Caffeinated Memos: Buying into the HYPE

The fastest growing trading platform went from ~$0 to $800M+ fees produced in under two years since launch and it's not done.

Welcome back to the Caffeinated Memos series. Prior memos have a median 14% three-month return and 20% six-month return.

The past decade has seen the rise of several new trading platforms. Robinhood, founded in 2013 used commission-free trading and a Covid-trading boom to get to 27.4 million funded customers. More recently, Kalshi rode a friendly regulatory environment to $265M in fee revenue and a $22 billion valuation.

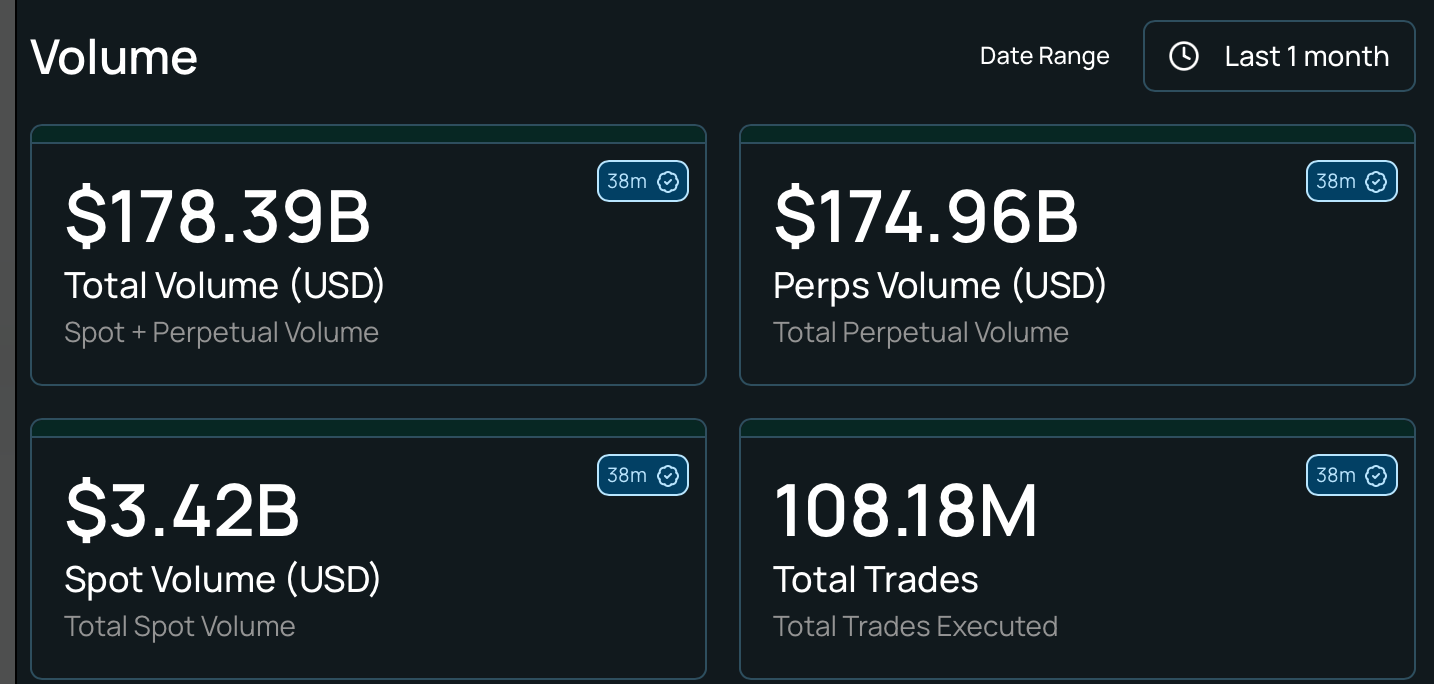

An even newer story is Hyperliquid. Hyperliquid was launched in November 2024. Run by a team of ~15 people in Singapore, Hyperliquid in the last 30 days has carried out over 100 million trades and $178B in total trading volume.

