Caffeinated Memos: Argentina is the new Texas

Vaca Muerta Oil Producer Trading at Less Than 5x 2026 Operating Income

Welcome back to the Caffeinated Memos series. Prior memos have a median 13% three-month return and 33% six-month return.

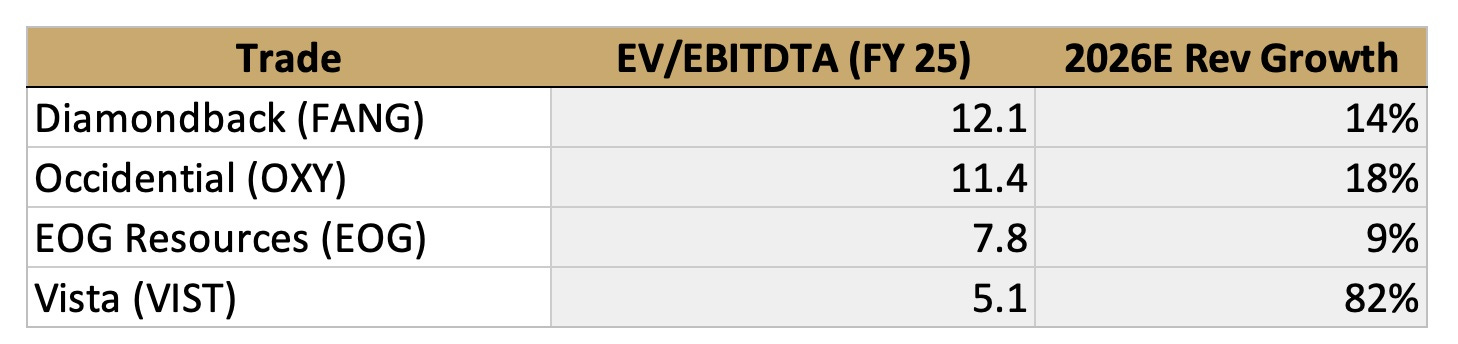

Chaos in the Middle East. Crude oil is trading above $100 a barrel. While this has been a clear tailwind for oil stocks in general (XLE 0.00%↑ is up almost 40% YTD), there is a producer in Argentina that is adding drills into the crisis faster than almost any US-based E&P and trades at a fraction of their valuations.

Vista Energy VIST 0.00%↑ was already riding a secular trend: the Permian boom of the last 15 years has peaked. The largest shale formation in the Americas outside of Texas is the Vaca Muerta. Combined with the most corporate-friendly political regime in years, Argentina was poised to experience its own version of the 2013 shale boom before the Iran war broke out. Vista Energy grew production 66% YoY and aims to double exports from 22 million barrels in 2025 to 44 million in 2028. They added over 10% production YTD… and they’re not done. Yet the market is valuing them at 11x last year’s earnings… on fears oil prices will revert to the pre-war levels in the $60s. Does that make sense? Vista energy is poised for further upside even on a quick resolution of the war.

Oil Prices are Not Returning to Pre-War Levels: $80 is the new $60

The most common retort from investors is “how can you invest in energy when the war could end tomorrow?” After all two weeks ago the war was “very much complete.” Marco Rubio told the G7 this past weekend the war was “2-4 weeks” from wrapping up. The pentagon is preparing for “weeks of ground of operations.” Whether the war is ending in days or months, investors have been overly focused on the timeline of the Iran operation and not the reality that the post-war environment will have structurally higher oil prices. Why?

