CM #4: The next ad giant is McLovin?

Why Applovin can be $500B company

AppLovin might be most controversial name on Wall Street bar Carvana. Short Sellers have chimed in from Muddy Waters, FuzzyPanda, Culper Research. The main reason is the financials seem too good to be true:

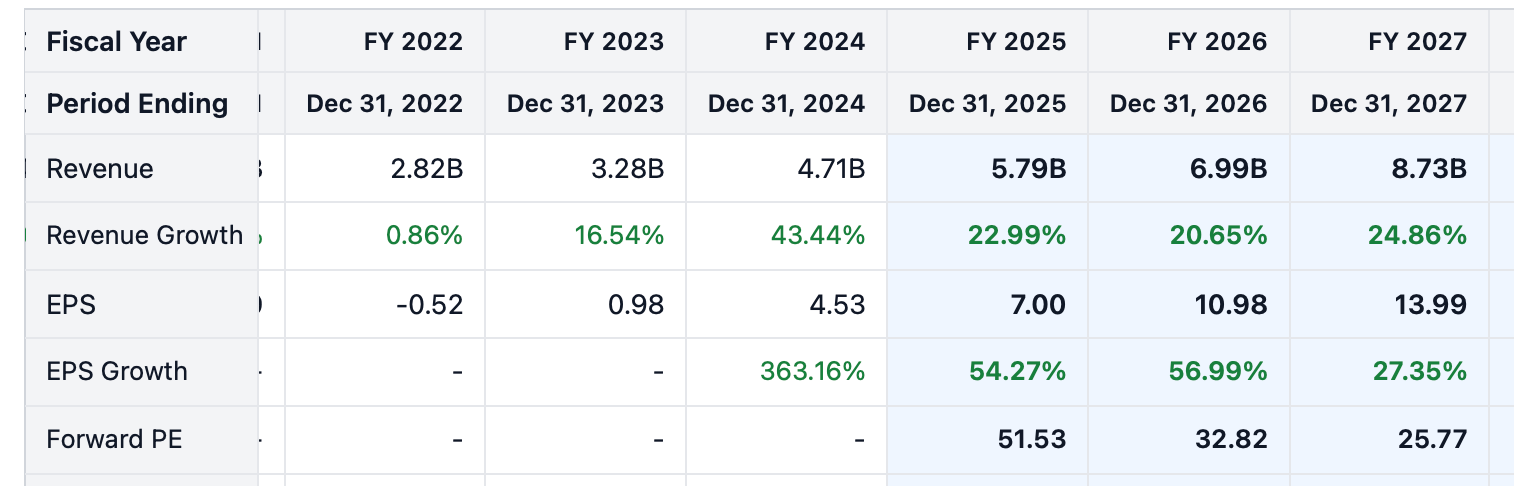

In fact, the financials are better than the entire software landscape. AppLovin scores a rule of 66 - even with share-based compensation factored in. That’s higher than PLTR, PANW, and MNDY. This puts APP in the highest caliber of growth stocks.

At the same time APP is trading on more reasonable multiples than its high-growth peers: for reference APP trades at 25x 2027 PE.

Compare this to PLTR, which despite similar expected growth #’s is at a 135x 2027 PE

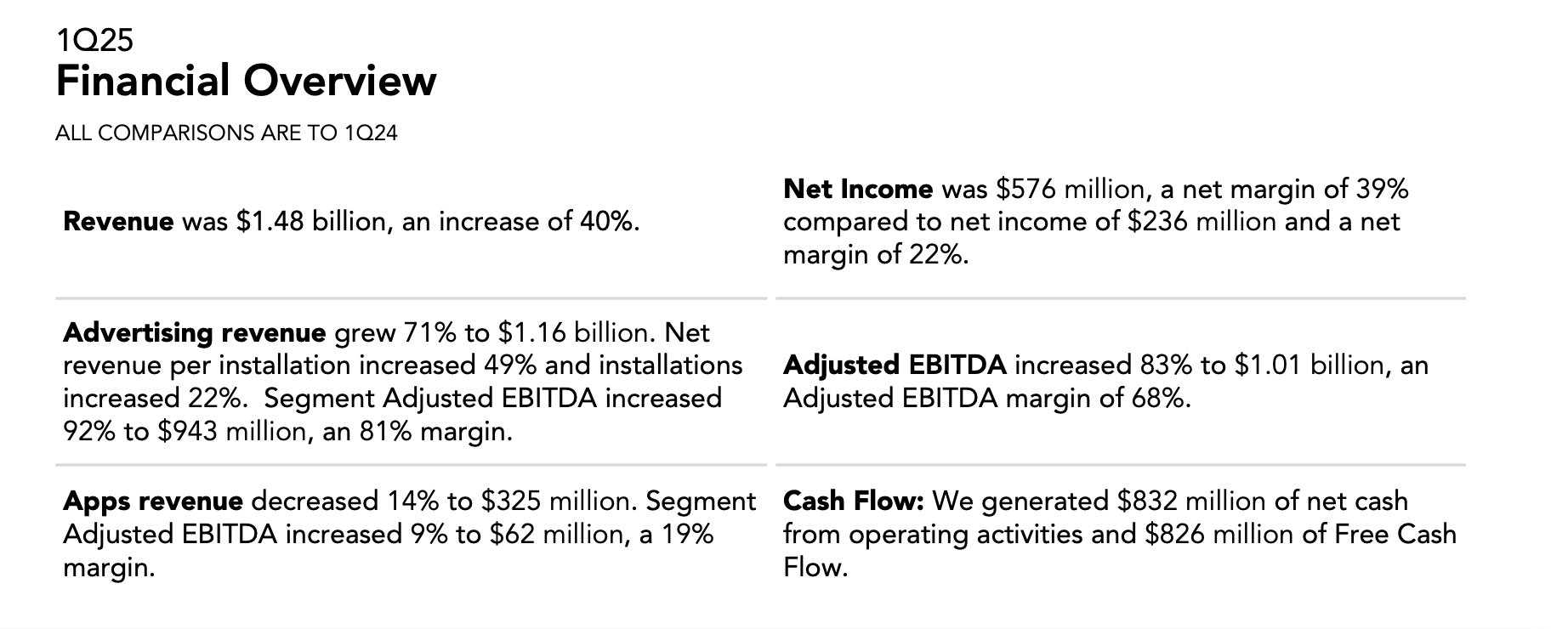

Also did you spot that revenue acceleration in 2024 for APP (17% → 43%)?