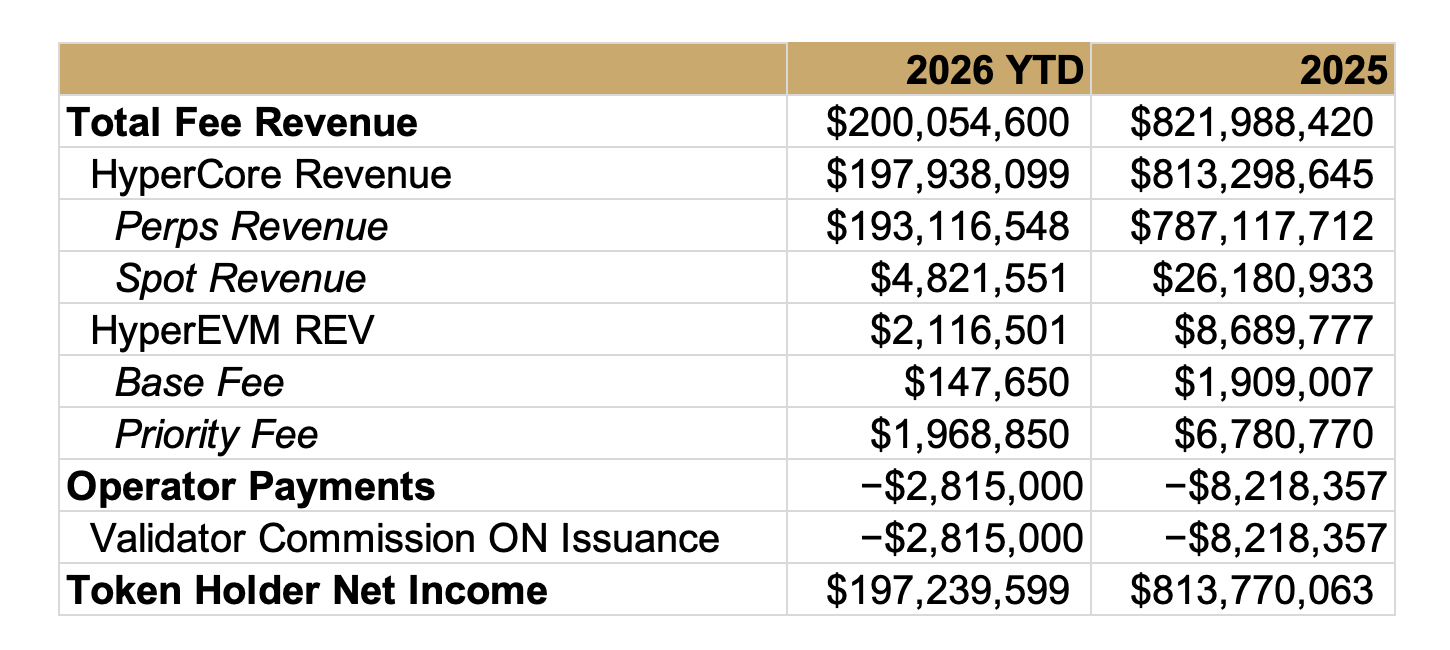

Hyperliquid has brought in over $800M of fees last year.

All of this is an incredible growth curve and raises some questions: such as 1. how did Hyperliquid take off so quickly, 2. what’s being traded on there, 3. where do all the fees go? And relatedly: how can one get exposure to Hyperliquid’s growth? Stock investors, don’t worry- there’s a Nasdaq listed proxy.

