CM # 3: It's time for LiDAR

The sub-$1B MC company at the center of the autonomous revolution?

What’s LiDAR anyways?

If you have been in San Francisco or Austin recently, you have seen those Waymos going around with a big spinny thing on top. What that sensor is a LiDAR system.

LiDAR is a system that uses lasers to detect objects. A laser will keep going in a straight line until it hits an object. When it hits the object, the laser will actually bounce back to the source (at a lower magnitude). You can use this to figure out an object’s distance from the source:

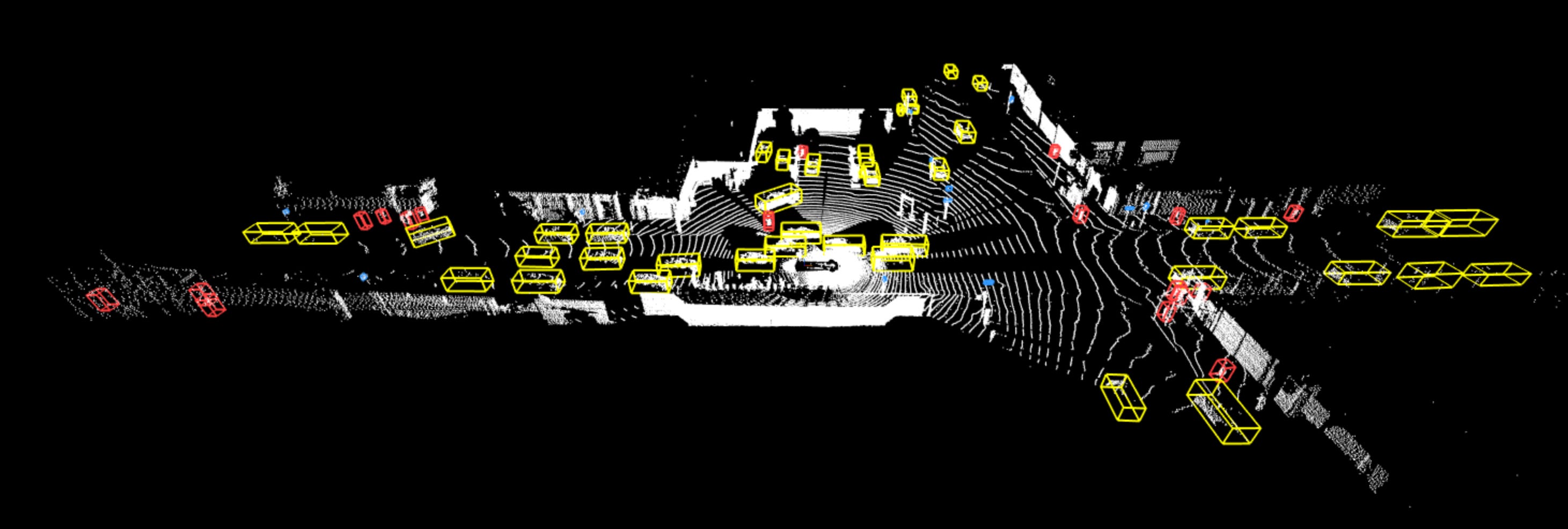

A Waymo maps its surroundings with a bunch of lasers rotating very quickly. This allows it to create a map that will look something like this:

In doing so, Waymo can quickly detect nearby pedestrians and vehicles. Waymo uses its own proprietary sensors, but let’s say you wanted to play LiDAR in the public markets.

There’s three sensor-plays that aren’t penny stocks. HSAI is the global leader in this space, but it’s Chinese. AEVA is your next option, which has been meme’d 250%+ YTD based on an unnamed “top-10 passenger OEM” partnership. OUST is operating with named partners, including a top-10 OEM of its own (Hyundai) and a larger-scale business including industrial partners such as John Deere and Komatsu.

OUST went public via SPAC in 2021 at roughly $2B, crashed 80%, but has been firming up technically, including a recent breakout. So what’s the story and is there actual fundamental value beyond meme-potential?

Ouster Background

Ouster was founded in 2015 by a group of Stanford mechanical engineers, including founder-CEO Angus Pacala. In 2017, they raised a $27M series A, originally a 64-channel sensor that was 85% cheaper than its main competitor. Ouster took the opportunity to go public during the SPAC-boom in 2021 and used the proceeds to acquire Sense Photonics which also had an automotive focus.

In 2022, Ouster merged with Velodyne LiDAR. Velodyne was one of the first companies in the LiDAR space, tracing its history to a 2005 DARPA challenge. Velodyne had also gone public via SPAC, but had fallen 67% from IPO at the time vs. Ouster which had fallen 50%.

Business Momentum

Ouster has begun to gain momentum with a series of partnerships:

Announced within 2025:

An already existing partnership of note is Serve Robotics (SERV), which uses Ouster as its LiDAR provider.

Business Case

On paper, the economics do not look great today: however, there are starting to be signs of operating leverage. Revenue has grown from $83M to $118M from 2023 to 2024 while operating expenses went down from $187M to $148M. The business is operating at a healthy 40% gross margin. Ouster has pledged to maintain its 40% gross margin while keeping R&D and operating expense flat, allowing it to potentially grow its way out of its current loss structure.

