CM #10: OpenAI is dead, long live the AI trade

why the AI data center trade can still survive without OpenAI

Welcome back to Caffeinated memos.

TeraWulf announced $9.5 billion in contracted revenue last week and the stock dropped 20%. Oracle gave back its entire OpenAI rally. OpenAI’s struggles have doomed the entire data center complex- or so markets think. With Nvidia earnings Wednesday, investors are asking: is the AI trade over?

Today we’re going to answer three questions: 1. Is OpenAI in trouble? 2. Does the DC Complex need OpenAI to survive? 3. What’s the best way to “buy the dip”?

1. Is OpenAI in trouble?

OpenAI spent most of September making blockbuster deals. 10GW from Nvidia. 6GW from AMD. 4.5GW from Oracle. An incremental $250B in Azure credits from Microsoft.

These deals led to a question on Brad Gerstner’s podcast:

“How can a company with $13 billion in revenues make $1.4 trillion of spend commitments?” to which Altman fumbled “We could sell your shares or anybody else’s”

OpenAI’s CFO in a WSJ interview asked for a “government backstop.” To make things worse, Microsoft made a financial disclosure in its 10Q, that it “lost $4.1B in other income (expense) respectively of net losses from investments in OpenAI.”

As Altman disclosed, OpenAI “expects to end this year above $20 billion in annualized revenue run rate” which implies they had less than $5B in revenue last quarter. And since OpenAI has a 20% rev share with Microsoft, in Q3 they had $5B+ in compute costs at Microsoft against $4B in revenue (that’s negative gross margins?)

These spend commitments are coming at the same time, OpenAI is giving up traffic share to other models including Gemini.

Since OpenAI is losing market share and is operating at negative GM’s, this raises legitimate questions for how sustainable OpenAI’s business model is.

Answer: YES, OpenAI is in trouble

2. Does the Data Center Complex need OpenAI to survive?

The market has decided that OpenAI’s health is important to the health of many stocks involved in the data center.

$CRWV is down 50% in the past few weeks. $CRWV 5-year credit default swaps are getting bid to ridiculous levels:

Crypto turned neocloud $IREN is down 35%+

Former Yandex subsidy turned AI cloud provider $NBIS is down 40%

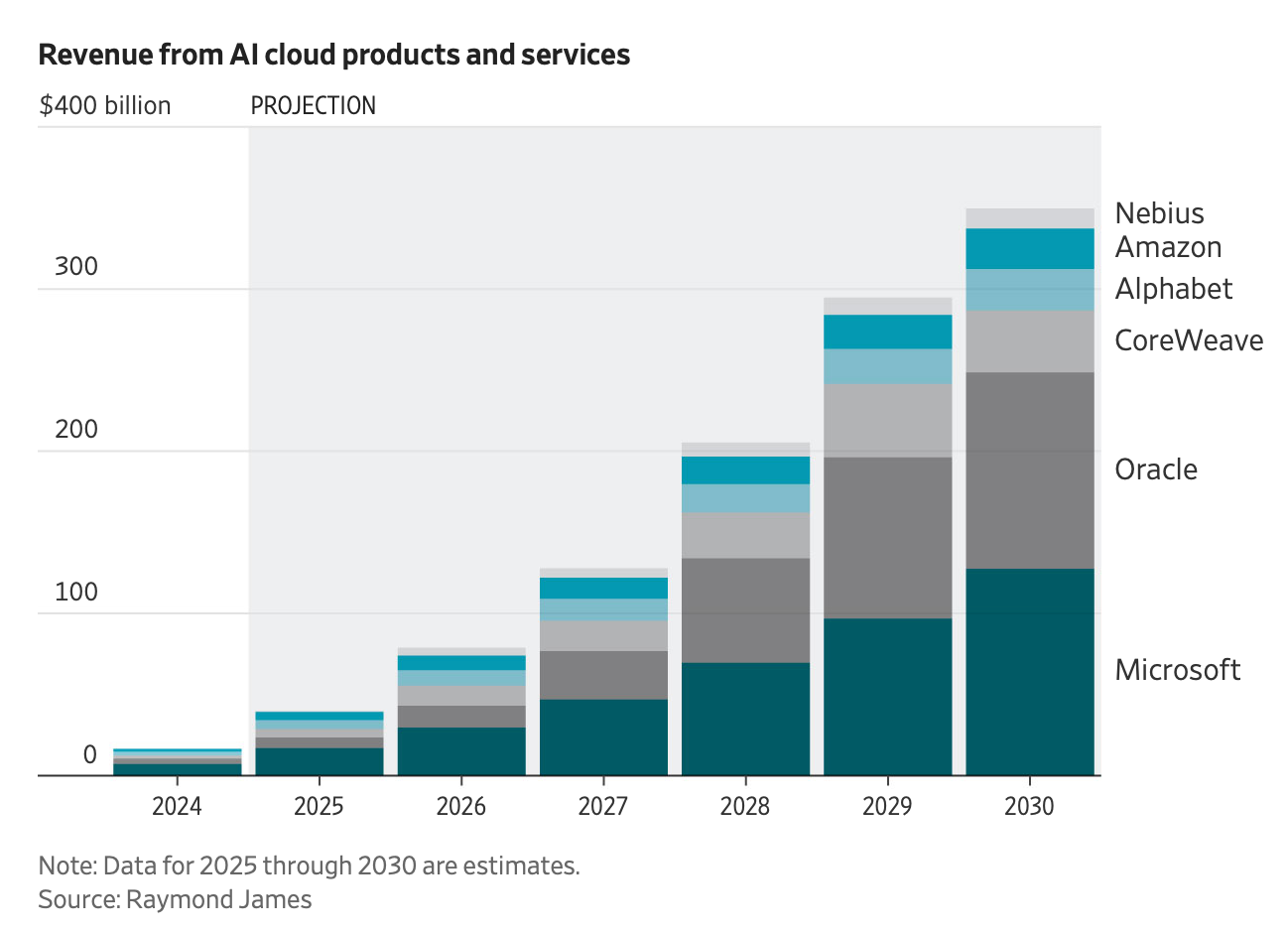

The market has decided if OpenAI is in trouble, the revenue projections from AI clouds have to be in question. There was a lot of revenue projected:

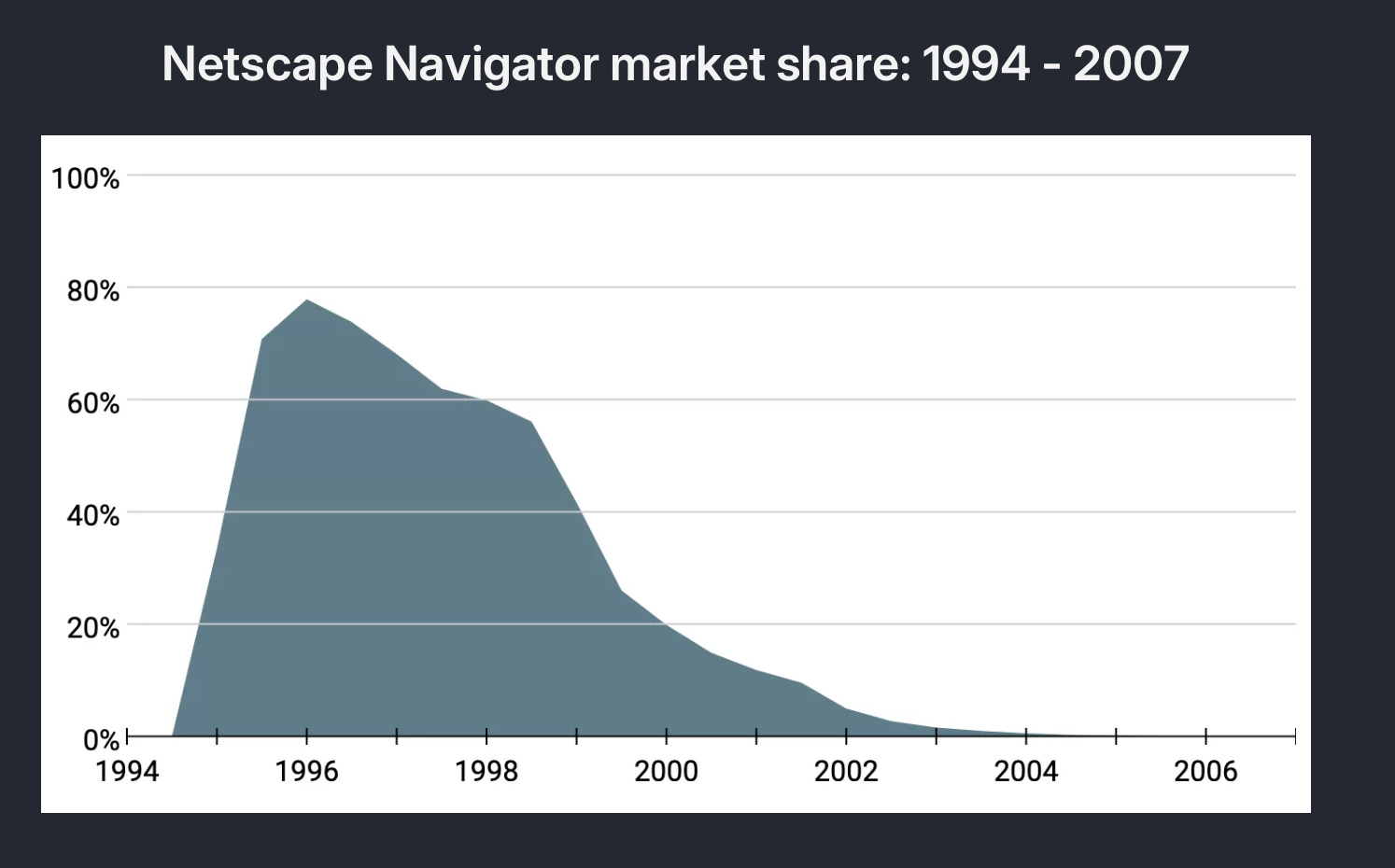

But is that simple? OpenAI could go bust in two years… and AI cloud revenues could move higher. The Netscape IPO famously marked the start of the dot-com bubble.

What’s often left out is Netscape underperformed after its IPO, eventually being sold to AOL in 1998. What happened to NetScape? Despite reaching 80% market share in early 1995, it bled users to competition including Microsoft’s Internet Explorer.

Did NetScape’s failure mean the internet was a fad? Would shorting the dot-com bubble based on NetScape’s 1997 economics have been a good idea?

It’s not obvious if OpenAI has the ideal business model for AI. OpenAI is optimizing for Meta-esque metrics from “time spent” to “weekly active users” and thinks ads will be an eventual path to profitability.

Anthropic believes corporate adoption can allow for higher gross margins. Satya Nadella believes that “grounding data” is the differentiator and will allow Microsoft to charge more for AI services. Zuckerberg believes it will simply come down to cash flow, and the company with the most cash to support AI will win.

