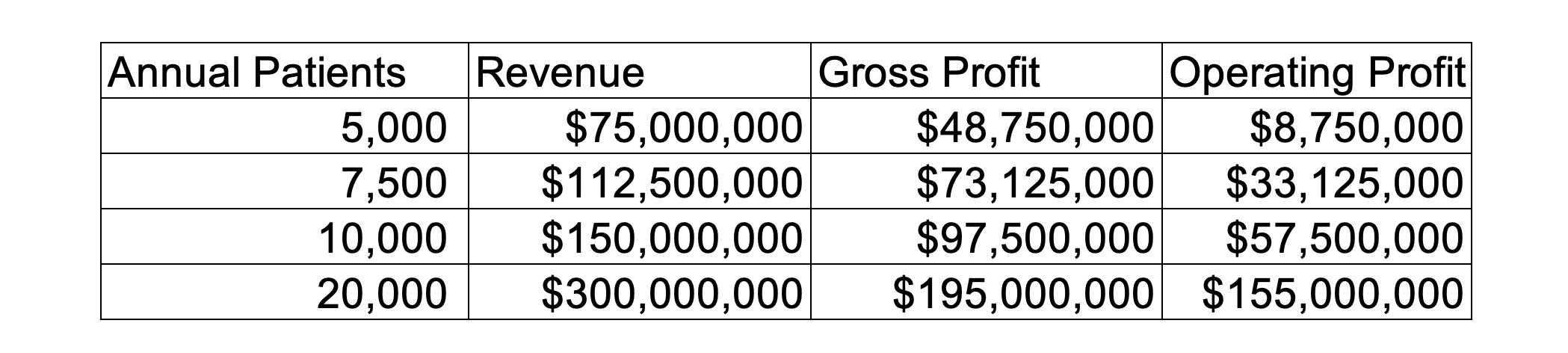

ClearPoint’s EV is roughly $582M. At about $40M of trailing revenue, it is not cheap on current numbers. Management has said 20,000 annual patients could imply approximately $300M of annual revenue. Treat that as an illustrative ceiling.

At roughly $15,000 per procedure and ~60%+ gross margins, there is a lot of torque in the model should a few therapies meet meaningful commercial volumes.

So the valuation is reasonable in the sense that while unprofitable today, there is a viable path to profitability and a fair valuation should they have the right set of approved treatments.

Price Target and Risks

While ClearPoint is well off the lows, but remains below the prior roughly $28–$30 high reached when AMT-130 initially looked promising last October. The bull case has gotten stronger since then with the Neurona Therapeutics acquisition by UCB.

The first hard catalyst is UniQure’s planned Q3 BLA filing for AMT-130, followed by whether FDA accepts the filing and the type of confirmatory study it asks for. A manageable path would validate for UniQure and for the perceived value of CLPT’s broader platform.

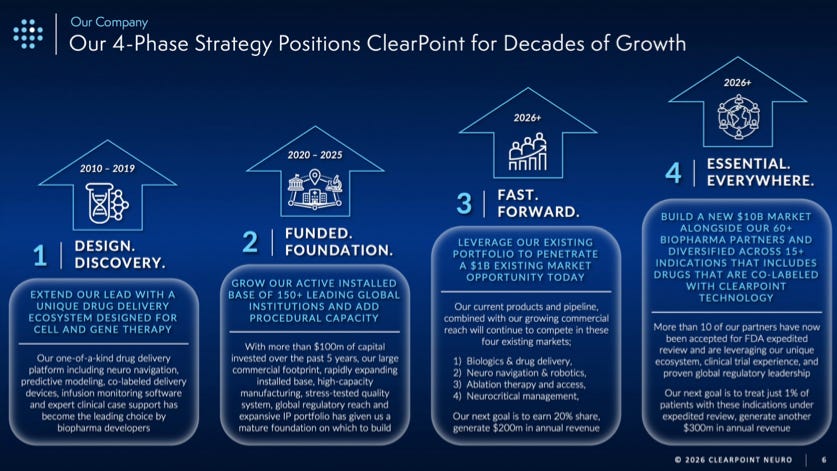

For CLPT to re-rate as a platform rather than a UniQure supplier, investors will need more proof points: additional positive partner data, progress from programs entering years two and three of Phase 1/2, and further regulatory clearance for ClearPoint’s delivery stack. In April, a surgical drill got cleared for clinical use. The company also has a Kuka robotic arm currently in preclinical use with pharma partners.

A return to the prior roughly $28–$30 range would imply that investors are again valuing CLPT as a platform rather than just a UniQure supplier. At that range, CLPT, which can be supported by the future earnings potential of $50M/yr of the platform should the platform hit scale.

Risks

The clearest risk is something could change for uniQure before approval. The FDA had a reversal previously so it could have another reversal again. Given consistent pressure and the change in FDA leadership for Huntington patients, this feels unlikely.

Another risk is someone makes a better cannula. In addition to patent protection, the path for a competitor to compete is difficult. The competitor would have to get new studies started which can take 5-6 years, a risk that a biotech does not need to take given ClearPoint has already been FDA approved before. The competitor would also have to figure out

Which centers are trained,

Which surgeons do the procedure

How to design a study (ClearPoint has its own CRO)

The software and systems beyond the cannula

Once ClearPoint is embedded in a clinical process, switching is not trivial.

CLPT is not profitable today. The company has invested ahead of the opportunity by placing systems, training centers, and building commercial infrastructure before disposable volume has scaled. So far SG&A has scaled in-line with revenues, over time the bull case is these diverge as ClearPoint achieves scale. One other red flag to note is the CEO has sold $1M into the recent rally.

To sum it up, this is a speculative, binary setup and should be sized accordingly. CLPT has already moved on the UniQure reversal, but the market may have priced the headline before fully pricing the broader platform read-through.

Disclosure: Author is long CLPT shares. Not investment advice - just ideas that seemed brilliant at 2am. Do your own research. Past results are not indicative of future results.