CM#2: Does money grow on trees?($TREE)

Why the current macro leads to an opportunity in LendingTree

The market the past few weeks has not been an easy environment for longs. With Trump tariffs, declining consumer confidence, and recession odds up to 50%, this may seem like an odd time to highlight LendingTree, a business focused on consumer lending. However, this is a business that is executing, cheap, and benefiting from a potential bull cycle in consumer credit. (Disc: I am long)

What’s going on with the economy anyways?

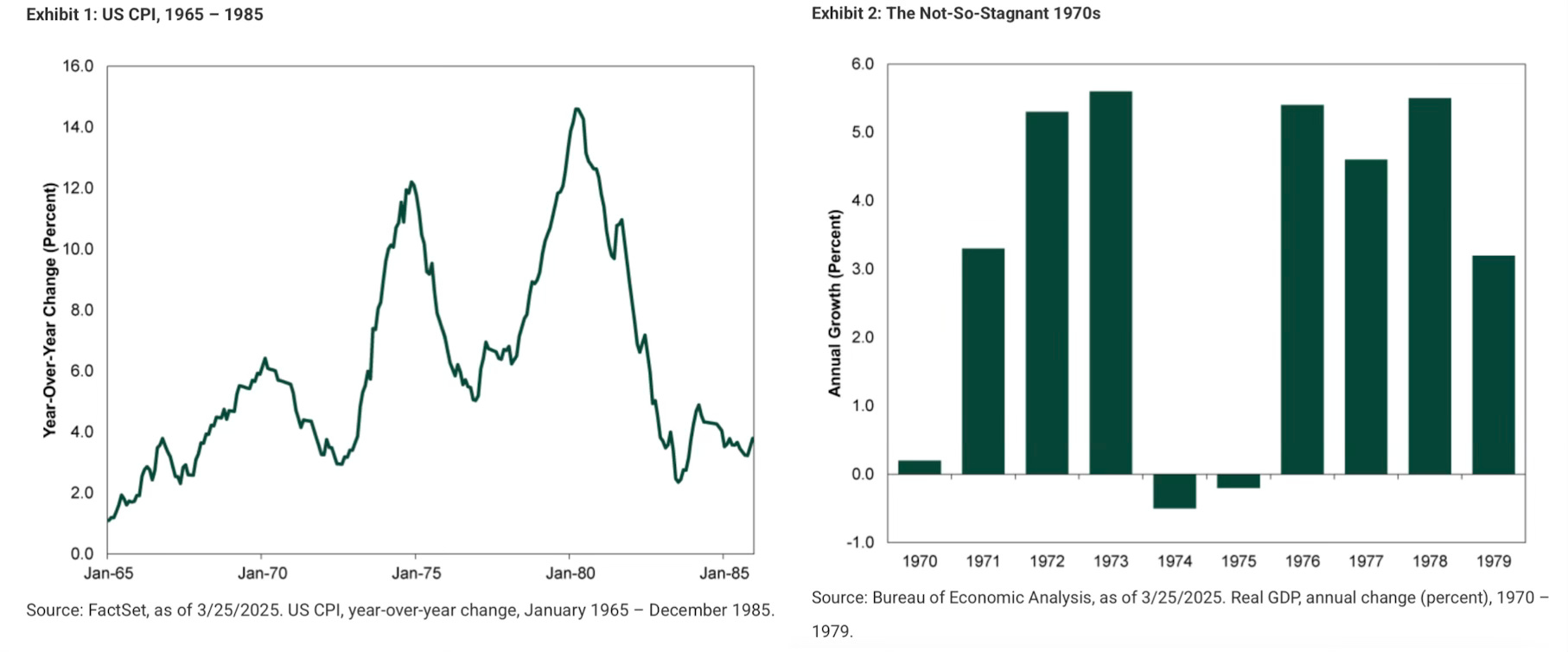

Will we enter a recession? Will the consumer break? I am not an economist, but those are questions the 19 members of the FOMC study in detail. The median FOMC member does not expect the economy to enter recession, but sees an environment with lower GDP growth, slightly higher inflation, and slightly higher unemployment. And while it can be described as “mini-stagflation” scenario, it’s not the same as the 1970’s. In 1974-1975, we had 10%+ CPI and negative real GDP.