Decentralized Trading, Perps, and Leverage

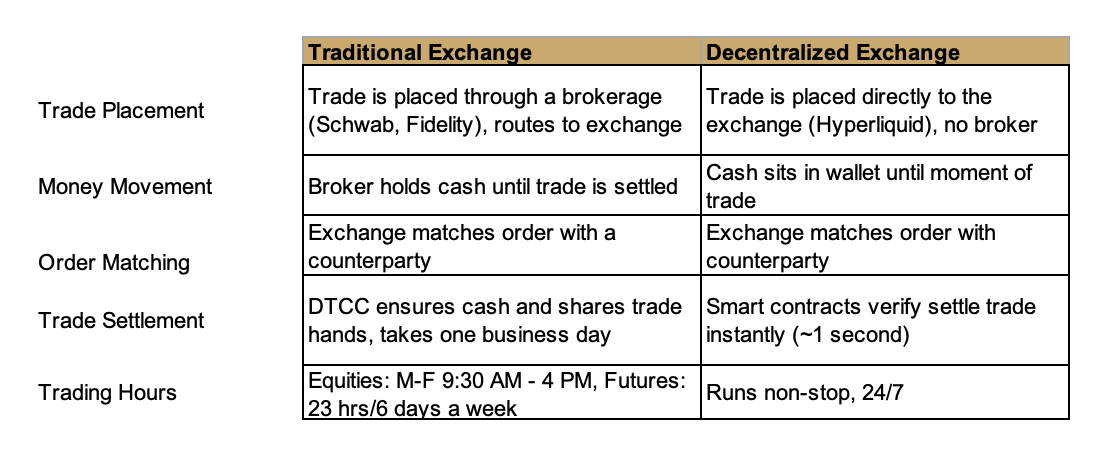

Hyperliquid falls under a category known as DEX or decentralized exchange. Decentralized exchanges use smart contracts, algorithmically tying your cash to the trade, effectively bypassing the need for brokers and time-consuming settlement.

A DEX can support a 24/7 cash settled future in almost any index or commodity. Even in illiquid markets. How?

The exchange relies on an oracle price, a benchmark the future on Hyperliquid is supposed to track. For BTC this could be the latest settlement price from Binance. When the price drifts from the underlying, i.e BTC is at $100K on Binance but $101K on Hyperliquid, a funding mechanism kicks in.

The longs will pay a yield for shorts to enter the market, set hourly until the $1K is resolved. The result: every exchange on hyperliquid has an equal amount of longs and shorts no matter how lopsided market sentiment might be.

This sets up the next trick. Since longs and shorts are in balance, Hyperliquid can match counterparties for absurd amounts of leverage without needing a balance sheet. If trader A has $1K and wants to be 30x long bitcoin, Hyperliquid doesn’t need to lend him $29K. It just matches his trade to a $30K short position. If bitcoin goes down 2% and his long position is liquidated, a profitable short position is closed (gaining $1K).

