Caffeinated Memos: #13: Tesla is a short

While always an outlier on valuation, the SpaceX IPO creates a short-term window to short Tesla

Welcome back to Caffeinated Memos, the financial newsletter covering short-term catalysts under-appreciated by the market.

Today we’re making the argument that Tesla is a short, not just on valuation but with actionable catalysts within the next 6 months.

Tesla is one of the most successful stocks of the last decade and at every turn, Tesla has made a fool of shorts.

In 2017, Jim Chanos, who famously shorted Enron, said Tesla’s equity was “worth zero”.

In 2020, Tesla short sellers lost $40B betting against Tesla.

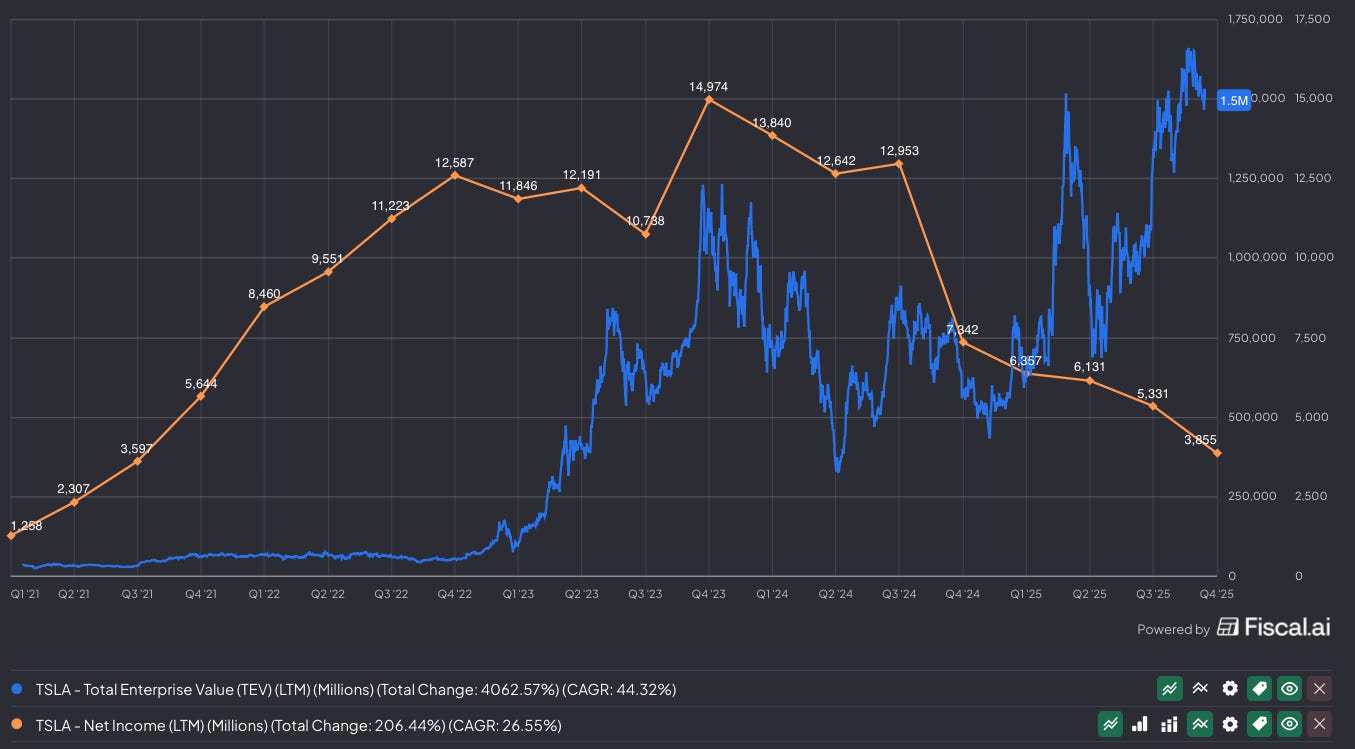

Yet Tesla has marched on to be the tenth most valuable company in the world, with a $1.5T market cap.

So why on earth, would I bother to bet against Tesla? Hasn’t enough brain power already been spent on this?

Every Tesla bear case has been a fundamentals argument… but Tesla has never traded on fundamentals. Here’s the catalyst that changes the narrative for Tesla.