A 3% CPI and a 1.5% real GDP, that the more pessimistic members of the FOMC may assign, is not a recession or even necessarily a “bad economy”

As Jerome Powell put it “it's not that inflation is really high, it's not that unemployment is high. It's none of those things. We have, you know, 4.1 percent unemployment, we've got 2 percent growth, and you know, it's a pretty good economy. But, people are unhappy because of the price level. And I do, we completely understand and accept that.”

In other words, we could be entering a 2022-style “Vibecession” but not a true economic downturn. One reason: tariffs “apply only to wholesale costs at the border, and US goods imports make up around 12% of GDP.” In most industries, goods are sold retail at a “keystone markup” of 2x the wholesale costs. When you see a headline “20% tariff” you can usually divide that by 2 to get the actual price increase a consumer may face. At the margin, goods still get more expensive and consumers buy less. The FOMC is pricing this in by predicting a -.5% decline from current GDP Growth levels into the end of the year.

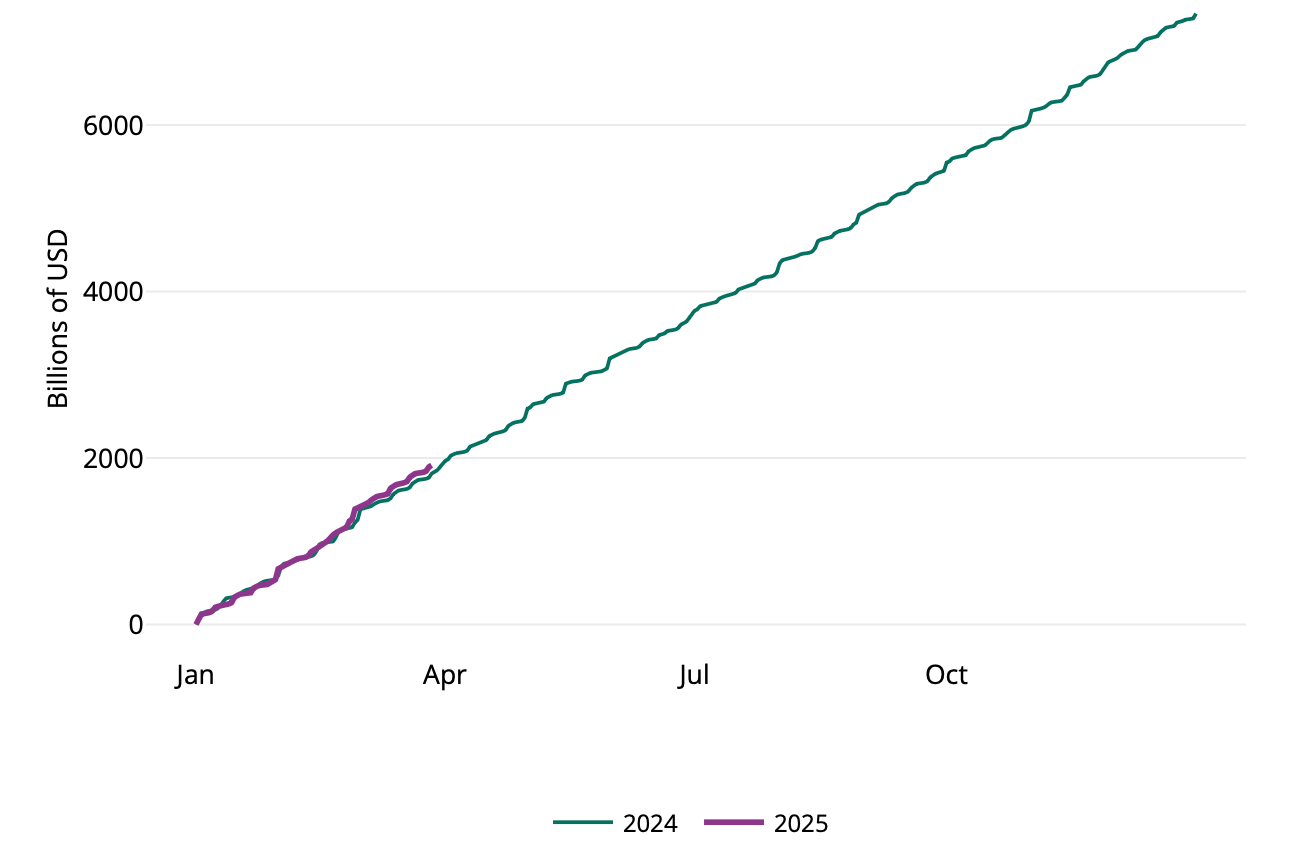

The other dynamic is government spending. While DOGE has made a lot of headlines about cutting billions in federal spending, real-time tracking by the Hamilton Project shows federal spending up 5% YoY (~$100B)

While spending on US AID is down ~$2B YoY, this is significant compared to things like Medicare prescription drugs (~up $11B YoY).

While congress could change this with major spending cuts, current proposals (tax cuts) and Trump’s general rhetoric (using proceeds from DOGE or tariffs) to not repay the debt, but to distribute as consumer stimulus) suggests the deficit will not be meaningfully cut in 2025.

Why consumer lending can go higher?

Having outlined the Fed’s expectations and examining the tariff and DOGE impacts, here is a plausible economic scenario for 2025:

Products get more expensive, growth slows but is still positive YoY. The Fed cuts 2-3 times. The consumer does not pull back significantly on spending, but feels pinched at the margin.

In this scenario, the consumer may turn to consumer lending to fill the gap. This could include credit cards, BNPL (Affirm, Klarna), or direct lending.

