CM#9: The AI Energy Crunch, Natural Gas, and a $4 SPAC beneficiary

Why the Rice Brothers' Carbon Capture Play Offers Asymmetric Upside

Welcome back to the Caffeinated Memos’ series. Last month we covered Google’s AI Turnaround and went long GOOGL Nov 21 255 Calls, which are up ~300%.

After Mag 7 earnings season, one thing is clear: AI’s energy demand is accelerating faster than anyone projected. While nuclear names have rallied on this thesis, last week Google quietly announced something more immediately actionable: their first carbon capture and storage project using natural gas. This shift opens the door for $NPWR, a sub-$500M EV carbon capture pure play most investors have overlooked with asymmetric upside potential.

TL;DR: AI needs power ASAP. Nuclear takes too long. Solar is intermittent. Natural gas with carbon capture offers the goldilocks solution and $NPWR is the pure play.

AI’s Energy Demand: The Key Limiting Factor

Various components go into a data center: servers, racks, cooling, land, power, and of course GPUs. Many of these components are in shortage, but the most crucial is the power. In general, servers and data components are used to rising demand and secular growth. U.S. power generation is not. The US did not add power to the grid for most of the past 15 years.

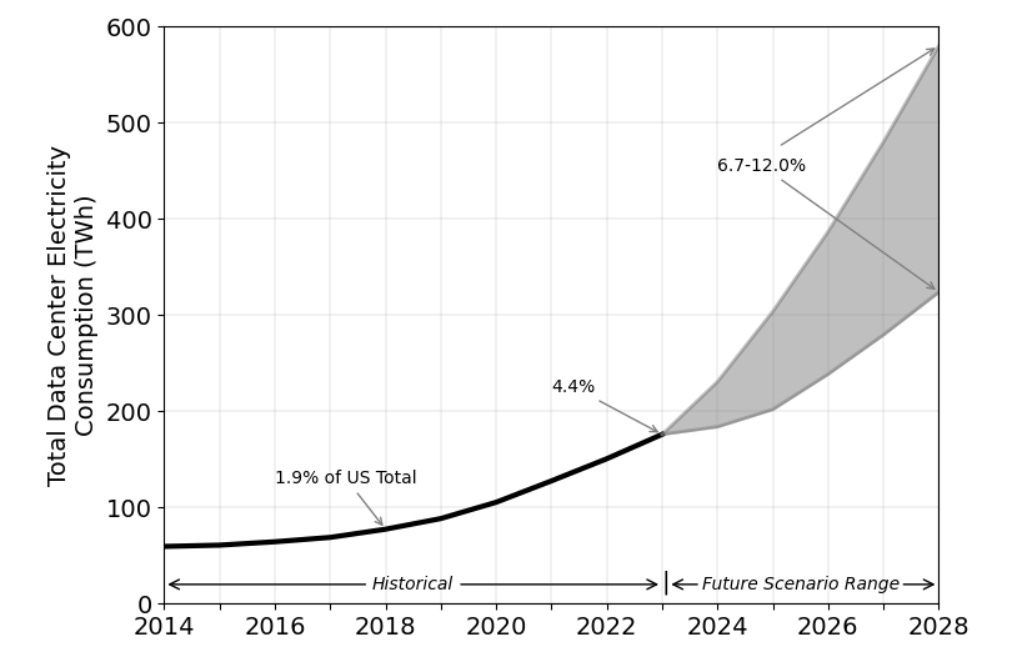

Coal-fired plants have been replaced with less polluting natural gas, but net energy demand had remained stable. That’s about to change. Data centers are expected to add at least 325-580 terawatt hours to the US power grid through 2030.

Data centers are projected to go from 2% of US total power consumption (historical) to ~10%. This requires net new power plants. Mag 7 CEOs keep reaffirming their need for power:

Andy Jassy said on the Amazon Q3 earning’s call: “we’ve added 3.8 GW of power in the past 12 months. To put that in perspective, we’re now double the power capacity that AWS was in 2022, and we’re on track to double again by 2027”

CFO Susan Li said on the Meta Q3 earnings call: “our compute needs continue to expand meaningfully, including versus our own expectations last quarter […] CapEx dollar growth will be notably larger in 2026 than 2025”

Satya Nadella said on the B2G pod: “The biggest issue we have is not compute, it’s the power. It’s the ability to get the builds done fast enough close to power.”