They did it with less employees than the year before!

The Applovin Debate

The key points of the story here:

Applovin was the primary advertising platform for games to advertise to other games

Applovin recently expanded into e-commerce ads within games

Somehow Applovin performance in those ads is ~90% as effective as Meta targeting

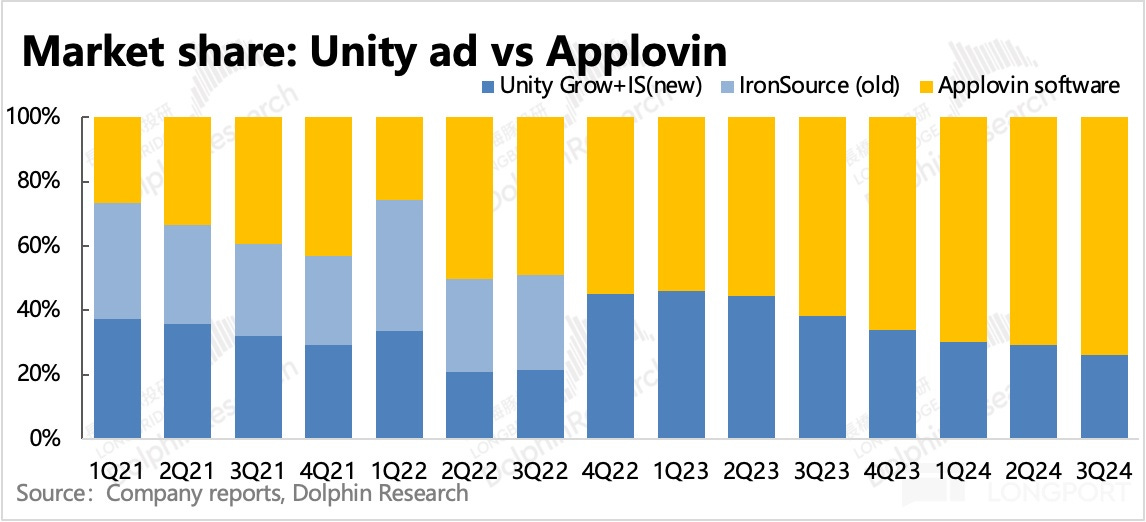

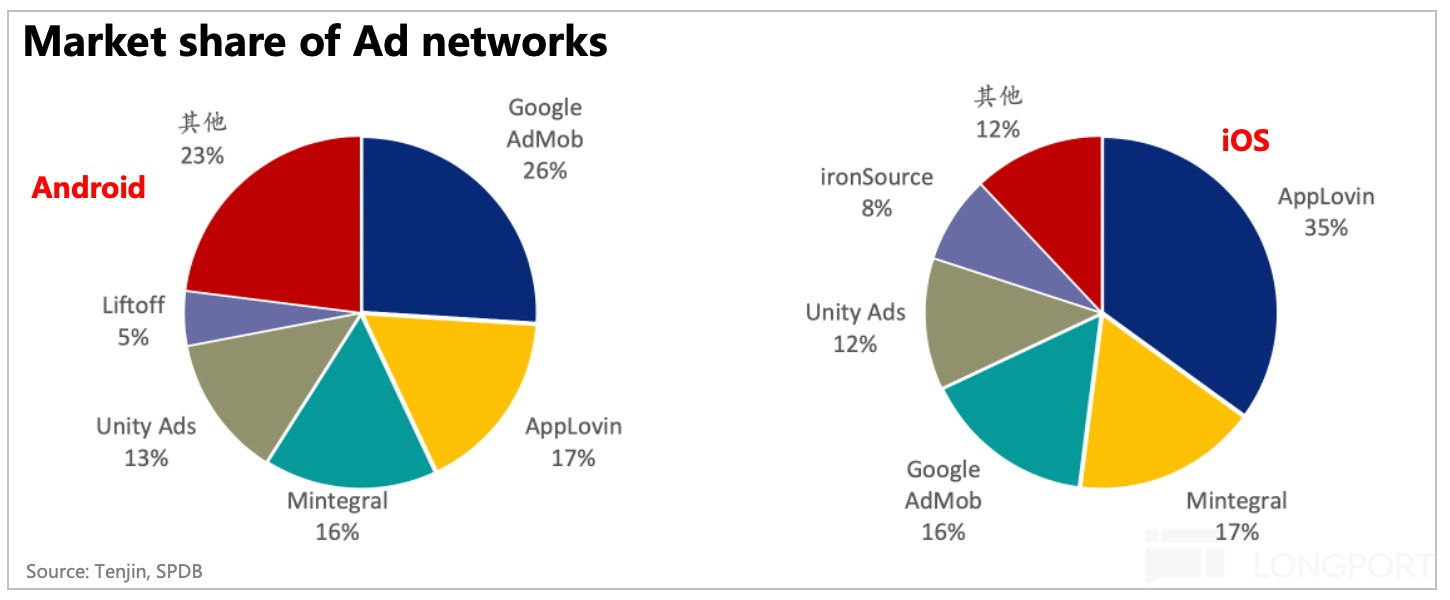

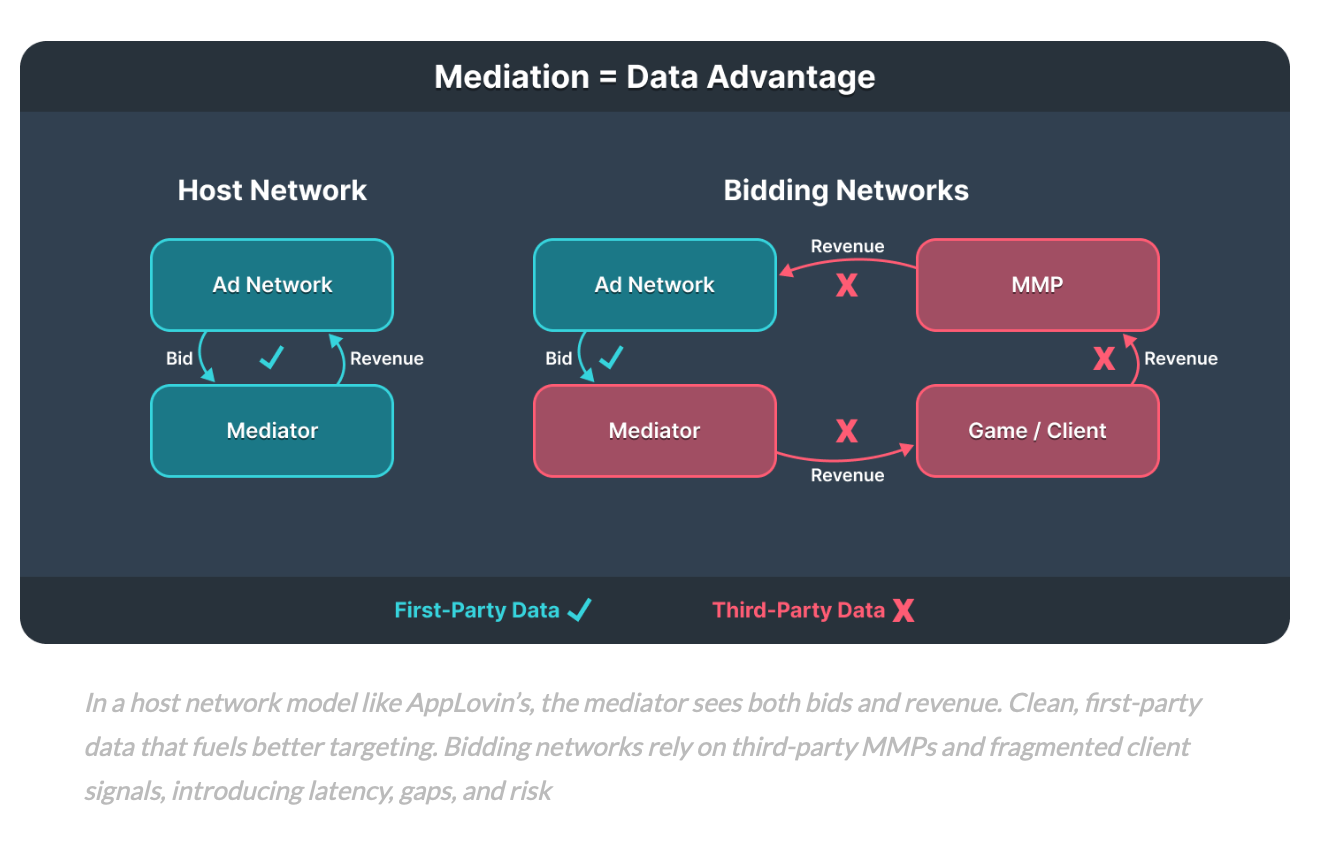

Even bears will admit to Applovin’s dominance on mobile game advertising. This is a market that Applovin won effectively from Unity (who were mismanaged). AppLovin was able to be early to the real-time bidding model for ads.

Bears are happy to admit Applovin’s dominance here as the mobile ad landscape isn’t glamorous. This starter pack is a good overview of the ads that are popular:

The “interactive elements” and small X’s serve to drive clicks which send users to the App Store. Much of the ads have more in common with the pop-ups that you would find on an illegal streaming site instead. An aggregator of these ads takes different skills than typical ad platforms.

After winning dominance in the mobile game-mobile game space, AppLovin set its sights on the e-commerce and general advertising space, surprising the industry.

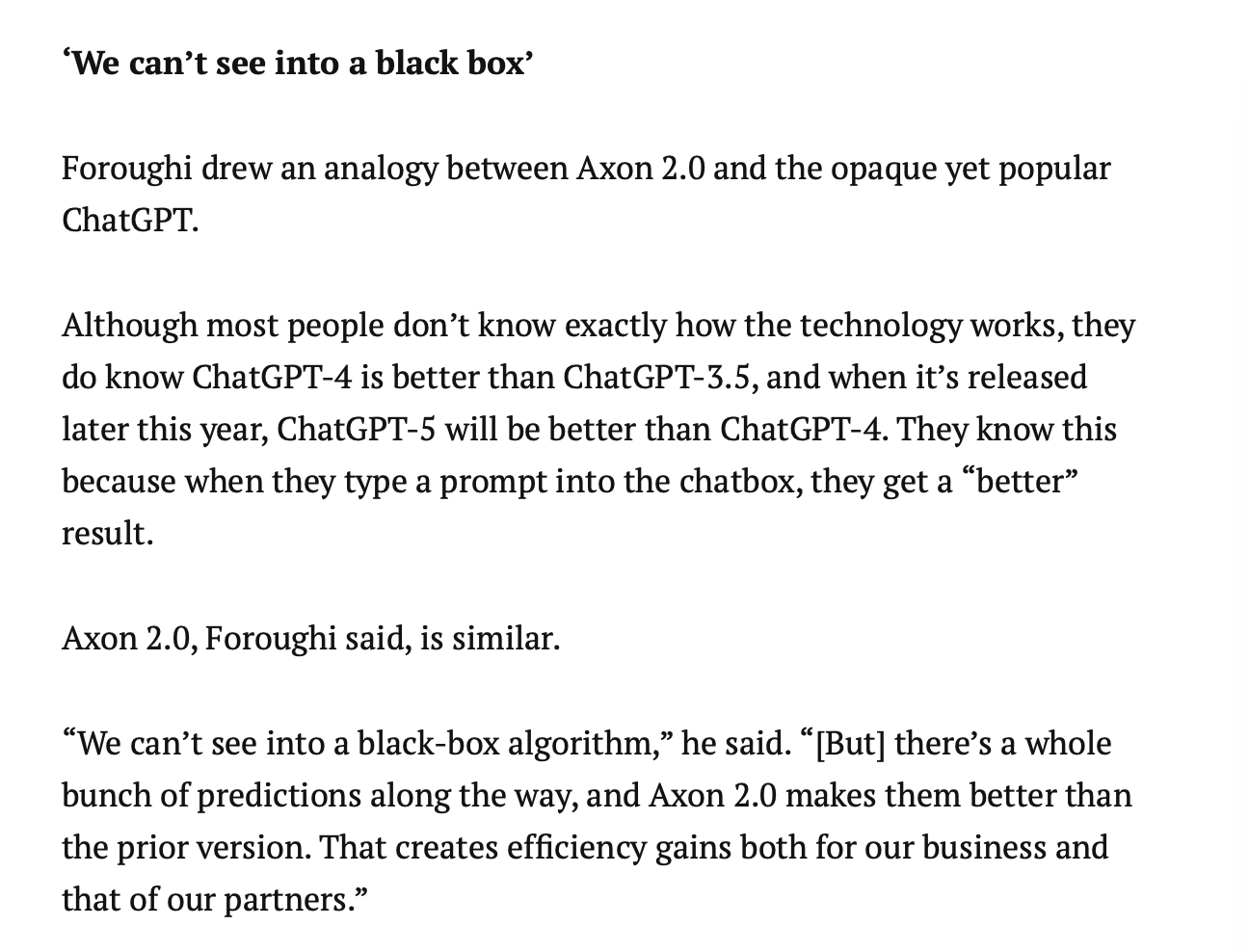

At the core of Applovin’s reinvention and the e-commerce pivot is Applovin’s “AXON 2.0 Engine” released in early 2024. Advertisers using Axon 2.0 have reported performance almost as effective as their Meta campaigns. The weird part? No one really knows why the algorithm is so effective. It’s AI?