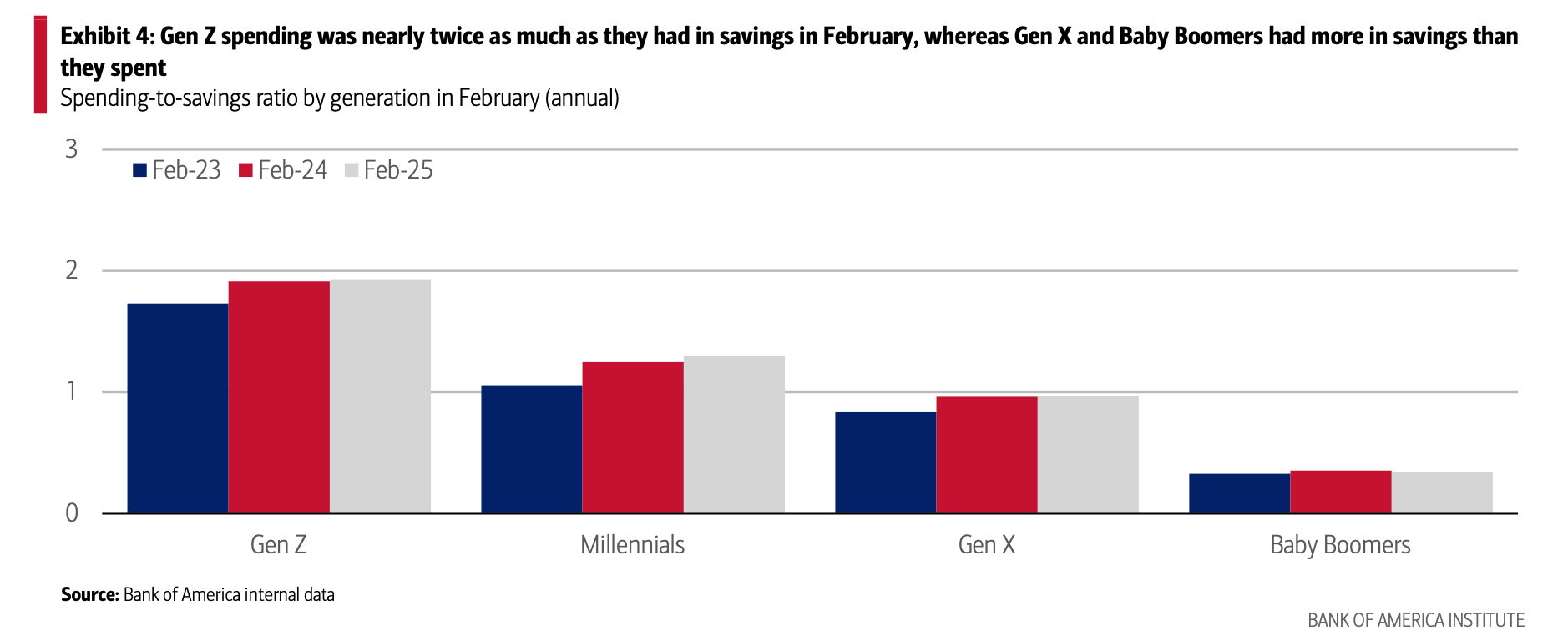

How can this work? Consumers are still less levered on their household balance sheets than they were before Covid. The stimulus checks helped to reset consumer’s debt levels. As interest rates decline, consumer debt becomes more affordable. So consumers, if pinched have room to take on more debt, instead of pulling back spending. There’s also some generational factors here: Gen Z has bad spending habits.

So there’s the thesis, consumer spending slows but doesn’t break as consumers have an available well of consumer credit they can tap. This will break eventually (2026? 2027?)- but what if there was a business that was profiting on this trend, without taking on credit risk? Introducing LendingTree.

What is LendingTree?

LendingTree ($TREE) is a recognizable business for most consumers, but as a public equity is under-covered. It’s not a new business, having first gone public during the dot-com days. Its market cap is under $1 billion and its stock is down 60%+ in the past 5 years. This is what creates the opportunity, as LendingTree has been through quite a turnaround in the past the two years.