Why There’s No Perfect Power Source

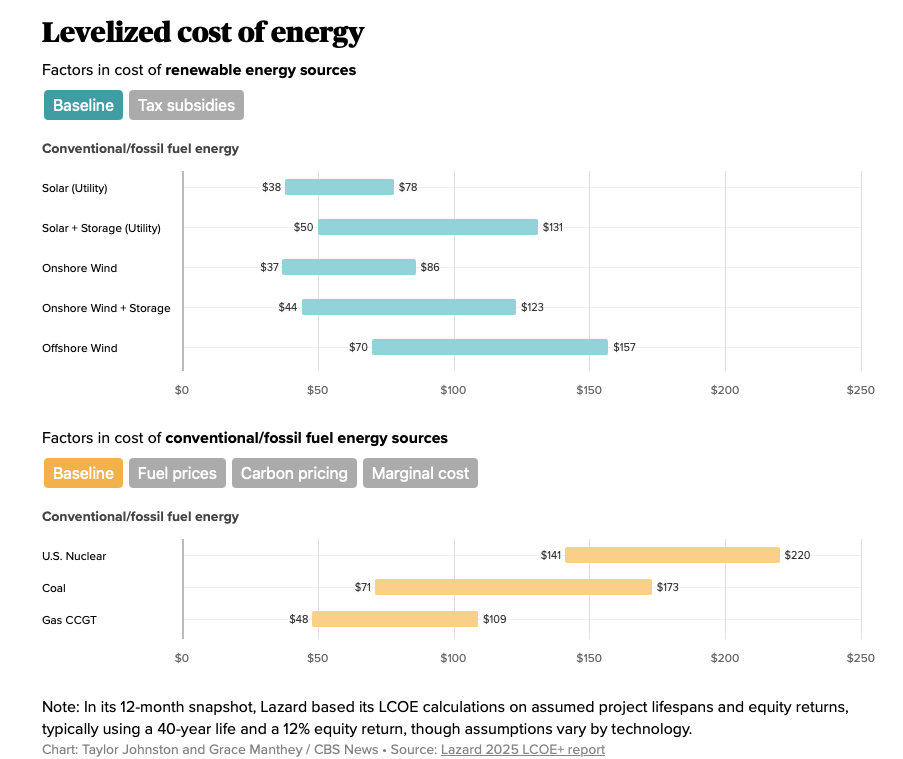

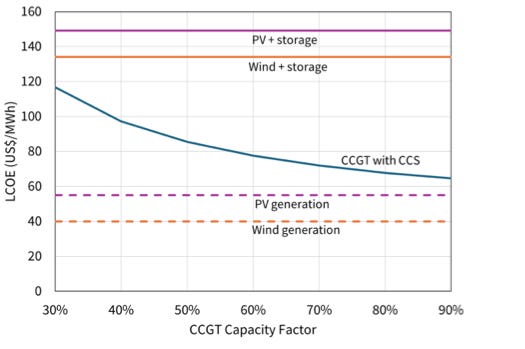

The quickest and cheapest way to spin up a new power plant is natural gas. Gas plants are roughly on par cost wise with renewables and solars (as IRA credits have been removed) and far cheaper compared to nuclear.

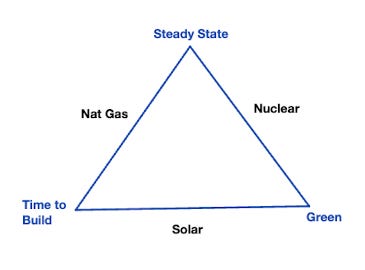

The LCOE on solar/wind is also often estimated too low, as when solar/wind conditions are not ideal, more of the energy grid needs to pick up the slack. For data centers which ideally are running 24/7, they prefer a steady state source of energy. The energy trilemma is visualized in this triangle:

Solar is green and fast to build, but intermittent. Nuclear is green and provides steady power, but takes a decade+ to construct. Natural gas hits the sweet spot, it’s fast to deploy and provides steady baseload power. The only drawback? Carbon emissions

Many of the big tech players including Microsoft, Google have made some pledges to be net zero by 2030. For Amazon, it’s 2040. These pledges are not that important in a Trump administration. But many of these power plants will come online in 2027 or later, with the bulk of their operating lifetime during the next administration.