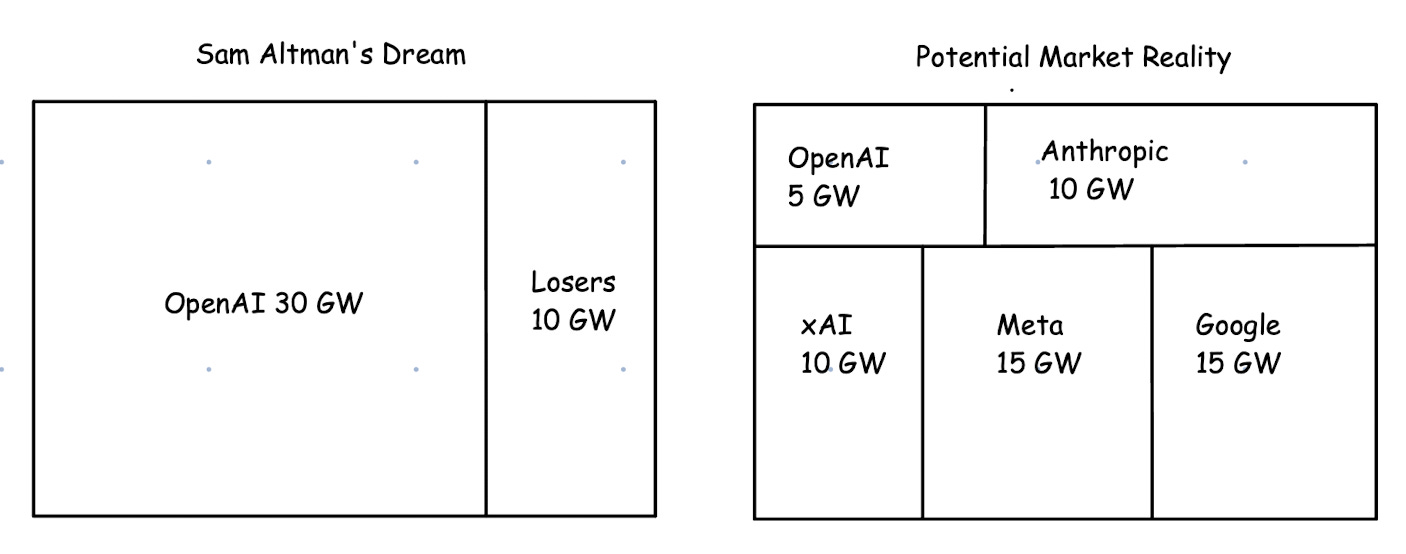

When looking at OpenAI’s compute needs, it’s worth remembering that Sam Altman is buying compute under the assumption OpenAI will be a monopoly (80% of AI traffic share). What if that isn’t the case? In a competition scenario, the total pie for compute can be larger, even if the largest compute consumer is smaller.

AI models are continuing to get better with scaling laws. As detailed before Gemini 3 is likely to be a step change over current models. Grok 5, which will be the first model powered by a 1GW data center is likely to be as good as Gemini 3.

Other 1GW data centers including Meta’s Prometheus, Amazon’s New Carlisle , and Microsoft’s Fairwater will all come online next year, powering further model advancements.

Another angle to Altman’s commitments was to convince competitors that OpenAI would spend so much it doesn’t make sense to compete.

OpenAI’s struggles are an invitation to competitors. Maybe OpenAI only is spending $300B over the next 8 years, not $1.4T. That means it’s possible to catch up to OpenAI in the near-term on compute.

In the past weeks, we’ve continued to see more, not less AI data center announcements. Anthropic announced $50B in AI infrastructure. Google $40B.

We are also finding more constraints on the data center buildout from memory, to hard drives, to power (gas turbines). This means completed/existing data centers are likely to be more valuable assets. Any data centers fully constructed by the end of 2026 should not go empty, whether OpenAI succeeds or fails.

Answer: NO, data centers are likely to remain in a shortage whether OpenAI succeeds or not

3. What’s the best way to buy the dip?

Given the market is making the misconception that OpenAI’s struggles mean that the entire economics for data centers are in question, how can one play this opportunity?

$ORCL: Oracle is one of the most straightforward ideas. Oracle went from $230 to $340 on OpenAI driven-RPOs, only to give it all back.

The market has not only written off the entire OpenAI contract (in which years 1-2 should still be funded) but assumes Oracle will never be able to lease the compute they’re building. One can take advantage of this pessimism and go long Oracle.