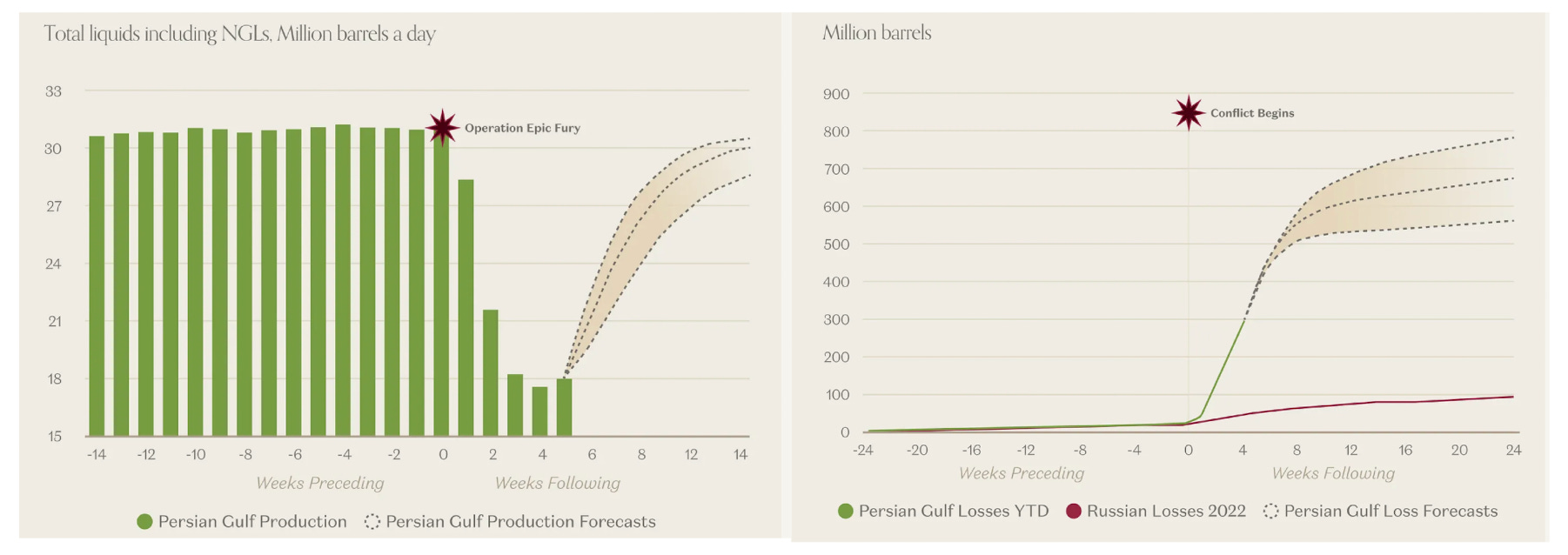

1. The existing closure has already significantly set back production

With the Strait of Hormuz closed, Gulf Countries have shut in production as their storage facilities have filled. To quote the IEA, “Gulf countries have cut total oil production by at least 10 mb/d. In the absence of a rapid resumption of shipping flows, supply losses are set to increase.” As we’re a month into the operation, this means there are ~300M barrels that never came out of the ground.

Additionally, this production that was shut-in does not get re-opened overnight. As Rystad Energy’s Aditya Saraswat noted, “It could take two to three weeks to restore full production at a small field that’s been halted, and four or five weeks for a larger one.” So even if the war ends tomorrow, there will be a lag to ramping up to full production.

2. The strategic reserves that have been drained need to be refilled

Countries have responded to this significant drop in production with releases from oil reserves: “IEA member countries agreed on 11 March to make available an unprecedented 400 million barrels of oil from their emergency reserves available to the market to mitigate the negative impact on economies from the supply disruptions.”