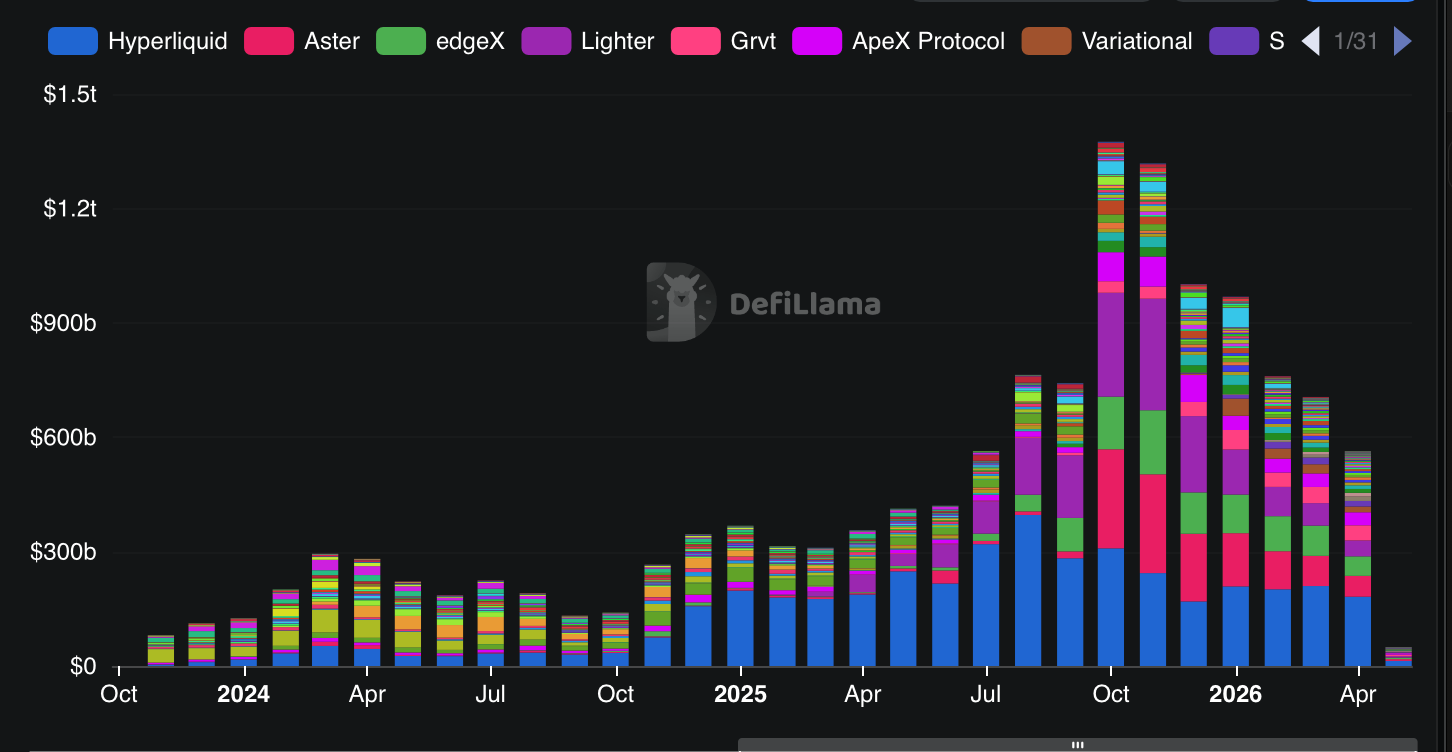

While Hyperliquid isn’t the only exchange that does this (Perpetual Contracts), it is the market leader. In April, Hyperliquid processed $181B of contract volume, 3x Aster, the #2 player.

Perpetual volumes as a whole are down since 10/10 (along with crypto volumes generally), but Hyperliquid has been gaining share.

Why? On 10/10, a threat of a 100% tariff on China led to $19B in Bitcoin positions were liquidated in a single day. This was a stress test for all leveraged crypto protocols and not every exchange passed, As Crypto Blog The Defiant reported:

”Lighter and other smaller perps venues went fully offline for minutes at a time. Meanwhile, Hyperliquid stayed online and profited.”

Critics argue Hyperliquid’s leverage mechanism accelerated the crash, but for traders, an early liquidation is preferable to a platform being offline during heightened volatility. Hyperliquid has consolidated its position as the leader.

There are also returns to scale. As Hyperliquid has the most active volume, it has the lowest slippage on new BTC trades, which helps fortify its lead over time.

Volume to Fees

Whenever a trade occurs on Hyperliquid, a taker fee and a maker fee is charged. While there are discounts for volume, the taker fee starts at 0.045% of the trade value and the maker fee 0.015%. As hundreds of billions are traded on the platform, Hyperliquid captures a small component. So on ~$181B perp volume in April → $60M platform fees, or 0.03% on average. So the more volume Hyperliquid does, the more fees it generates.

Where do all those fees go? Hyperliquid has a crypto coin called HYPE. Something on the order of 98%-99% of all fees go directly to buybacks (in crypto mechanics, they “burn the float”, as in move to an inaccessible wallet)

For analysis terms, this means the HYPE coin is more or less equivalent to the equity of Hyperliquid the company, given fees are the main revenue stream and 98% of fee revenue goes directly to buybacks, and the coin represents the main financial interest of the founders.

Quick Valuation Note

So we have a company founded in Nov. 2024 that made $814M last year with 98%+ operating margins and all profits going to buybacks.

So what’s a fair valuation? The HYPE coin is currently at a fully diluted market cap of $40B. So 50x trailing earnings. If you extrapolate the YTD pace that would be $590M or 67x earnings. None of that seems crazy for an asset this unique and high-margin.