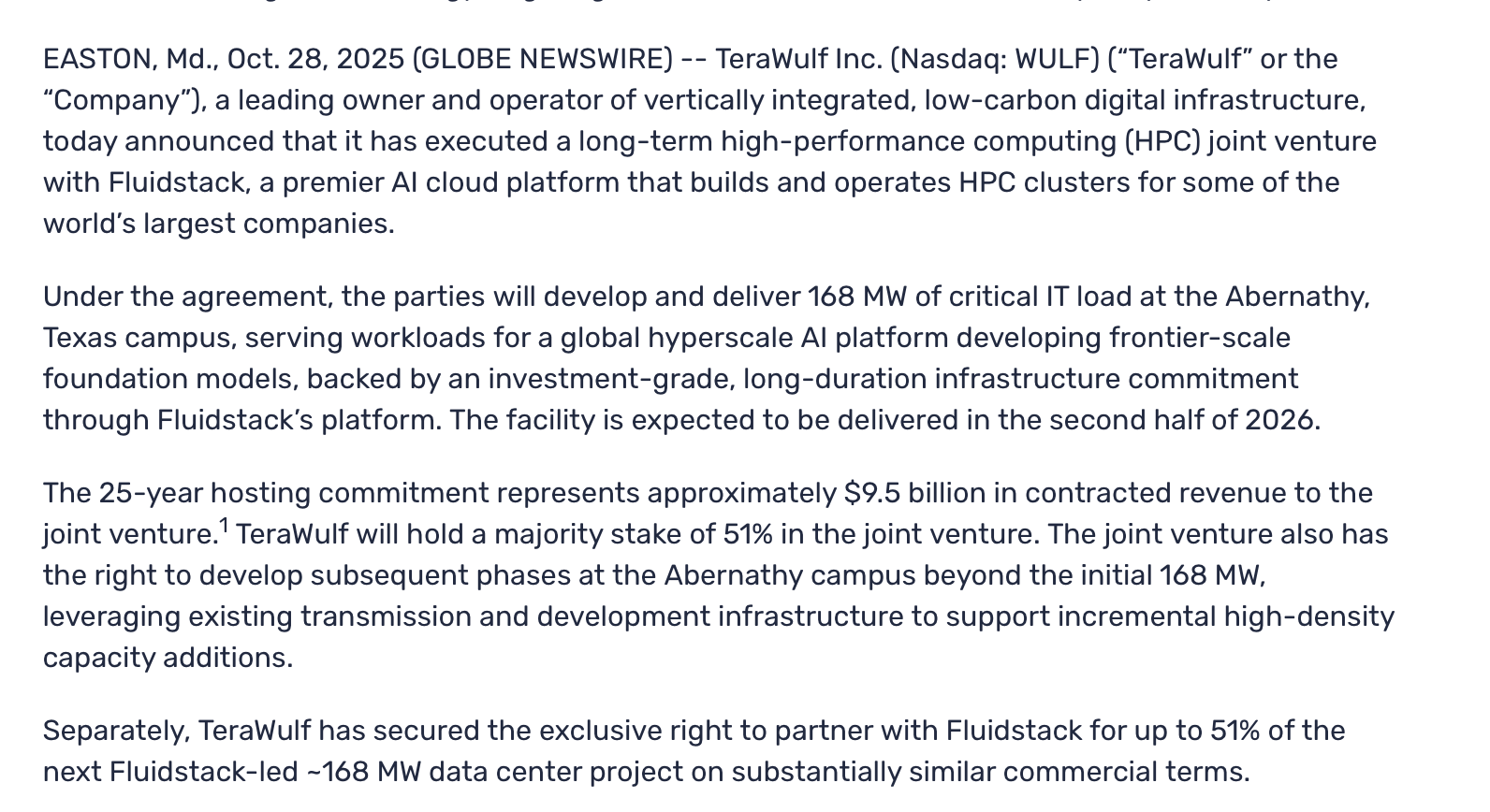

$WULF is one of the crypto miners that have done the AI pivot. TeraWulf is trading down to $11 from $17 only a few weeks ago.

Both the Google $40B and the Anthropic $50B announcements involve TeraWulf to some degree. Google’s is $40B focused in Texas. Anthropic’s $50B data center spend is through “Fluidstack in Texas and New York.” TeraWulf owns 51% of the Abernathy campus in Texas, which is one of the mega-projects tied to both announcements.

This is a 25 year commitment backstopped by Google. TeraWulf’s 51% share represents $4.8B in contracted revenue when $WULF has a $4.6B MC. Yet WULF is down 20% because the market conflated OpenAI’s struggles with the entire AI buildout. If these announcements came out a month ago, Terawulf would have been up 30%.

These are just a few of the clearest tech opportunities. There are likely more dislocations in the market in the data center space.

Good luck on holiday shopping- these discounts might not last!