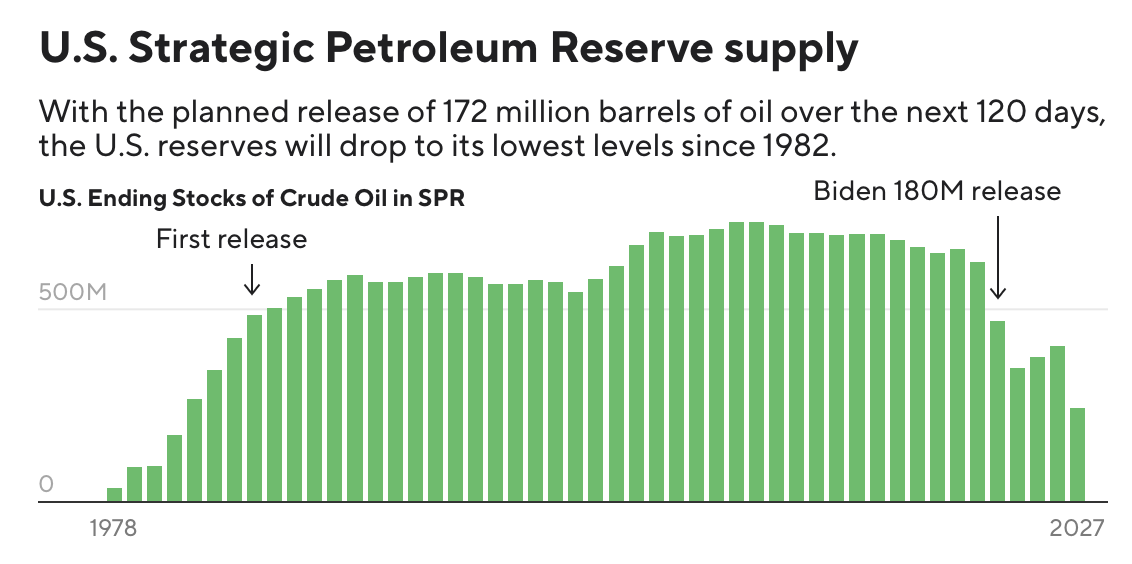

The issue is the current drain follows the 2022 reserve IEA reserve drain of 182 million barrels, which was also “unprecedented”. Many countries did not fully refill their reserves to pre-2022 levels. The US is projected to end the war with the lowest levels in the strategic reserve since 1982.

While the US may delay the refill until after midterms, there will be a critical need to refill the SPR from these low levels. China, which also maintains a sizable strategic reserves for strategic/commercial reasons, is likely to refill any reserves drained during the war.

3. Neither OPEC or the Permian Can Afford Sub-80’s

The damage to Middle East infrastructure has been extensive. Energy infrastructure has been targeted throughout the war. Even without further escalation, over 40 Middle East energy assets have been “severely damaged” per the IEA, in addition to lost tourism revenue, airports targeted among other collateral damage.

While Saudi Arabia and other gulf nations have sub-$40 barrel breakevens, their budgets assume significantly higher oil prices. Saudi Arabia’s Fiscal Breakeven before the war (to be in a government surplus) was $94/barrel. Now with the added burden of repairing war damage/replacing missile defenses, Saudi Arabia (and other Gulf States) have a massive fiscal hole.