What it’s really lacking is scale. If you think about 4,800 sensors on a quarterly basis, that’s not an industrial-scale business. Despite this, Ouster is still in an industry leadership position. As explained in a recent CEO interview: Ouster is the “largest provider of LiDAR technology in the Western world.” Ouster also has a moat in their custom silicon Chronos chip platform. However, to date Ouster has mainly provided sensors to R&D divisions and universities and has not been asked to deliver sensors at scale.

Even Waymo, the flagship LiDAR industry solution, isn’t operating at scale yet, with around 2000 vehicles worldwide. While not directly partnered with Waymo, Ouster does power the Google Maps street-view vehicles, which will be needed for continued Waymo expansion to new cities.

To value this, one could begin by penciling in growth in the individual business divisions: Komatsu/John Deere partnerships will drive incremental volume, a city larger than Chattanooga decides to go with a pedestrian-safe traffic grid (the state of Utah recently allocated a grant), SERV has done a few offerings to double its cash position to $200M so will likely deploy more robots. They have two robotaxi customers, Motional - a subsidiary of Hyundai and May Mobility- a smaller player with Toyota investments. You could have some upside from humanoid robotics, with platforms such as Unitree incorporating a small LiDAR sensor into their infrastructure.

All in all, that’s enough to keep Ouster growing at 30% moving forward. But you’re also dealing with high share dilution (~5% QoQ) and being years away from real profits. The real interesting investment case which the market hasn’t caught onto yet is defense.

The Next-Gen Defense Platform

In May, the army announced an “Army Transformation Initiative,” its new comprehensive strategy to create a “more lethal force.”

While still in its early days, the basic principles are

1. We live in a new age of warfare driven by autonomous warfare (as shown by the effectiveness of Drones in the Ukraine war)

2. The army should cancel current procurement programs for “outdated crewed attack aircraft such as the AH-64D, excess ground vehicles like the HMMWV”

3. The army should redeploy the budget from those canceled programs into “long-range missiles and modernized UAS into formations”

The implications of this strategy are still coming into view. Meta and Anduril recently announced a joint partnership project developing systems that provide “enhanced perception and intuitive control of autonomous platforms."

LiDAR is a core and undervalued component of next-gen warfare. It’s also one where the US is currently lagging behind China. As stated in a congressional report:

“U.S. and PRC forces are among the militaries using LiDAR to support autonomous navigation capabilities for uncrewed ground and aerial vehicles (UxV). LiDAR's precision and speed enable military-specific use. UxV equipped with LiDAR could be used to conduct battle damage assessment—an estimate of the physical and functional damage produced by an attack—removing the need for military personnel to be physically present and exposed on the battlefield. LiDAR-equipped UxV could be used to survey structural damage after natural disasters and to collect environmental data in remote or dangerous locations. The U.S. military has explored using LiDAR to identify and determine the depth of littoral sea mines and to conduct atmospheric monitoring to predict laser weapons' effectiveness. The U.S. Army says potential uses include "platform target identification, aim point selection, range instrumentation support, weapon defenses, and mapping."

There are several draft bills in congress to ban US defense departments from buying Chinese LiDAR solutions. Beyond obvious reasons, there was a specific incident where a “Chinese lidar manufacturer planned to transmit data culled from Estonian cars back to China.” If the US was to focus on a next-gen LiDAR strategy, it is unlikely they would turn to Chinese HESAI but instead pick the largest-US based LiDAR sensor manufacturer (Ouster).

While UAV drones can use infrared cameras for general strikes, LiDAR can come into play for other contexts. As explained by Northrop Grumman “A drone fitted with LIDAR technology could do all sorts of survey work, but it could also do something far more sensitive: fly into a dangerous urban environment, even a building interior inaccessible to GPS data, and give American troops a quick, real-time look at the layout, obstacles, and hazards.

In other words, the pivot to a Drone-First military will also become a pivot to a LiDAR-first military. There hasn’t yet been a provider selected at scale to fulfill this need. By scale alone, Ouster is likely on track to do this. Forterra, a $75M series B defense contractor partnered with Oshkosh, already uses Ouster sensors for autonomous military vehicles.

Ouster maintains a commitment to “not sell our products to adversaries of the United States or repressive regimes.” Ouster’s Gemini Software platform, a surveillance platform meant for “perimeter security, transportation safety systems, traffic signal control, retail and customer analytics, and logistics” also seems tailored-made to be a dual use software for border surveillance and military operations.

Bottom Line: At $500M enterprise value, you're getting the dominant Western LiDAR provider at the inflection point of multiple demand drivers. I believe LiDAR is likely to become more important in the market’s view than previously as the new defense strategy and “Physical AI” continue to gain relevance in the market narratives. The economics are not as bad as they seem with 40% gross margin on units sold, just operating at sub-scale. The upside allows for a speculative position.

Defense and smart cities imo. That's where the monopoly is.