The weird part is Applovin is a 3rd party advertising platform. They don't have a captive audience like Google or Meta or a unique source of spending attribution like Amazon. No 3rd party advertising platform should be putting up numbers like this. So short-sellers are rightfully skeptical.

Axon 2.0: Did They Steal Meta’s Homework?

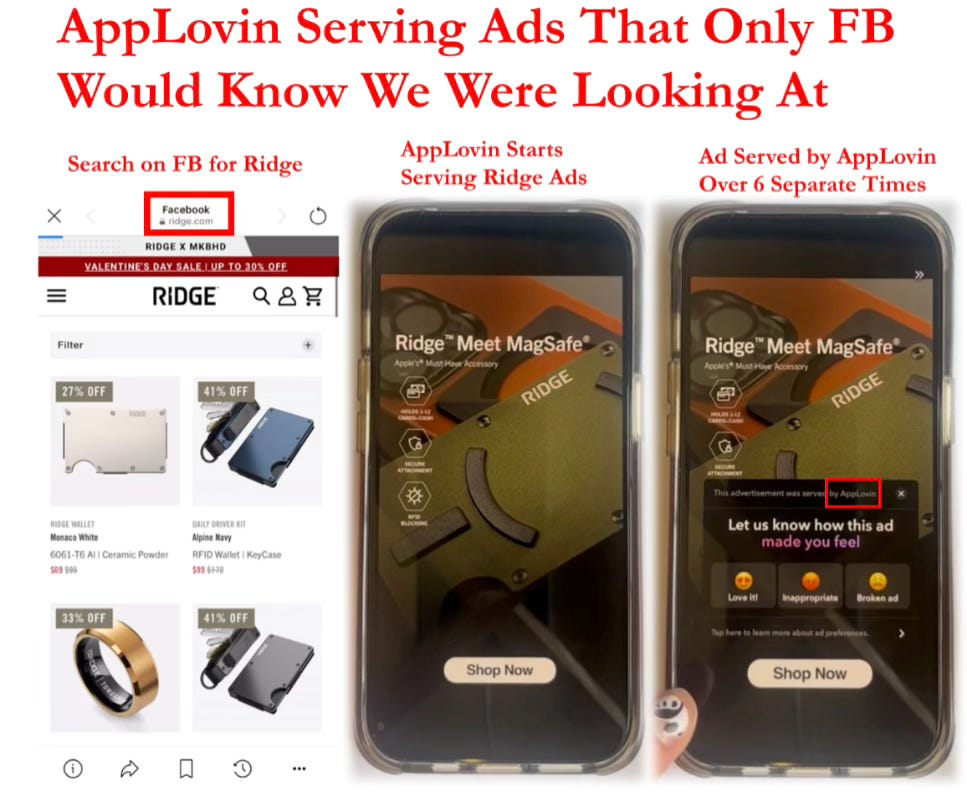

A theory from the short-sellers for the performance is AppLovin used Meta data to kickstart their e-commerce/general advertising business.

When rolling out the E-Commerce product, AppLovin required advertisers to spend $600k a month on Meta alongside AppLovin campaigns. As AppLovin has various integrations with Facebook audience networks (Facebook ad-targeting outside the apps), AppLovin could see the prices Meta was paying for ad space on its network. Combined with the $600K verified spend, AppLovin could attempt to reverse-engineer the Meta ad-targeting.

Short sellers allege this was the reason for initial effectiveness. Applovin could have used this Meta data as a base to add on third party data (cookies, website interactions) to build customer profiles and reduce their reliance on Meta over time.

This would be a smart strategy on AppLovin’s part and not too uncommon for the fast-moving digital ad industry:

But it would be a mistake to assume this is the only reason Axon 2.0 succeeded.

Axon 2.0: Advertisers Just Gave Their Data?