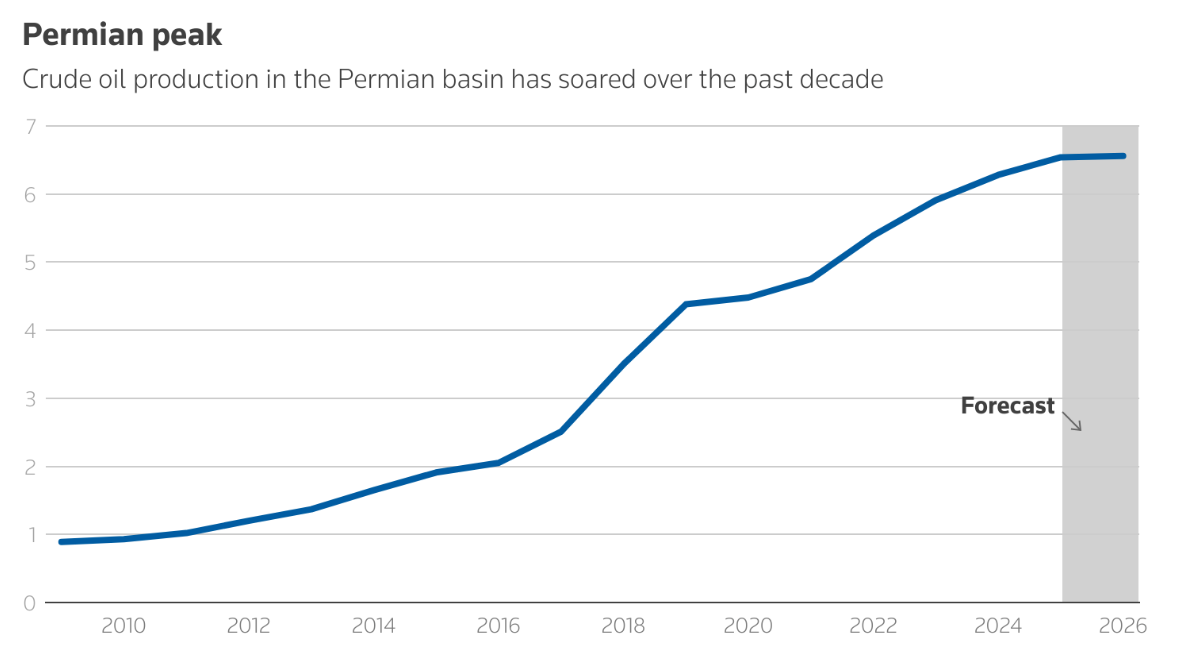

While OPEC in the mid-2010s facilitated “price dives” to take out US Shale players, it does not make sense in the post-war environment. US shale players don’t want $60’ oil either. After ramping significantly over the last decade, the permian production is considered to have peaked.