Generally, it’s not good optics to be laying off tens of thousands of employees and polluting the environment. If AI continues to disrupt the labor market, a not so “out there” idea is a tax on AI carbon emissions, especially in a future democratic administration. But with natural gas being this cheap, hyperscalers can’t afford not to take advantage.

What if there was a way to still use natural gas but be effectively carbon-free? Enter carbon capture.

Google Adopts Carbon Capture

With AI data center announcements happening almost daily, an easy one to miss would have been Google last week announcing “their first carbon capture and storage project.” Google announced they “identified natural gas with carbon capture and storage (CCS) as a critical source of clean firm power”

“The Broadwing project is located at an industrial facility run by Archer Daniels Midland (ADM), which has nearly a decade of experience safely storing CO2 from ethanol production. A new power plant with over 400 MW of generating capacity will be built on site, and the CO2 it generates will be permanently stored in ADM’s adjacent EPA-approved Class VI sequestration facilities more than a mile underground.”

Google also attached this a helpful video illustrating how it will work:

CCS captures the emissions from natural gas combustion, condenses them, and stores them deep underground, turning a “dirty” fuel into 90%+ carbon-free power. Gas turbines with carbon capture are likely cheaper than wind or solar + battery storage while delivering comparable emissions reductions.

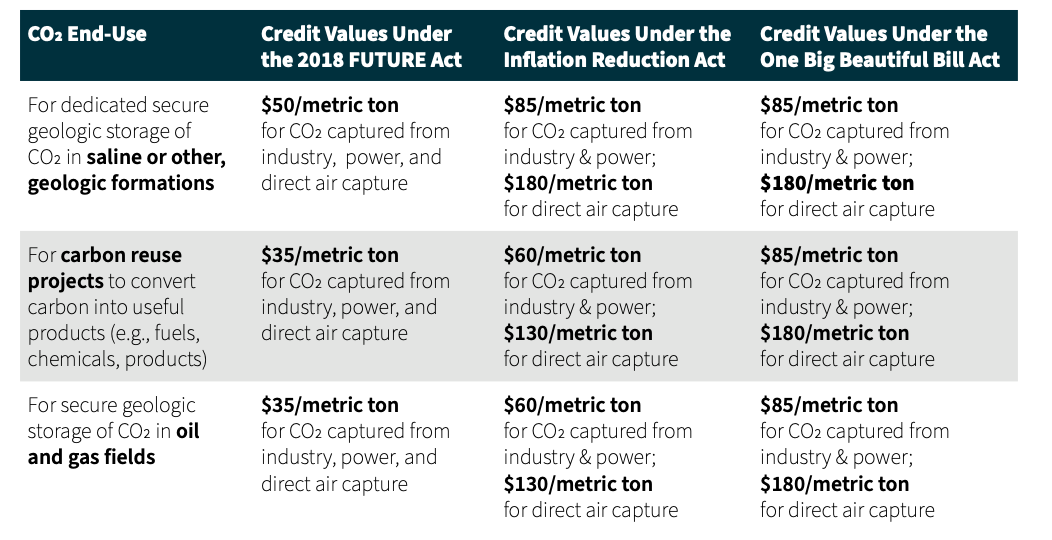

So why is carbon capture suddenly viable for hyperscalers? The “big beautiful bill” increased subsidies for carbon capture from $60 to $85 a ton, a 42% jump, at a time when most green technologies are seeing subsidies cut. As it turns out, the easiest way to win Republican support for green energy is to say “clean natural gas.” Combined with improved bonus depreciation on land, natural gas with carbon capture might have just become economically superior to renewables.