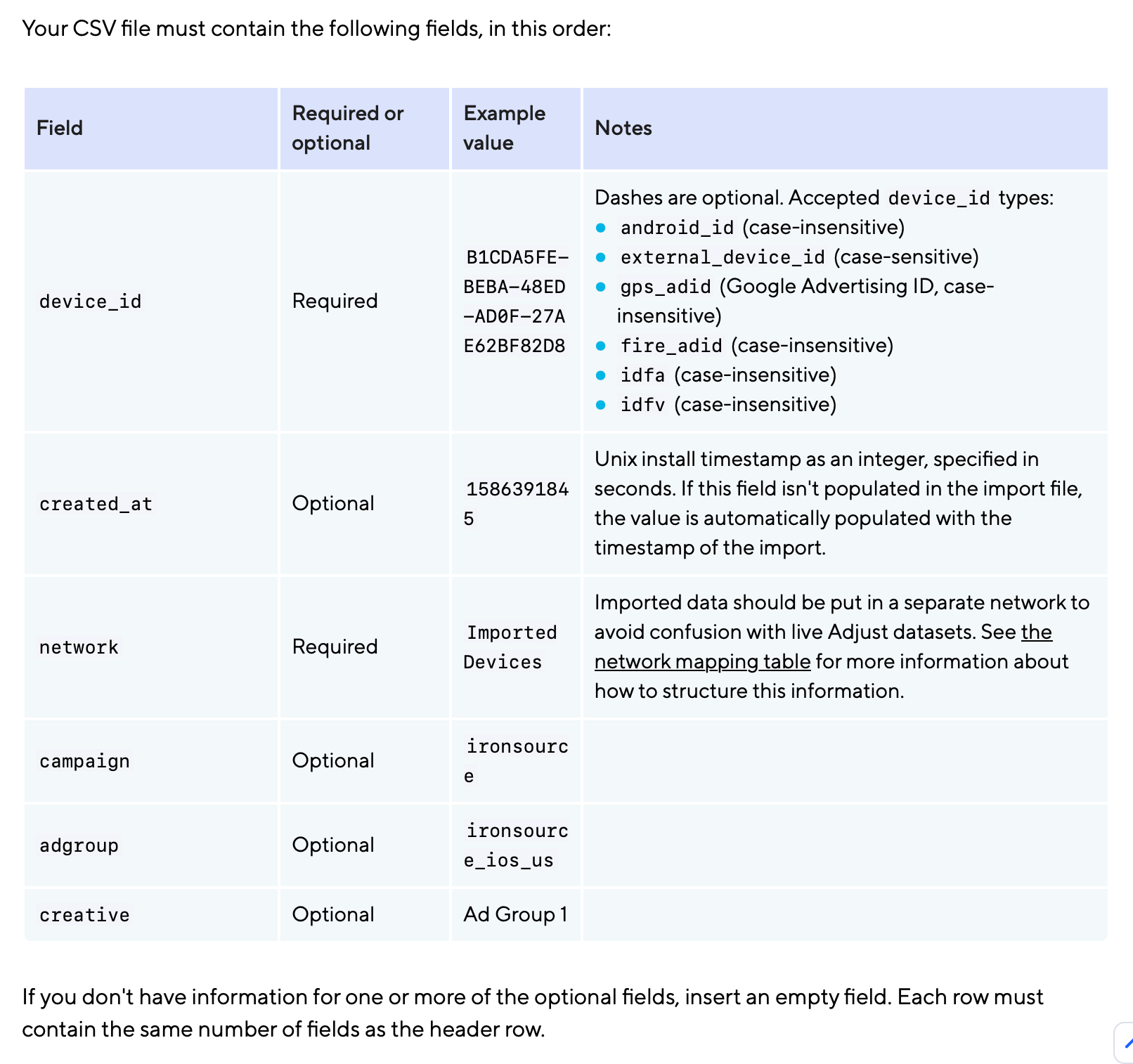

AppLovin acquired a platform “Adjust” in 2021 which measures performance across different ad platforms. Adjust is the second largest advertising data analysis and attribution platform in the world, behind the Israeli AppFlyer.

When you are switching to Adjust from another ad measurement platform, in the onboarding process, you upload a CSV with historical data for all your ad campaigns including device_Ids, networks, time stamps and ad groups.

This is an insanely rich source of data for a company like AppLovin to train their models on. So if they were getting enough CSV files, that could explain out-performance.

The Reality: Axon 2.0 Just Works

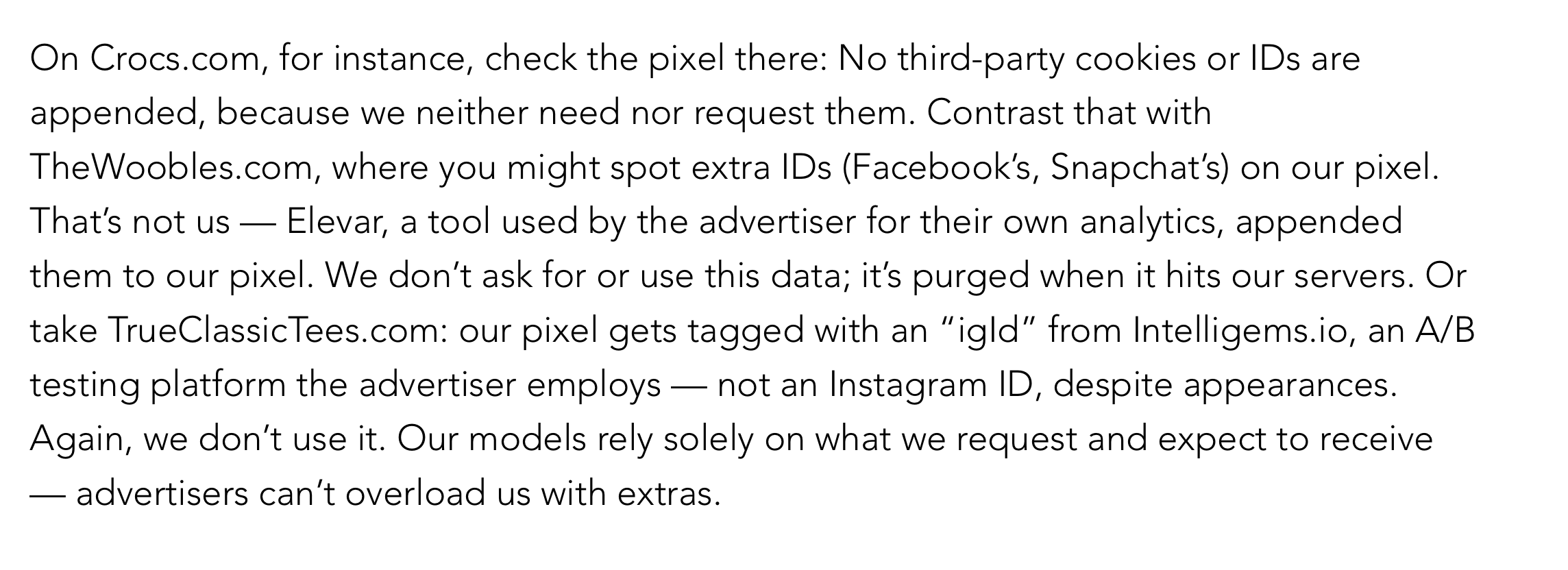

AppLovin’s CEO posted a blog post at the end of May giving a bit more detail on what goes into the Axon 2.0 Black Box. First thing: Facebook and Snapchat may show up on their pixels, but they aren’t directly going off an instagram ID

Even if a competitor tried to the same strategy, they would struggle to be effective. You need enough ad space for Meta to bid on. At the same time, AppLovin is building a moat over time through repeated interactions (which they have more of):