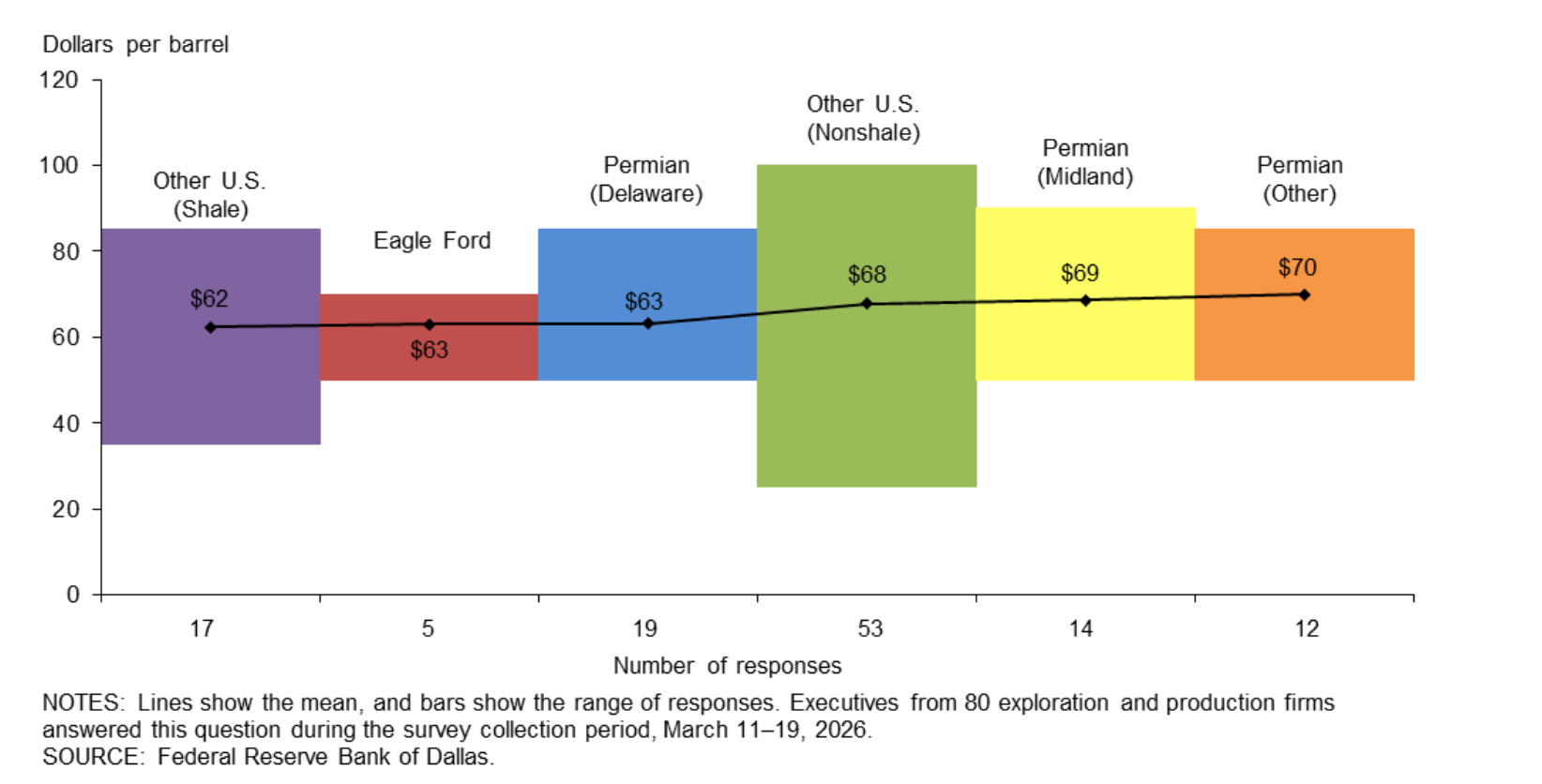

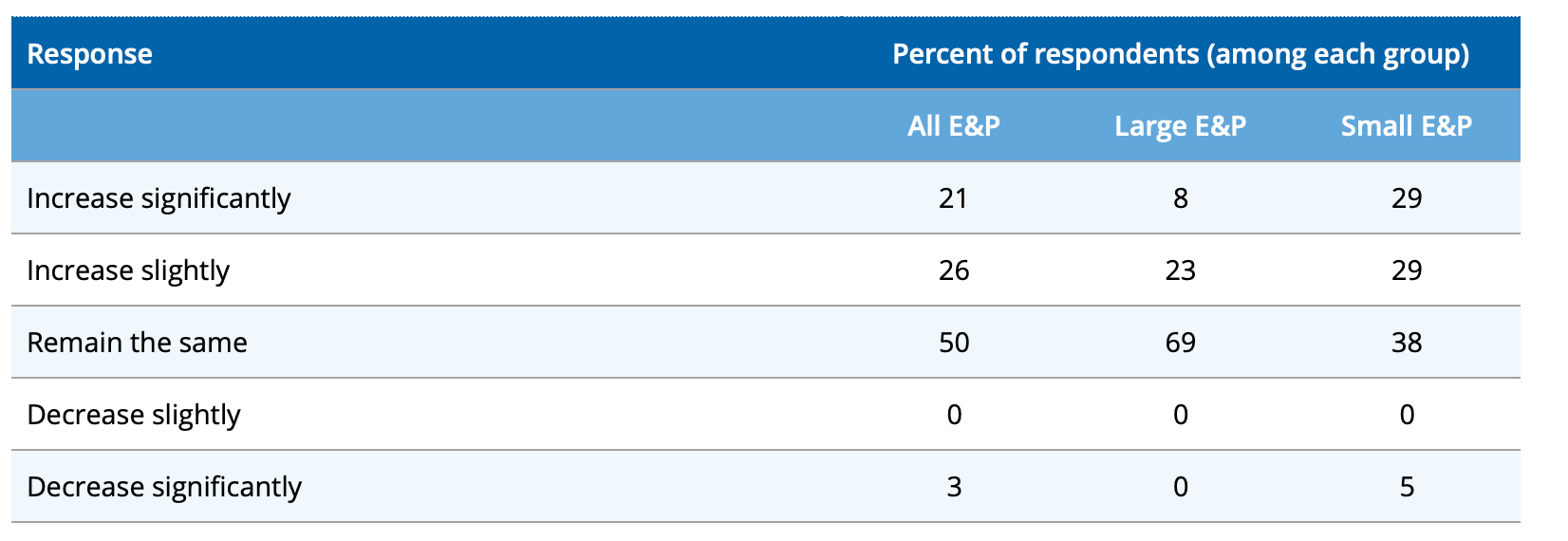

Like any oil boom, the easy sites were tapped first. The sites being drilled in the Permian today require significantly higher breakevens. Execs surveyed by the Dallas Fed in March stated they need at least $60-$70 oil prices to profitability drill a new well.

They were also asked by the Dallas Fed if they planned to increase their drilling in light of the recent events. 50% of E&P’s said they would not change their plans, even with the current oil surge. Only 21% of E&P’s said they would increase drilling significantly.