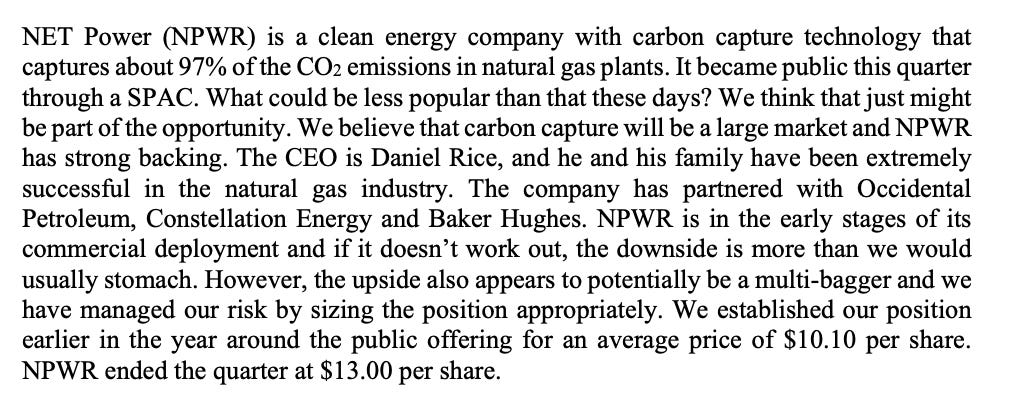

How do you play this? Google is using Archer Daniels Midland, which is too large of a company for this to move the needle. Luckily, NetPower ($NPWR) is a pure play natural gas carbon capture name, trading at sub-$500M EV.

NetPower: A Credible Carbon Capture Play

When you hear “zero-revenue energy SPAC” your brain auto-correlates to fraud (zinc battery storage didn’t work?) This isn’t your typical spac disaster.