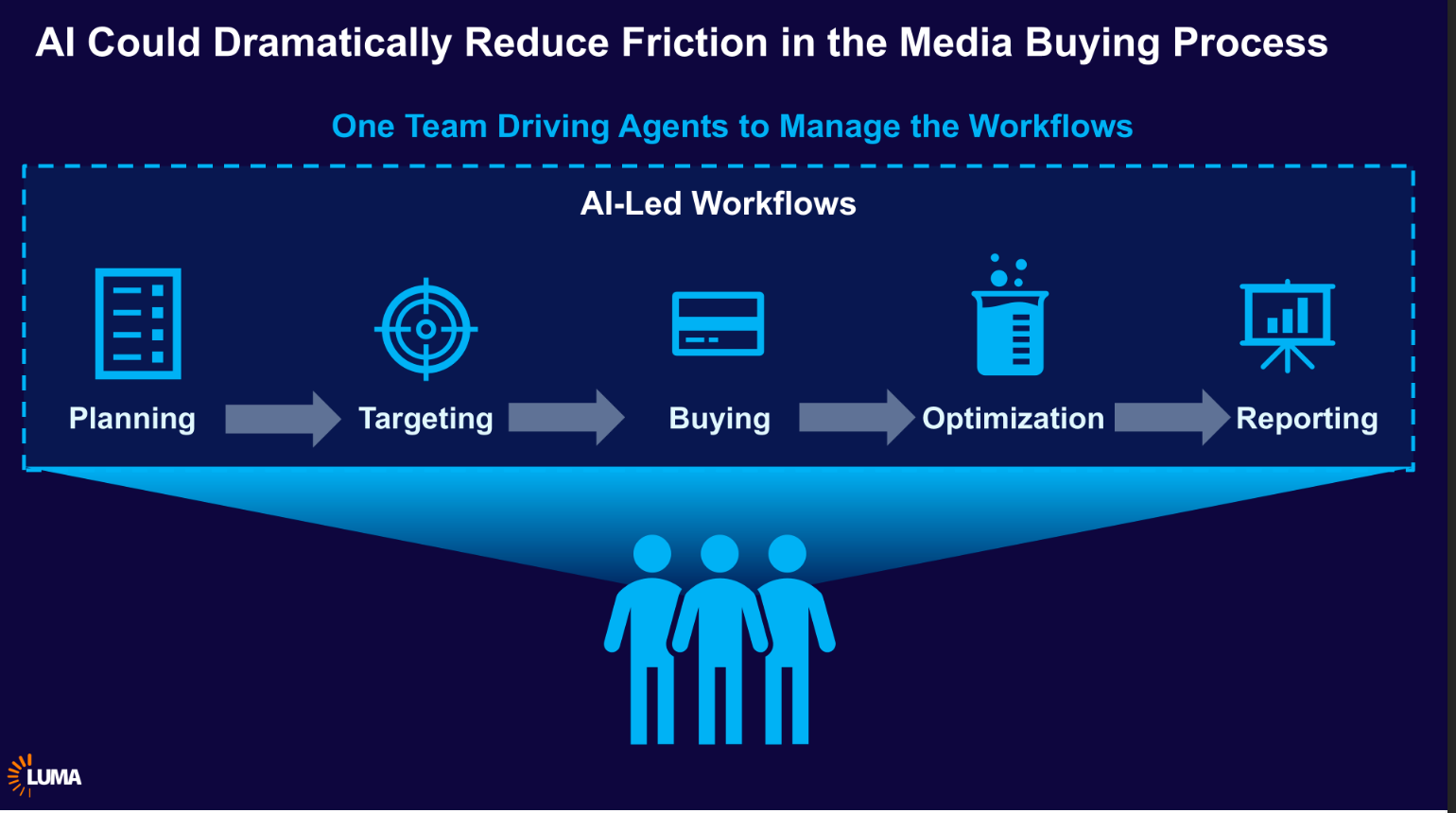

So AppLovin has mastered the art of ad targeting, but that’s only the beginning. The industry is shifting from ad platforms performing targeting only ad to taking on the entire advertising process.