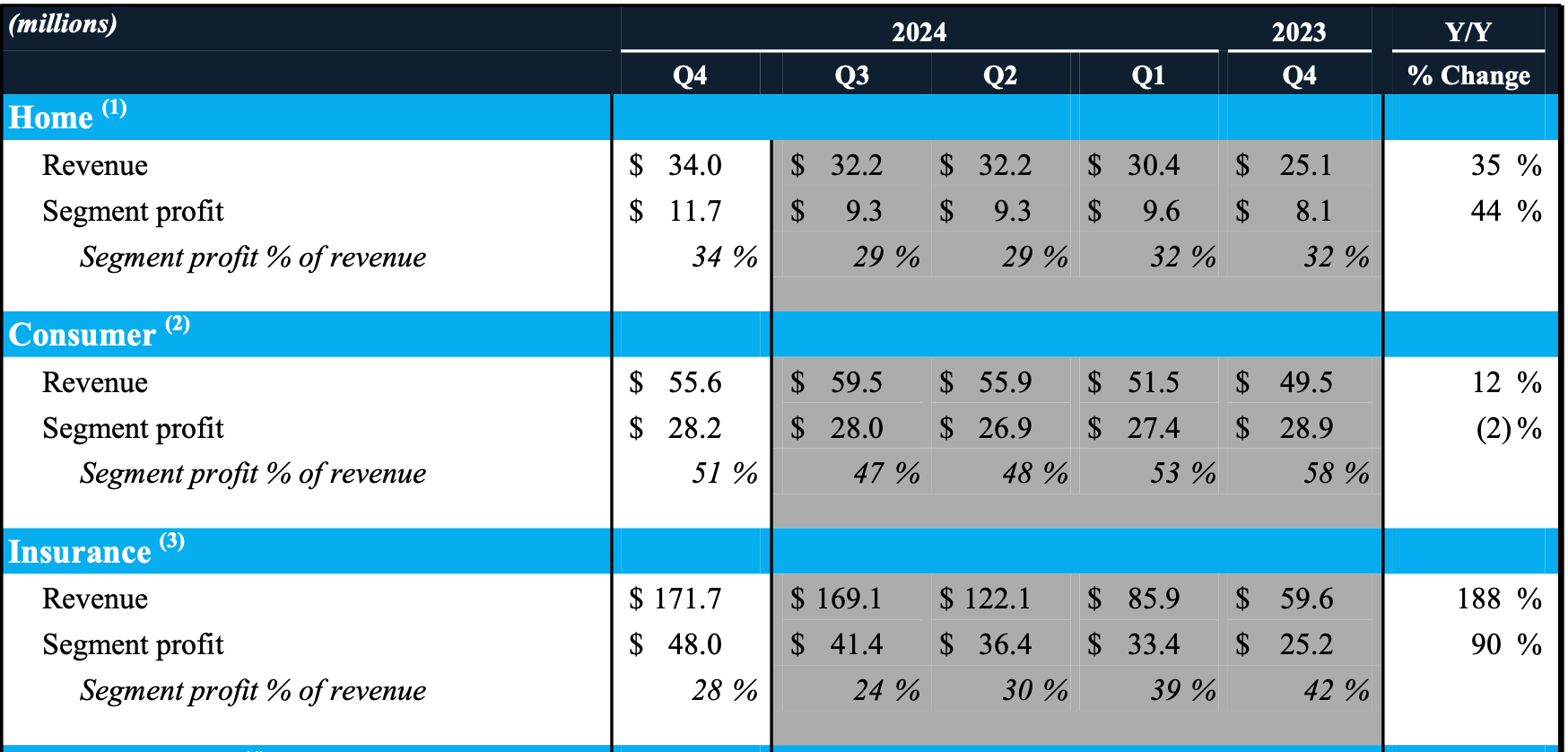

At its core, LendingTree is a marketing platform, having more in common with Nerdwallet than a Rocket Mortgage. LendingTree offers a marketplace for consumers to compare providers across their three segments: home lending, insurance, and personal loans (inc. SMB). LendingTree has 430 “Network Partners” who provide the loans. Consumers will fill out their basic financial information and LendingTree will get paid for matching the consumer to a network partner.

How are these three segments doing? Home grew revenues 44% YoY and profit 44% YoY. Insurance grew 188% YoY and profit 90% YoY. Consumer is LendingTree’s most profitable segment (51% gross margins), but has lagged with segment profit down 2% Y/Y.

For 2025, LendingTree gave the following guidance: Our full-year 2025 outlook assumes double-digit revenue growth in both the Home and Consumer segments, with more modest Insurance segment growth following a record year.

Insurance

This higher 10-year environment has been gold for insurers and insurance companies have found they now have extra dollars for marketing spend that they didn’t have previously. Insurance premiums have also gone meaningfully higher, making consumers more apt to compare options.

We don’t need to speculate who these insurers are. Per the 10K: “For the year ended December 31, 2024, two Network Partners, Progressive Casualty Insurance and Allstate Insurance Company, accounted for 22% and 11%, respectively, of total consolidated revenue”

Management expects moderate growth in this segment in 2025 per their Q4 earnings:

"Almost all of our carriers are still in a growth position with us, and they've made that pretty clear to us [..] So definitely, we still expect insurance to be a really good story in '25. As the year goes on, I think you're going to see that growth moderating.”

Progressive and Allstate have presumably communicated higher spend, but this segment does have tough comps (as any segment with 188% YoY growth would.)

Home

LendingTree offers comparisons of mortgage loans and home equity lines of credit. The double-digit guide for 2025 does not take into account lower interest rates:

Per LendingTree’s CFO: “Jed, I'll just add on to that. As it relates to the guide for home, we're not contemplating any material reduction in rates. We're kind of assuming basically the rate environment that we are in today. What we're basically assuming in the guide is a continuation of the strength in home equity”

While mortgages are down, home equity lines of credit have been popular in this environment, offering later rates than credit cards or direct loans, but requiring valuable collateral (your home).