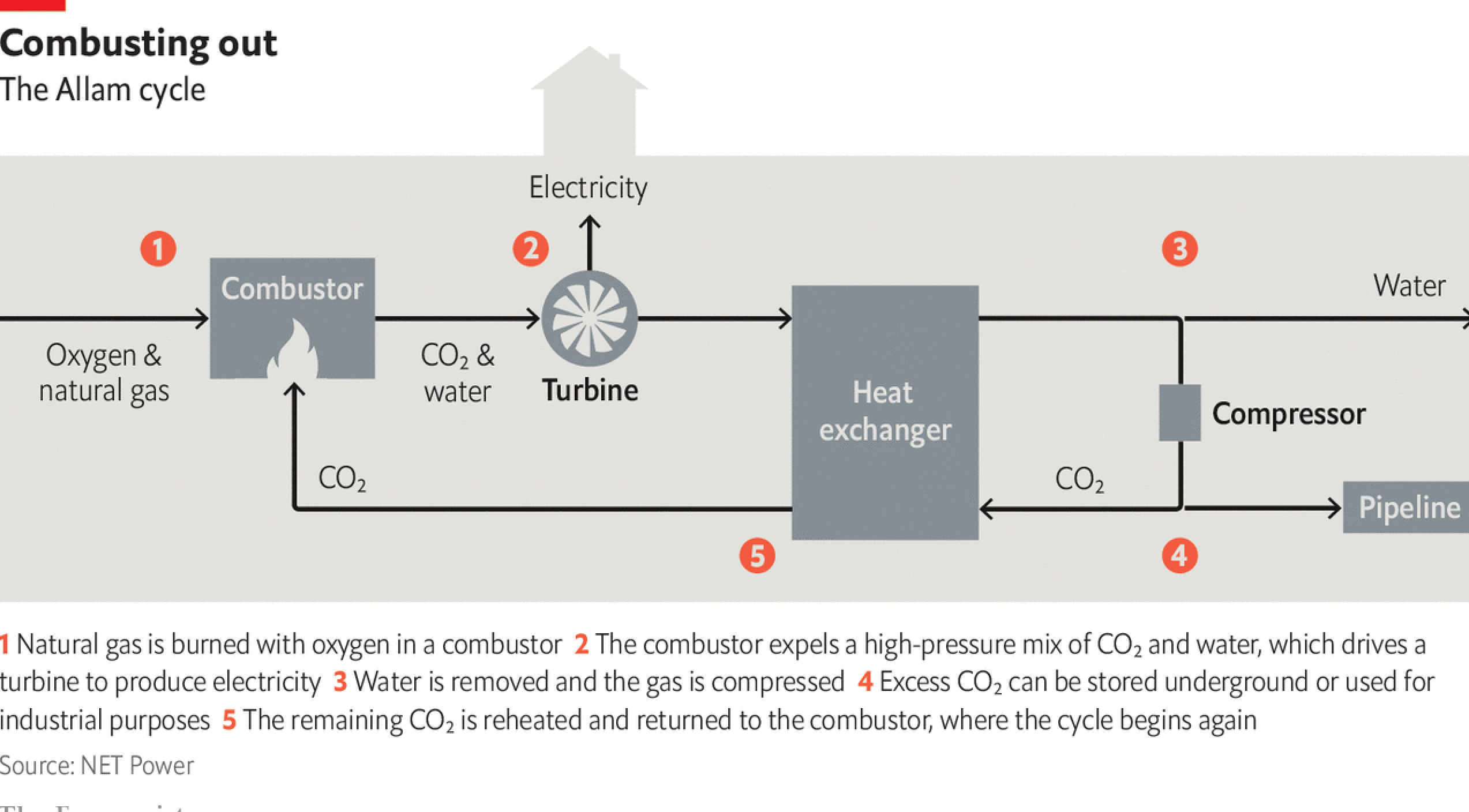

NetPower is 40% owned by Occidental Energy, not the type of investor to throw millions on fake science. The Rice Brothers, who built Rice Energy, took Archaea Energy public (acquired at $26/share) are the driving force. Danny with his brother Tony Rice have been power players in the natural gas space. Danny Rice is on the board and Tony Rice is the CEO of EQT, the largest US natural gas producer. Baker Hughes is managing equipment and construction. The core technology, the Allam Cycle, developed by MIT and tested successfully in a 50MW proof of concept.

Even the conservative Joel Greenblatt was long at one point:

The idea of the Allam Cycle is to use as much of the CO2 back into the combustion process as possible, reducing the amount that needs to be stored underground.

While NetPower has almost revenue today, their core project is Project Permian, a 370MW carbon-neutral plant, located in Odessa, Texas.

| Seeking Alpha")