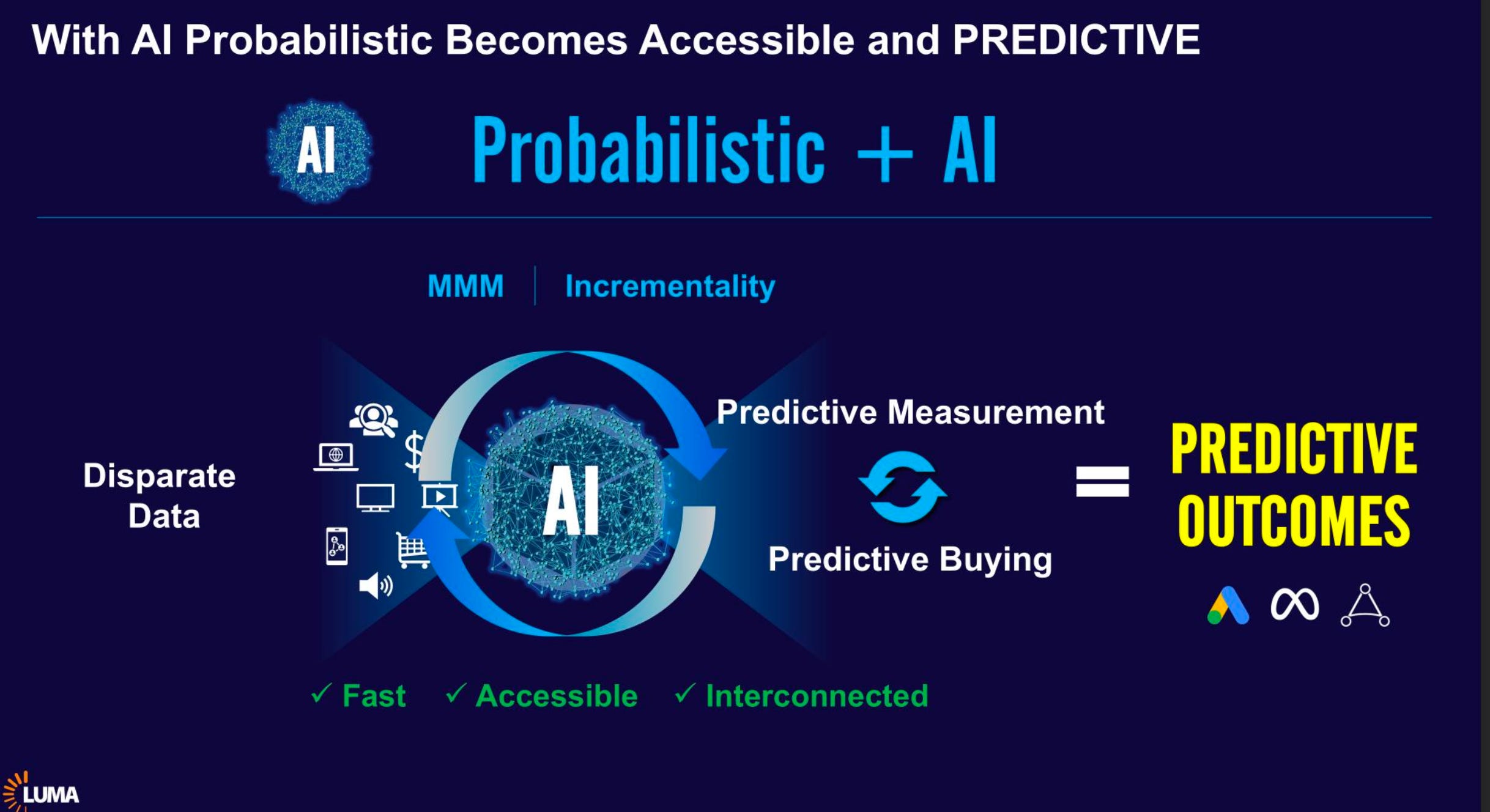

Let’s Zoom Out for A Second

Initially in advertising there was a complex work flow. You had to plan an ad campaign. Then target the ads. Then buy the ads. Then optimize the results. Then report performance. AI-first ad platforms like Google, Meta, and AppLovin have systematically taken on more of these steps.