Addendum: NetPower Update

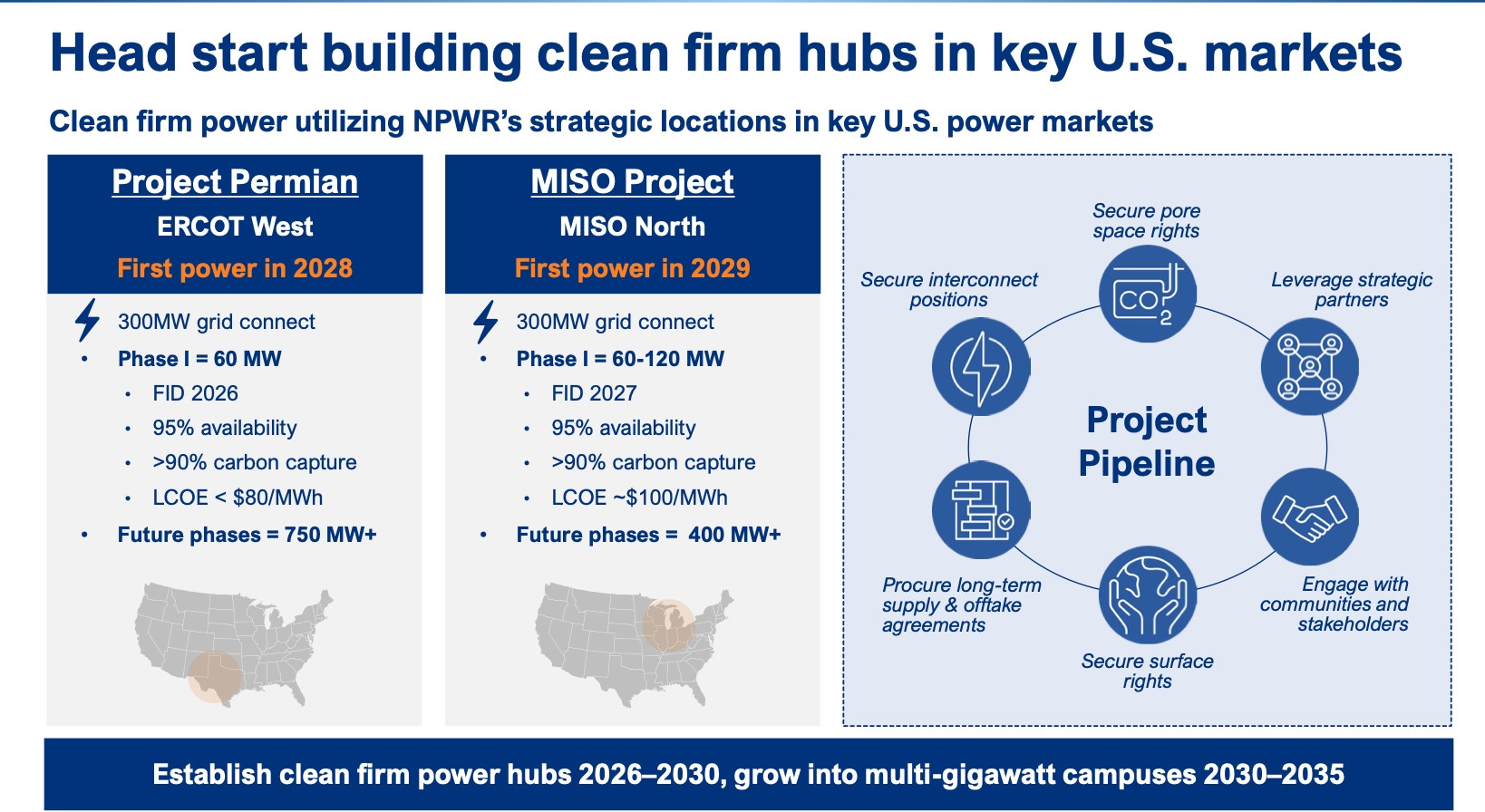

We had previously highlighted NetPower as a play on Texas natural gas demand, with its unique carbon capture technology and Project Permian buildout. NetPower in its Q3 earnings made a significant pivot, replacing its developmental Oxy-combustion technology with Entropy Inc.’s proven carbon capture system. While this changes the original thesis, the strategic rationale is sound:

Timeline: 2028 first power (vs 2030-2031 for oxy-combustion)

Capital efficiency: $75-90M equity from NPWR (vs $1.7B for original plan)

Execution risk: Entropy tech (operating since 2022) vs first-of-a-kind

Project financing: 50-70% debt vs 100% equity required

Danny Rice: “We can either keep our heads down and continue investing 100% of our capital to advance our oxy-combustion technology... or we can slow down that spending in order to free up some of our resources for near-term accretive opportunities. We strive to allocate our capital in a responsible manner that maximizes shareholder value.”

While “SPAC abandons breakthrough tech” is not an ideal headline, NetPower is trading at ~$250M EV net of cash, you’re paying almost nothing for two premium carbon capture sites, each with 300MW interconnects. Oxy has committed 30 MW + 100% CO2 offtake to the Permian phase 1 site with a second offtaker in advanced discussions for the remaining 30MW. The Midwest site is targeted at hyperscalers.

Disclosure: Author is long ORCL/WULF calls, and NPWR shares. Not investment advice - just ideas that seemed brilliant at 2am. Do your own research.