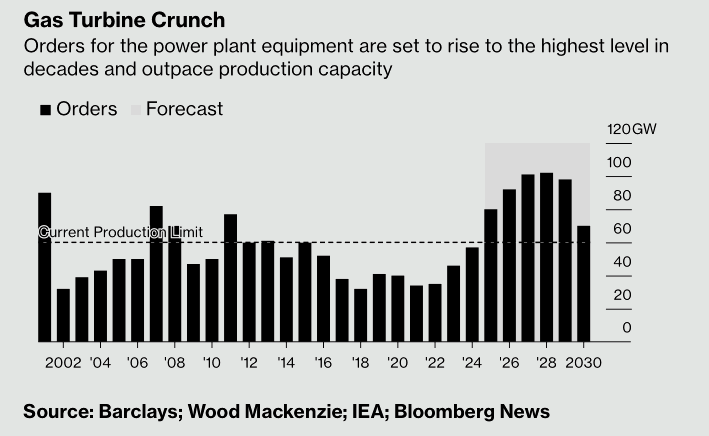

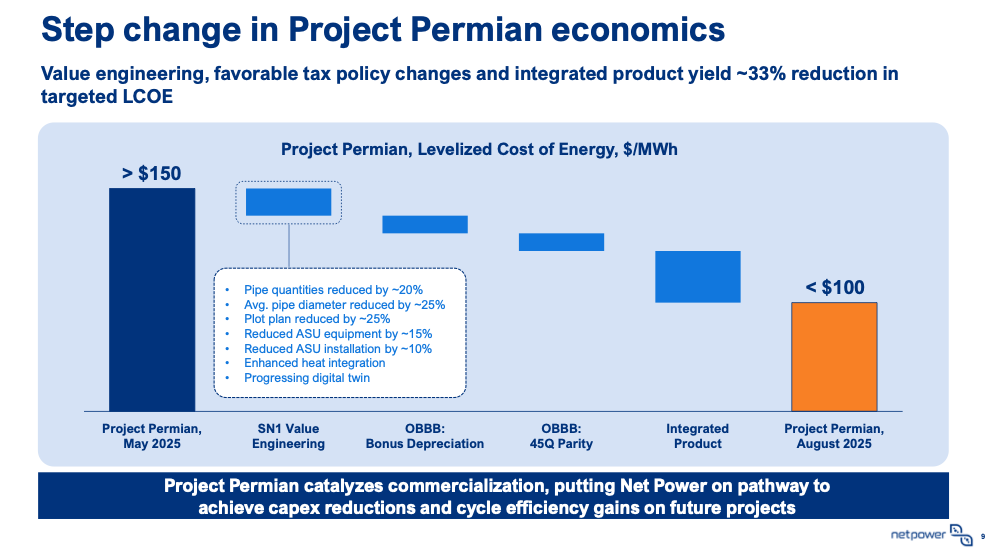

What went wrong that sent the SPAC tumbling down to $2-$3 a share? Since initial projections, the cost for the plant rose to “between $1.7 and $2 billion, up from an initial cost range of $750 to $950 million and then $1 billion when it was announced in November 2023.” The demand for natural gas plants nationwide has caused a shortage in components, along with various issues one faces when scaling an innovative technology for the first time. While NetPower had started with a healthy $650M cash on hand, the project now is likely to use all the cash on the balance sheet. The sell-off was rational and that creates the opportunity.

Here’s what changed. Danny Rice has taken a more hands-on role at the management of the company, after having fired the COO and the CFO in April. NetPower has mitigated the delays with a plan to generate revenue before the cycle is finished:“in August released an updated strategy that would bring simple cycle natural gas turbines to the project site sooner - potentially in 2027 or 2028 and subsequently integrate those assets with the Net Power Cycle turbine, all on the same schedule announced in March.“We said why can’t we sequence to deploy gas turbines now and when the Net Power Cycle is ready, those same turbines can provide auxiliary power to the plant,” Rice said.

The other key catalyst is the increase in CC subsidies in the “big beautiful bill” along with improved bonus deprecation for land projects.

This helps to ensure the project’s economics will make sense once complete.

There is a final key catalyst remaining, a PPA (power purchase agreement) from a hyperscaler for the plant. Danny Rice believes this could happen soon “Most important, and unique to West Texas, data centers and hyperscalers are wondering how to get as much power as they can as quickly as they can. We’ve seen the last couple of years a shift in the market to as much natural gas generation as possible. It’s the only thing that can scale to the amount needed and offers affordability.”

A PPA would fill the funding gap needed to finish the plant without dilution and allow NetPower to raise funding in the credit markets. The hyperscalers are paying a lot for clean power. Terrawulf’s 200MW NY plant signed a 10Y PPA for $3.7B in contracted revenue. While NPWR, is not as close to a dense metro, a PPA for NPWR’s 370MW of carbon-free power could deliver $3-4B+ in contracted revenues against the current $430M enterprise value. The stock would likely double on a PPA announcement and this is not just wishful thinking.