The COO added: “from a consumer standpoint, I think it's also the scenario of with very little buying and selling of homes and with the equity that the consumers are sitting on, the homeowners are sitting on specifically, just keep going up and up, they're going to want to to remodels. They're going to want to consolidate debt. They're going to want to go on vacations. And so it's like they're -- it's still the best interest rate product compared to all other lending products”

Consumer

On consumer, management expects double digit growth. By sub-segments, credit card is “rough,” SMB is on a “strong growth trajectory”, "Personal loans, that one has been growing well for us, grew 20% […] “that category is like -- the credit boxes are still pretty tight. But as long as you can find the consumers that meet those credit boxes, they're -- our clients are very actively telling us, "Bring them on."

The bottom line is: “interest rates are still a little high, but you've got a lot of consumers out there that are looking for lending options.” The guide again does not take into account lower rates, but if rates do go lower this is a segment that can pop.

Other factors

LendingTree has benefited from shifts in the insurance market, but why has their growth turned around in other segments? One reason was a shift in Google SEO:

“And on the SEO and organic traffic, call it, 15% to 20% of our traffic is organic. SEO is a piece of that. The rest would obviously be people hearing us and typing us in, et cetera […] in terms of the Google algorithm change, what I've noticed Google doing, and I, quite frankly, agree with it, is they are giving more credit to high-quality, unique content that really aids the consumer. So they did things like shutting down the"marketplaces" in -- of newspaper sites because they basically were leveraging their credibility on the news to go sell jackhammers and screws or whatever and mortgages. […] LendingTree has always been unabashedly in the paid marketing camp, and I've wanted our SEO side to work since 1999. I would say for the first time, it's really gripping.”

Google decided that LendingTree had higher credibility than Forbes Advisor, CNBC Select, and the other media sites that advertise loans, insurance etc.

Valuing LendingTree:

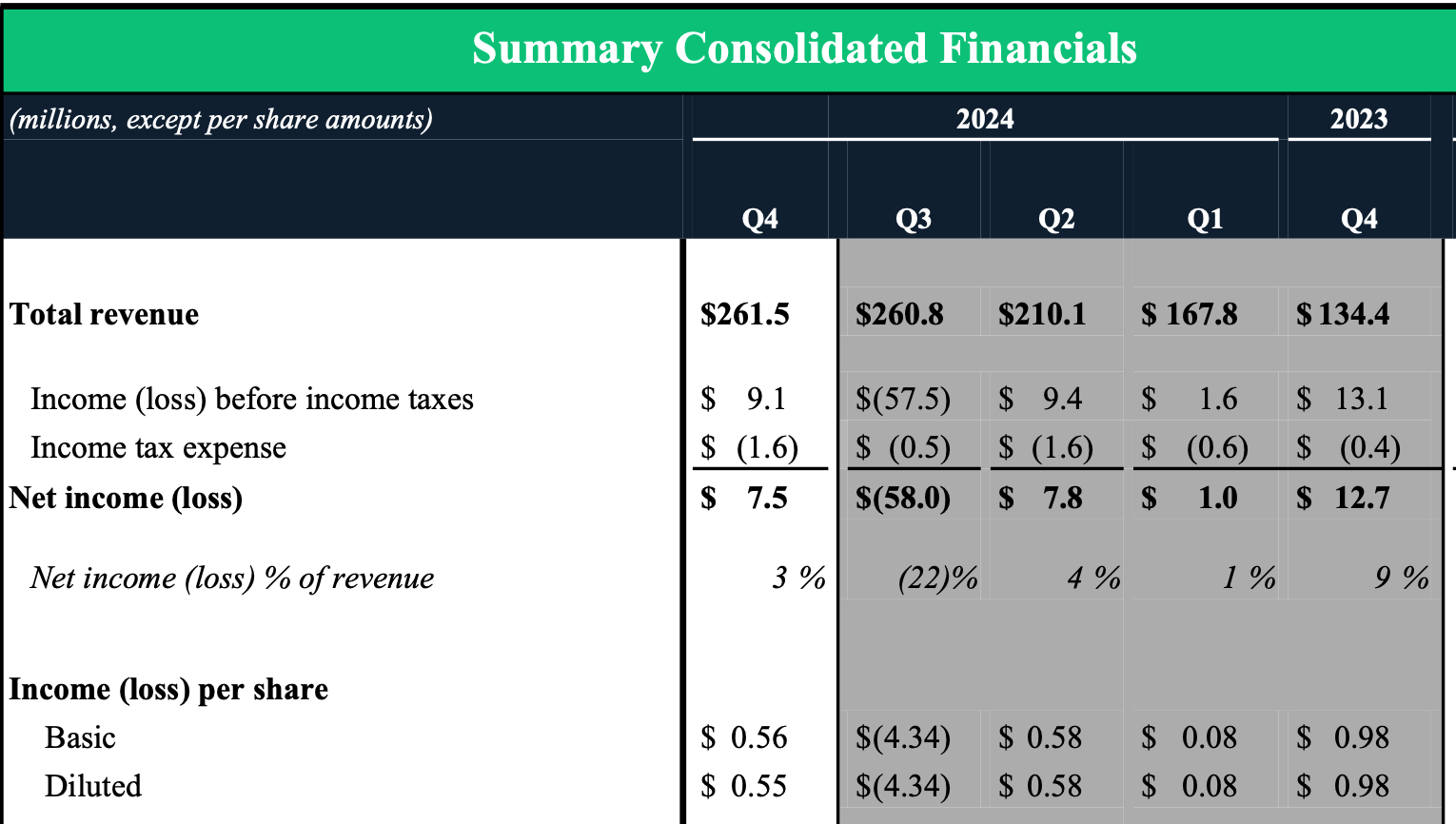

LendingTree grew revenue 12% YoY and is guiding to ~8-9% YoY growth this year, with this year’s cut not pricing in rate cuts. But is it profitable?