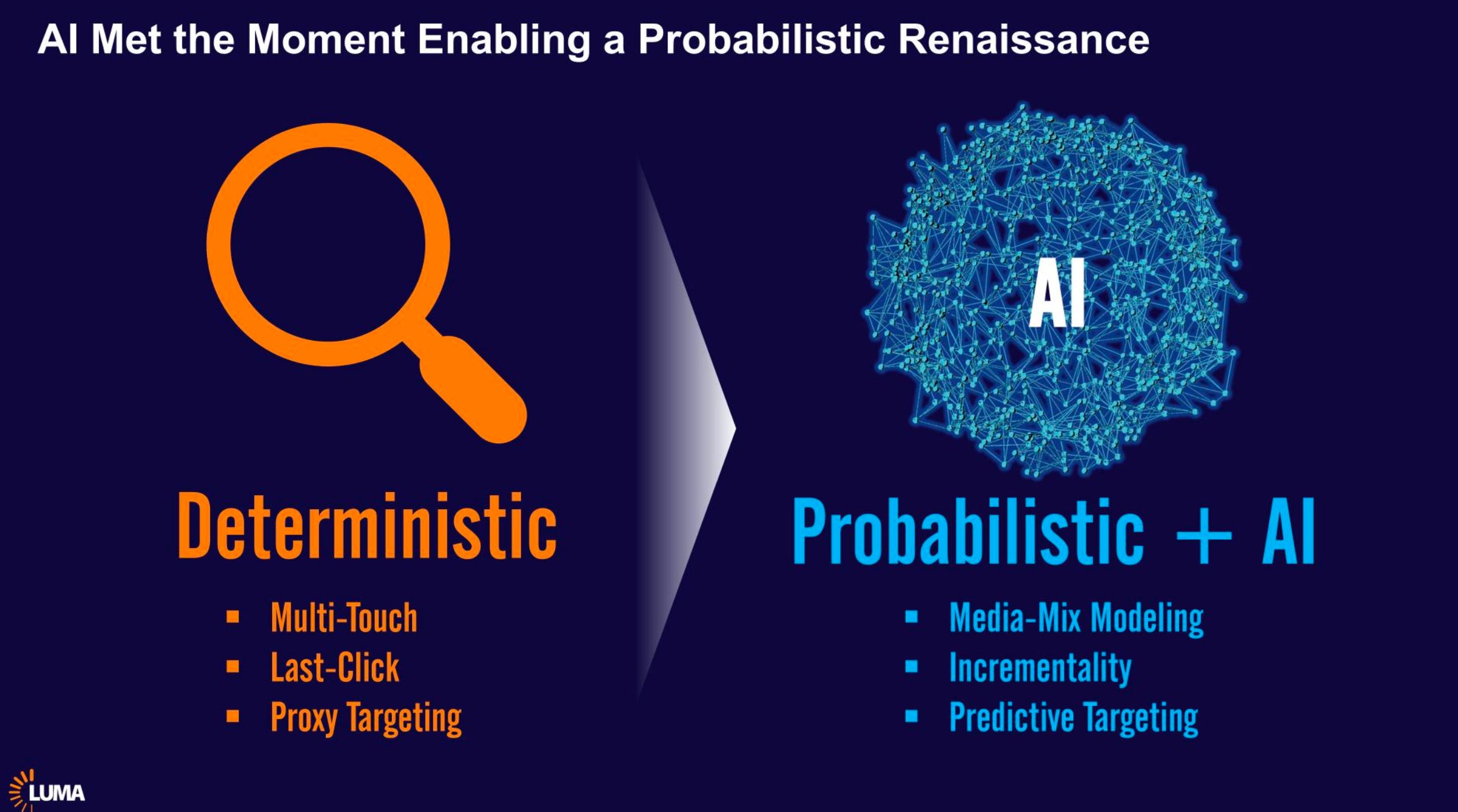

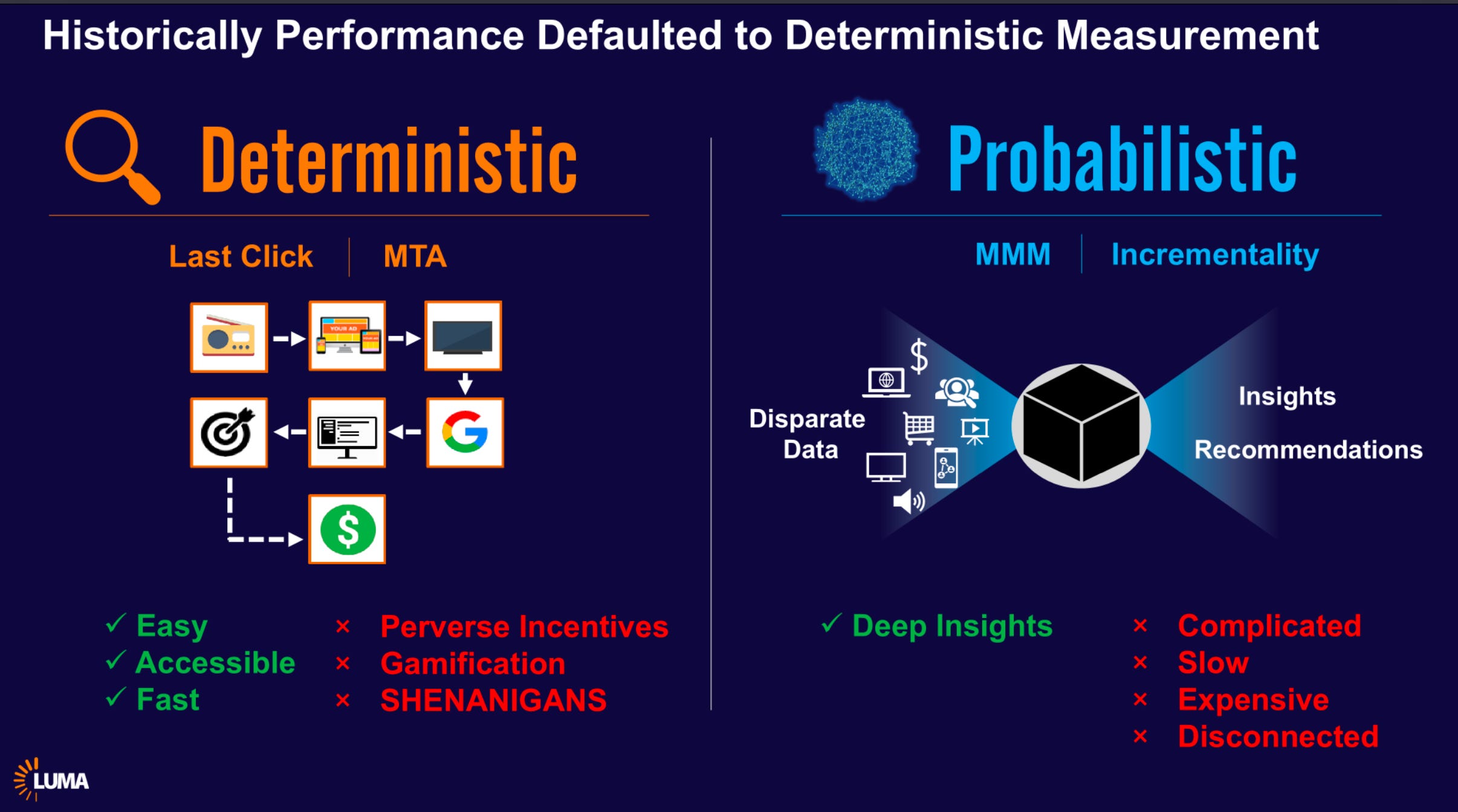

With generative AI, the platforms may even take on the ad creation themselves. Another fundamental change is the shift to attribution models. Originally, in the Google search ads model, you would use the last click, the blue link, to attribute the sale. But what if you clicked on that link after seeing an ad on TV? How do you know what really drove the sale?

Modern advertisers now track multiple interactions along the customer journey and assign attribution scores based on engagement and deep learning models. The key is making sure you can track the same customer across all these touchpoints over time.

With AI and better probabilistic models, advertising platforms are finally solving the attribution problem. Meta, Google, and AppLovin are leading this shift.

By tying advertising directly to actual sales outcomes rather than just clicks, this increases what advertisers are willing to pay per ad. They'll pay premiums for ads that demonstrably drive revenue, for outcomes over clicks. This is where AppLovin's background gives them an advantage, mobile games were forced to solve this attribution problem years ago. You can't rely on last-click when users might see an ad in one game, then download your game hours later. Mobile ad platforms like AppLovin pioneered user-attribution models out of necessity, giving them a head start in the outcome-based advertising world that's now emerging across all channels.

The winner in all this will be someone who can coordinate data across the different platforms from open web to CTV to social media.

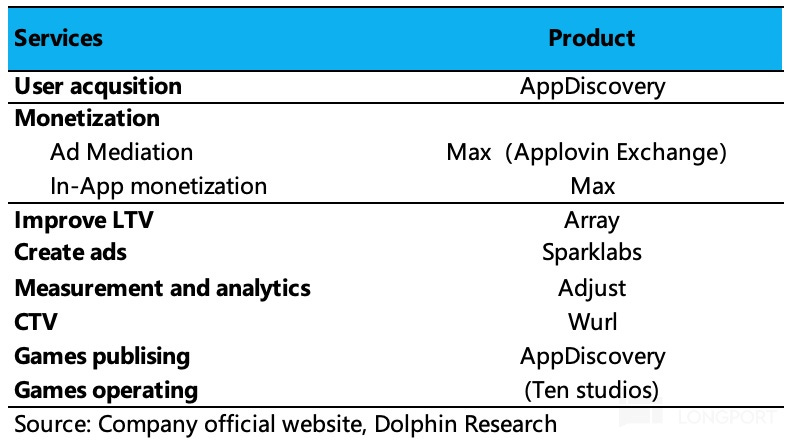

AppLovin's management understands this and has assembled a full-stack ad platform through strategic acquisitions over the past few years.

In doing so, AppLovin is in the process of of building a vertical ecosystem that can compete with Meta and Google's integrated approach.

The missing piece is a walled garden of their own. AppLovin has submitted a bid for TikTok's US business, but that's not their only option. With a market cap of $120B, AppLovin could pursue other social platforms like Pinterest with smaller market caps to complete their ecosystem. Adding a social network would create another crucial touchpoint to improve ad effectiveness across their entire platform.

To sum it up:

AppLovin has developed a leading AI ad algorithm (Axon 2.0) that ranks behind only Meta and Google in effectiveness

The data sources and technical capabilities that built this algorithm create significant barriers for other competitors to replicate

They're building vertical integration spanning ad creation through deployment to reporting. This becomes more valuable as generative AI advances

Strategic acquisitions enabled horizontal expansion across ad markets from mobile games to web pixels and CTV

The market still isn’t sure if any of this is even real, creating opportunity.

Once you’ve figured this out, $120B MC is too evidently small for where this is going. For a company positioned to be the third major player in digital advertising during an era where AI is expanding the value of digital advertising. The 20% revenue growth estimates from analysts may prove to be too conservative.

Disclosure: I am long 150 shares of APP