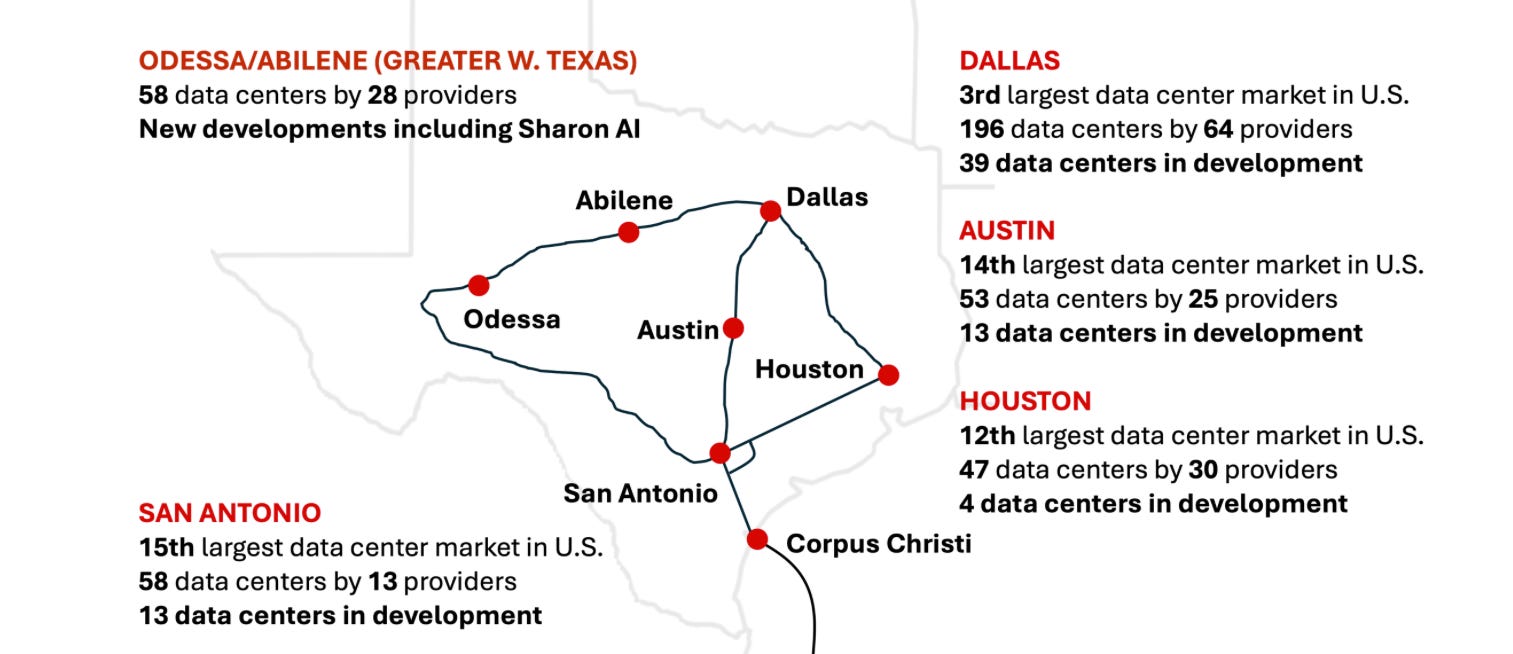

Texas is becoming AI infrastructure ground zero, with 395 data centers operational or in development, only 2nd to Virginia as hyperscalers look for power close to the natural gas abundant in the permian.

West Texas in particular is seeing an a pickup in DataCenter development. NRG and LandBridge are constructing a 1.1GW Data center in Reeves county, within 100 miles from Odessa. Australian NeoCloud SharonAI is building a 400MW data center in Odessa. Microsoft recently contracted out to nScale a 240MW data center in Texas, to be constructed at an unknown location. OpenAI is building the StarGate complex in nearby Abeline Texas. 58 data centers are currently in development in the Greater W. Texas area.

Why West Texas? The region offers the cheapest natural gas in America (possibly, the world), cheap available land, and fiber connectivity. Perhaps even more important is what it lacks: state taxes, excessive regulations, or local govts who care about noise pollution. As Odessa Oil producer Kirk Edwards put it: “ “No other region can compete dollar for dollar with West Texas when it comes to fueling energy-intensive data centers with abundant, low-cost, clean-burning natural gas.” With all these data centers coming online in Odessa, the potential to contract 370MW of a carbon-free plant already in production starts to sound attractive, at least as a component of a larger project.

A PPA for Project Permian would accomplish three things: 1. solve then financing gap without dilution, 2. validate the Allam Cycle technology, and 3. open the door for NetPower to pursue additional projects in net new natural gas build outs or through retrofits of existing natural gas plants.

We see NetPower reaching $6-$8 on a PPA announcement, with potential tail outcomes to $10-$15 driven by commercial adoption. This is similar to outcomes that recently played out in the AI-adjacent energy space including Bloom Energy and Fluence.

Risks:

- While the project appears to be moving in the right direction timeline wise, a delay is always possible (as is the case with any first-of-its kind infrastructure project

-8Rivers, who exclusively licensed the core tech to NetPower has made insider sells. 8Rivers is structured as an LLC with investments across various clear energy technologies so this may be portfolio management instead of a lack of conviction

- the AI capex “bubble”/data center build out could crash before Project Permian comes live (for now current Mag 7 commentary suggests capex is accelerating, not slowing)

Next catalyst to watch: PPA announcement, likely within the next 2 quarters as West Texas data centers progress toward operation.

Disclosure: Author is long NPWR shares. Not investment advice - just ideas that seemed brilliant at 2am. Do your own research.

Full port