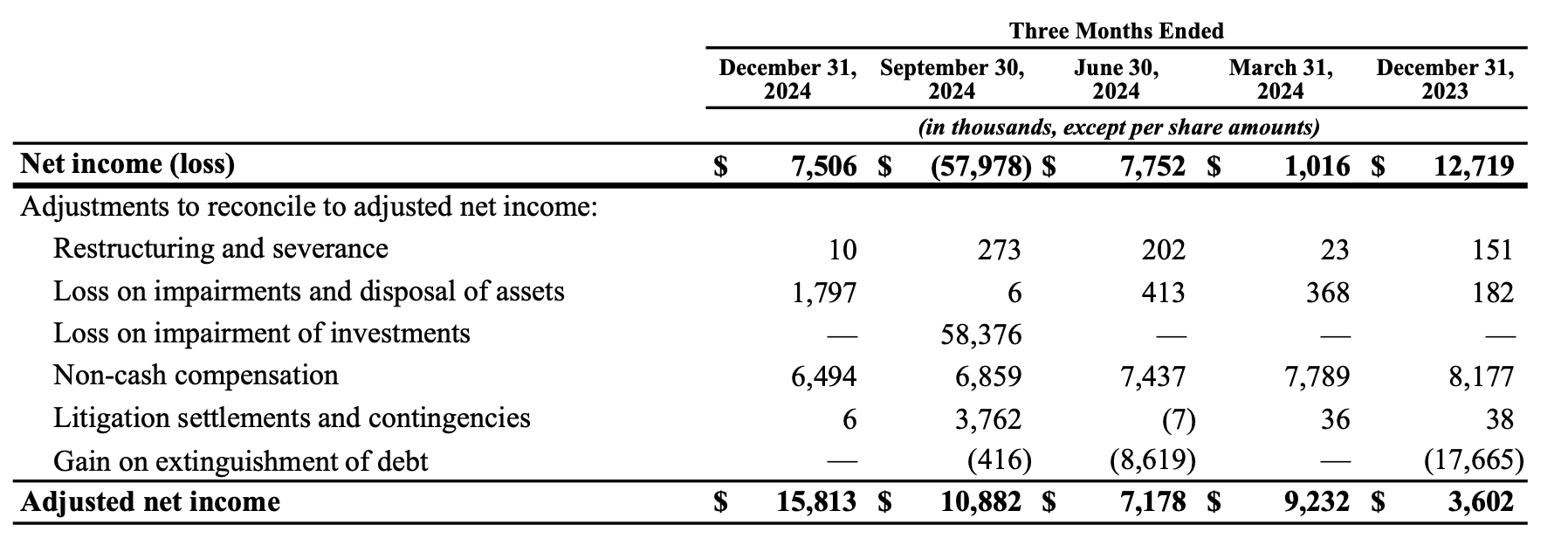

It wasn’t on a TTM basis, but this is misleading: Q3, was mostly a goodwill impairment towards LendingTree’s 2020 $80 million investment in Stash. LendingTree is not expecting any new investments in the near future. Another question is why revenue has doubled YoY but EPS has halved from Q423. This is also misleading:

The Q3 23 had a large gain associated with an Apollo debt. The latest Q4, with the $.55 GAAP EPS and few one-time adjustments, its a more accurate reflection of the earnings power moving forward.

As revenue increases 8+% next year and they continue getting more fit (notice the $1.5M reduction in SBC from 2024 to 2025), you can see a path to $0.9 - $1.0 GAAP EPS. That’s roughly where the analyst consensus is at:

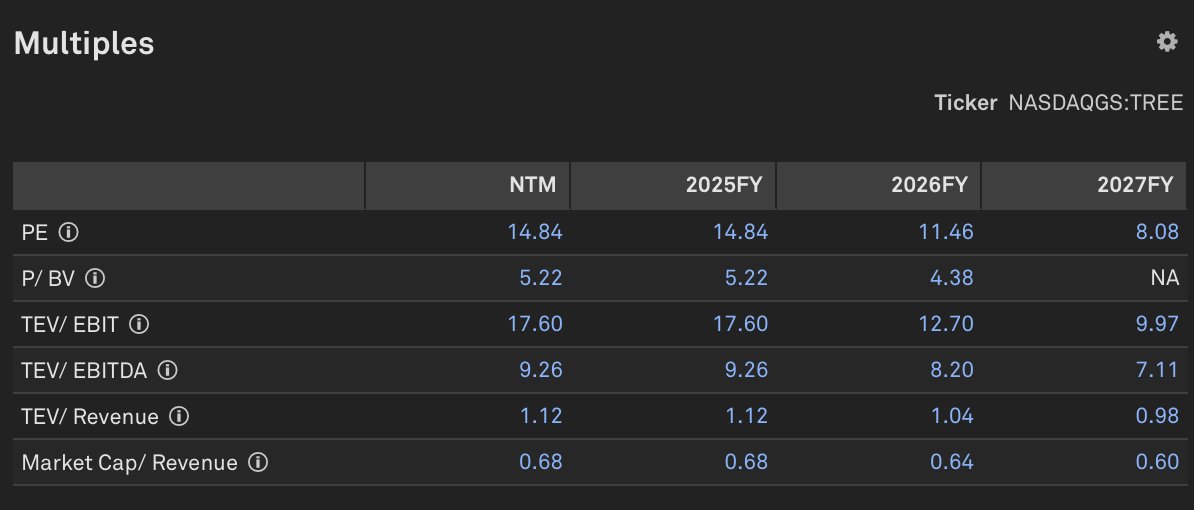

You’re looking at NTM 15 PE, 9 EV/EBIDTA, and 1.12/Revenue, multiples generally below market averages. The current growth profile should argue for a higher valuation. Debt is high but at 5x Debt/Ebidta, but improving.

These multiples would make more sense if valuing a financials business. While this is exposed to similar cycles as financials, the business model itself does not involve consumer credit risk. The CEO (who is also the founder), has been through multiple cycles (dot-com crash, great financial crisis) and has been successfully de-levering the business in the past few years.

As LendingTree starts to screen better in the next year (debt metrics, GAAP earnings, revenue growth) and if the consumer segment turns around, this could see increased institutional adoption and rerate. With only a 10M share float, it doesn’t take much for this to move fast. You’re also starting to have some insider buys, most recently the COO buying 5000 shares in the $41-42 range.