At the CERAWeek energy conference in Houston held on March 23rd, ConocoPhillips’ Nick Olds said they were “not currently increasing production (in the lower 48 states)” adding ConocoPhillips would need to see “sustained higher prices.” SLB exec Steve Gassen stated “the cycle from the time you begin to when you make a decision that you're going to add rigs to then ultimately drilling and producing and getting to market, that can be a year-long process, even in the U.S., which is a short-cycle market. Nine months would be the very best-case scenario.”

The US which was “the swing producer” is not adding rigs into this crisis. So who is?

Vista Energy: A Rapidly Scaling Pure Play Argentina Shale Producer

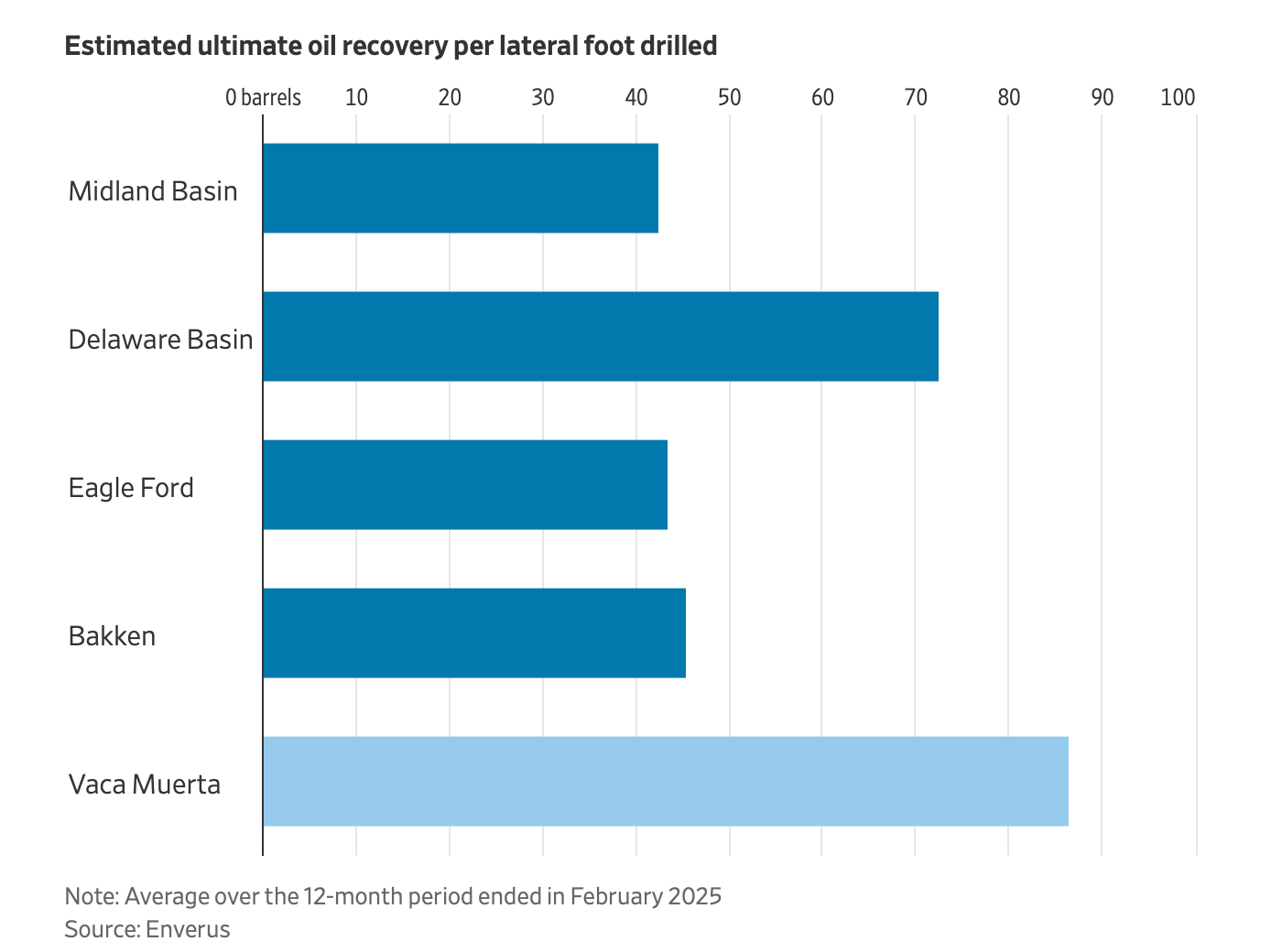

The Vaca Muerta is the “second largest shale gas reserve and fourth largest shale oil reserve on the planet.” Compared the Permian, the Vaca Muerta is relatively untapped. Wells are 20% more productive than the Delaware basin and 100% more productive than the Eagle Ford on a barrel/lateral foot basis.