The relevant question is was October last year a long-term top in fees? Or can Hyperliquid regain fee momentum and accelerate growth into the 2H of the year? For this, there are 3 relevant catalysts worth highlighting.

Three Catalysts

1. Hyperliquid has been expanding from crypto markets

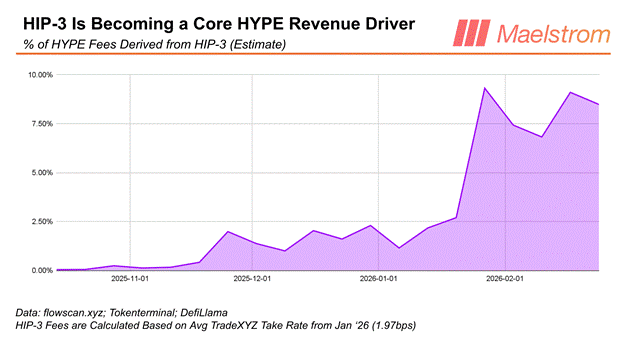

In October, Hyperliquid was only a crypto trading platform but that has changed dramatically. The HIP-3 upgrade allowed developers to create markets on top of the Hyperliquid framework.

When the Iran war started on a weekend, traders turned to Hyperliquid’s Oil future market, hitting $1.7B in peak volume. TradeXYZ built equity trading on top of Hyperliquid, including the official S&P 500 index. Almost ~10% of HYPE fees are now being generated from non-crypto activity.

This diversification will continue with HIP-4, which brings prediction market functionality to Hyperliquid. HIP-4 launched officially on May 2nd, meaning this is a very live catalyst as Hyperliquid’s prediction market ecosystem builds out.

HIP-4 has a distributed structure where anyone with 1M HYPE (~$40M) can deploy a prediction market, with their stake at risk if they manipulate outcomes. Over time, this could lead to more variety vs. Polymarket/Kalshi which curate markets.

Beyond prediction trading, HIP-4 can be hedging tools within the HYPE ecosystem (hold a stock while buying a ‘no’ on its next earnings beat). The more HYPE can activate non-crypto activity, the greater the argument for its outperformance vs. crypto as a whole.

2. Potential Crypto Recovery

A YTD performance chart of BTC, HYPE, and the S&P 500, reveals two things:

HYPE has been vastly outperforming BTC (64% vs. -9%)

BTC was at one point down 25% YTD vs. the S&P but has narrowed that gap considerably despite macro turmoil

Together this suggests a potential recovery from bitcoin with pessimism having peaked at some point in February.

One reason for optimism? On May 1st, Senators Alsobrooks and Tillis released a new compromise draft of the CLARITY Act after months of negotiations between banks and crypto firms. The act which clarifies CFTC over SEC regulation over most crypto use cases, is widely seen as a positive for the crypto industry but has been on hold due to questions on rewards programs as a loophole for paying interest on stablecoins.

The compromise bill delineates between interest and activity-based rewards and is now likely head to a markup and vote over the summer. If the act catalyzes an improvement in crypto as a whole, HYPE will be a beneficiary.

Crypto trading volumes as a whole are down 60%+ from October. A recovery in volume with Hyperliquid’s improved market position would lead to meaningful fee growth.

3. Possible US Market Entry

Hyperliquid is currently banned for US users (some use VPN) but they are making a legitimate lobbying push. In February, Hyperliquid launched the “Hyperliquid Policy Center,” with $29M in initial funding.

Jake Chervinsky, previously Chief Legal Officer at Variant is serving as CEO of the center and is making the argument that “the regulatory picture for crypto derivatives in the United States is uncertain”

While a tail outcome, US approval would lead to a derivative adoption by one of the largest crypto markets by trading volume. It may be possible for Hyperliquid to find a way into the CLARITY act before it passes.