Vista Energy’s CEO/Founder Miguel Galuccio was formerly the CEO of Argentina’s State Oil Company YPF, where he was branded "the Architect of Vaca Muerta.” While YPF had much more resources it is also 51% government owned. Galuccio took Vista Energy public in 2019 as a more “nimble” independent pure play. It has worked out spectacularly for shareholders, with the stock returning almost 800% since inception

Today, Vista energy owns 229,000 acres with 1,300 ready to drill locations.

Unlike most shale producers, they are operating at only 1.5x leverage. 64% of their barrels produced are exported outside of Argentina into the global market.

While the operating performance and track record are already better than most independent oil producers, a more recent move speaks to the quality of management.

On February 2nd, just weeks before the start of the war, they bought Equinor’s full onshore Argentina assets. The deal added ~22,000 barrels/day to Vista’s production. Management bought this asset for US$712 million for a highly accretive 3x 2025 EBITDA (at a $70.2 average oil price). The deal also includes an annual contingent payment linked to oil prices but no payment is due below $65 Brent and above $80, Vista keeps 100% of the incremental upside on every barrel produced from the acquired assets.

Shale is already the fastest type of oil asset to scale production. Yet Vista has a head start on every shale producer as it was actively acquiring and drilling ahead of the crisis, instead of trying to catch up on a 6-9 month timeline.

Vista By the Numbers

Vista energy had already guided to a great year on its Feb 26th earnings call. This guidance included growing production 22% and showing operating leverage with lifting costs only going up 7% and FCF doubling.

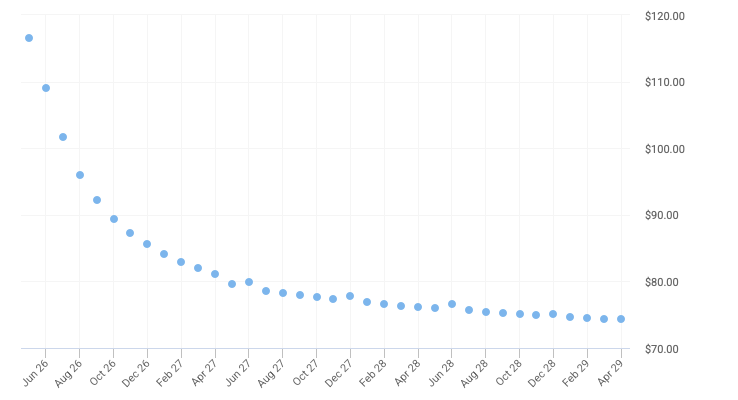

The fun part is the guidance assumed $65 oil for the rest of 26. Here’s the current futures curve for Brent oil.