Price Target:

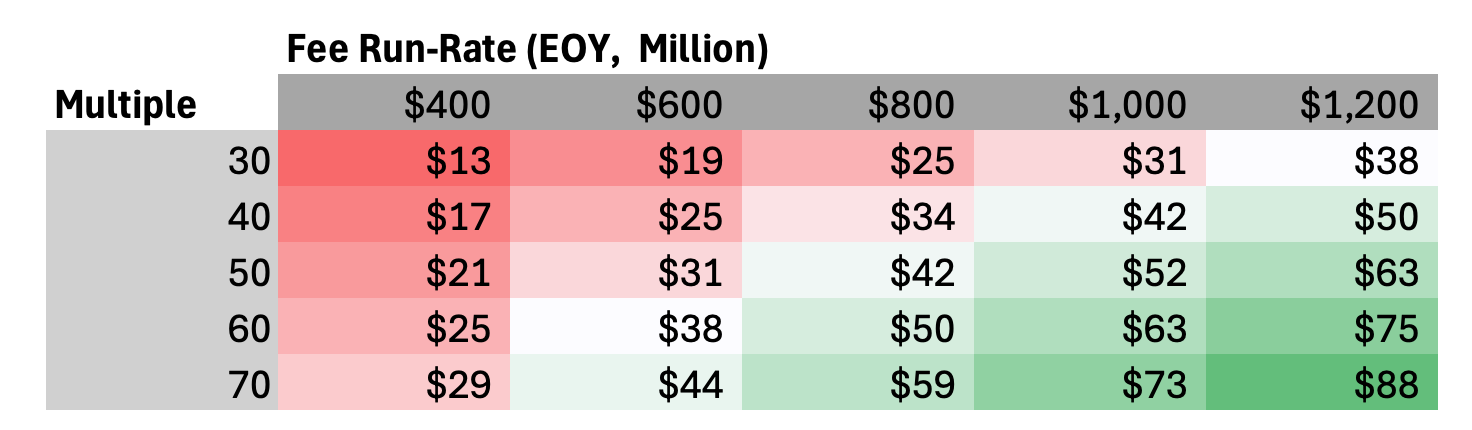

Retaining a 50x multiple on Hyperliquid's fees, the price can move to the $52-$88 range should volume recover. The bet is that between HIP-3 continued growth, HIP-4 traction, and any crypto recovery, HYPE drives its fee run-rate above last year's peak. $70 as a 6-month PT for HYPE is achievable without multiple expansion.

How to Buy It

Three Options for Buying Hyperliquid

Buy HYPE direct on a crypto exchange (Robinhood, Coinbase): as the 10th largest crypto by MC, most exchanges now offer it

PURR (NASDAQ) - Hyperliquid strategies: this is a Hyperliquid treasury company: it sells stock to buy HYPE tokens. Currently it is trading at 1.05x NAV or 1.15x including its tax liability (if it were to sell all HYPE). MSTR which popularized the category, traded above NAV before compressing after an ETF launch.

TXXH (NASDAQ) — 2x daily leveraged ETF, launched last week. Note a 2x leverage ETF will have slippage: if HYPE was down 5% one day and up 5% the next, the underlying would be down 0.25% but the 2x ETF would be down 1% (as went down 10% before up 10%)

Why not just wait for the spot ETF?

While there will be a spot ETF eventually (even XRP got one), Bitwise just filed its S-1, so actual ETF approval is likely 3+ months away

Tokens front-run ETF approval. BTC rallied almost 50% from October 2023 to ETF approval in January 2024

The most meaningful catalyst window, HIP-4 traction + clarity act is within the next 3 months

In short: the 1.15x premium is the price of being early.

For newsletter tracking, PURR will be the pick. While 1.15x premium is not ideal, that is the price of an accessible equity wrapper. Assuming mNAV compression from 1.15x to 1.05x during the trade window, this translates to a $9.78 PURR price target (+56%).

Risks

HIP-4 Fails to Gain Traction (want to see similar to HIP-3 a trajectory to 10% of volume)

CLARITY Act fails to pass (stalls in Senate)

Crypto rolls over again (HYPE would get hurt in a broader crypto risk off)

mNAV compression/slippage (for equity instruments)

Another exchange rises to the top (Hyperliquid is currently 3x its closest competitor)

Disclosure: Author is long PURR shares. Not investment advice - just ideas that seemed brilliant at 2am. Do your own research. Past results are not indicative of future results.