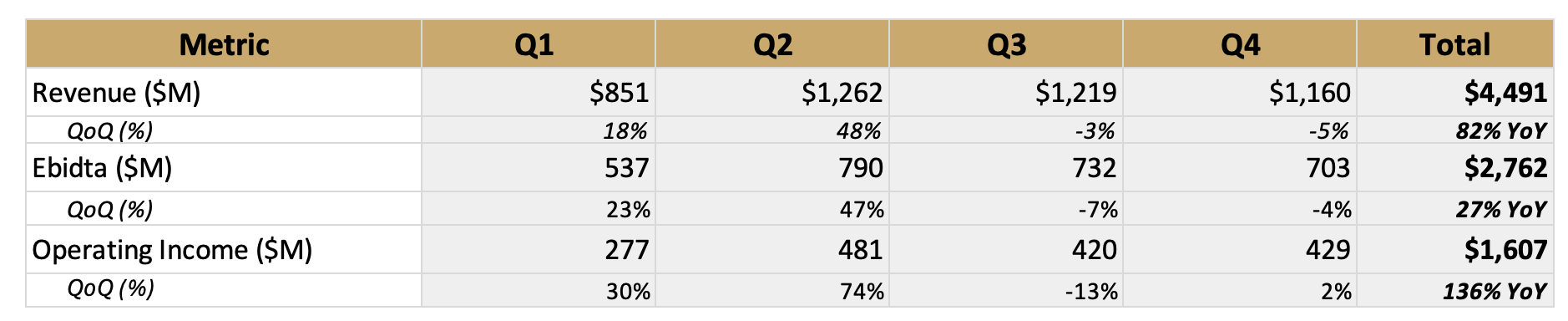

Analysts are pricing this is as a massive jump in profits in Q2, followed by declines in Q3/Q4. Even with this assumption, Vista generates $2.8B in EBIDTA and $1.6B in operating income.

The company as a whole is valued at $10.1B EV even after the 50% run-up YTD, putting it at a 3.6x 2026 EV/EBIDTA. Unlike most oil companies, Vista is growing production fast enough to outweigh the expected price decline in the 2H of the year (see the 2% QoQ growth in Q4).

On the FY25 Q4 earnings call (February 26), CEO Galuccio called out that the company had added 10 wells in January with “very good productivity,” leading to a production rate of 132,000 barrels of oil per day in February. He added that March was a “very good surprise” estimated to surpass 140,000 bbl/d, the full-year guidance number. And that’s before Vista gets the 22,000 barrels from Equinor (closes in Q2).

A recent UBS note on February production confirms the ramp is accelerating, with Vista’s production “up by +10% MoM” with 4 new wells “in production early stages, implying potential additional production ramp up ahead.”

As Galuccio mentioned in a March 12th interview with Bloomberg: “We have a lot of elasticity: We drill a pad of four wells in four months […] so if we push a button today because we have more capex because the oil price is higher, in four months we’ll be delivering more to the world.” Vista is likely already trending well above its 140K barrel full year guidance.

And the production growth story has no reason to stop in 2026. A recent Goldman Sachs note on South American oil producers argues “Vista and YPF would be more likely to speed up production growth" in a sustained oil disruption compared to Brazil’s Petrobras or Colombia’s Ecopetrol due to less leverage on the balance sheet.

Goldman Sachs estimates: “fracking projects under development in Argentina and Saudi Arabia alone will meet roughly one-fifth of expected global oil demand growth through 2030.” Vista is the best pure play on the Argentina side of the equation.

Price Target: $100 in the next 3 months (4.5x 26 EV/EBIDTA). This does not require a significant re-rating but merely maintaining close to the current multiple in a period of significant production growth.

Risks:

Any headline that confirms a ceasefire or Strait of Hormuz opening will lead to an immediate 10-15% drop on sentiment alone. For the reasons outlined above, a drop like this should be viewed as a buying opportunity.

A large part of the discount is explained by political risk in Argentina. While Milei won the midterm election, his approval rating has fallen in recent months. YPF re-nationalized in 2012 and investors have painful memories of the situation. This will be more significant in 2027, the election year.

Investors believe a sustained period of $100+ oil would be bad for oil producers due to demand destruction. While this was a price level associated with demand declines historically, the bar is higher in 2026. The world is 56% less dependent on Oil for GDP growth since 1973 (Columbia SIPA). The 2008 oil high was $147 or $223 adjusted for inflation. Demand destruction is still a risk but requires higher prices than $110. The global economy still grew 3.4% in 2022 despite WTI averaging $100.

Vista is likely to reinvest back into CapEx as opposed to significant buybacks/returns to investors. With an ROIC of 19.7% (as of the end of 2025) and the immediate return on the Equinor acquisition, Vista’s management has demonstrated themselves to be capable capital allocators.

Vista energy is still limited in part by the ability of oil services to get to Argentina and build pipelines/exporting infrastructure. As Galuccio noted in the Bloomberg interview: “to accelerate, we need more capital, we need more oil service providers, more product providers, more competition.”

Disclosure: Author is long VIST shares. Not investment advice - just ideas that seemed brilliant at 2am. Do your own research. Past results are not indicative of future results.