SpaceX is aiming to IPO at $1.75T MC, bigger than Tesla today. Sources have told Reuters that “an IPO was likely in June.”

The SpaceX IPO will create an alternative way to bet on Elon at a company more centered on his long-time ambitions of Space and AI. The IPO will draw funds away from Tesla at a time Tesla is facing a revenue decline with a robotaxi program crashing 4x more often than human drivers.

Part 1: The Core Auto Business is Shrinking

Tesla is an outlier. It trades at one of the highest forward PEs of any company in the S&P 500. It’s priced for growth… only it’s not growing.

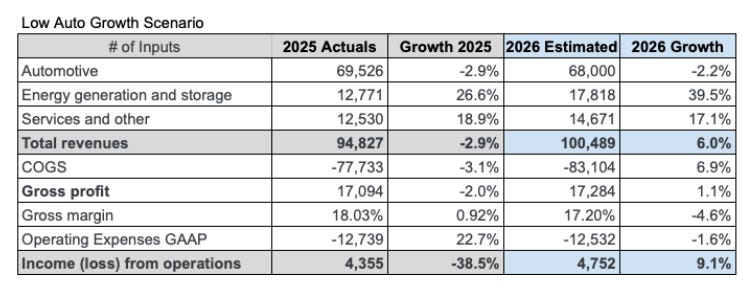

From last quarter’s earnings: revenue for 2025 was $94.8B vs $97.7B in 2024

(-3 YoY%), Q4 deliveries were down -16% YoY.

Tesla is struggling to grow revenue despite attempts by Tesla to discount. Tesla which once had an operating margin of 19% has seen that shrink to 5.7%.

The evidence is since earnings Tesla’s auto sales trend has gotten worse, not better.

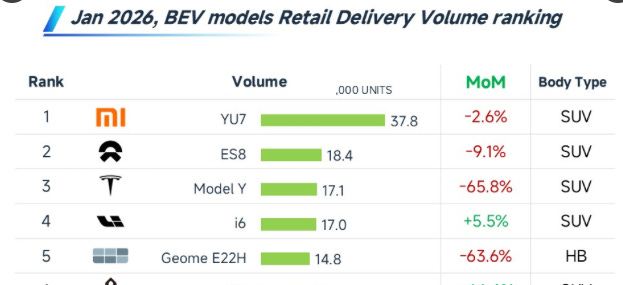

China, domestic retail sales are down 45% YoY the lowest monthly figure since November 2022. China, Tesla faces increased competition in a highly sophisticated EV landscape. Xiaomi’s YU7 outsold Model Y 2:1 in January at the same $35,000 (USD) starting price.

In the US, January registrations are down 17% YoY. Tesla had pulled forward demand with the $7,500 EV tax credit last year.

In Europe, registrations are down 17% YoY, the 13th consecutive month of sales declines amid Musk’s entrance into politics and increased competition from BYD whose registrations were up 165% YoY in January. BYD is doubling its sales outlets in Europe. BYD’s Atto 2 Boost plug-in hybrid is now selling in Germany at a discounted price of €16,000.

This isn’t a cyclical trough. Tesla is losing on product in China (YU7), price in US (no tax credit), and brand in Europe (13 consecutive months of EU declines). Instead of reinvigorating its lineup, Tesla is retreating, ending Model S and X production.

Part 2: Robotaxi at Risk as Waymo Accelerates

One of the Tesla bull cases has always been that Tesla will be the leader in self-driving cars. Tesla launched its Robotaxi service in Austin in June 2025. Tesla currently has an active fleet of 45 vehicles. Elon claimed last year Tesla would be at 500. What’s the delay?

Tesla’s Robotaxis have already been in 14 car crashes! This is in a best case scenario: small fleet, in Tesla’s HQ, most of those miles with a safety driver in the car.

From Fortune’s coverage on this:

“Tesla states that the average American driver (of a Tesla) is involved in a minor collision every 229,000 miles, meaning in the estimated 800,000 miles Tesla’s vehicles drove in Austin, the average human would have been involved in roughly four crashes, compared to the 14 involving Tesla robotaxis.”

Tesla claims it will launch in 7 additional cities in the 1H of 2026. One of those cities is San Francisco. Yet in California, Tesla hasn’t applied for a permit. The permit requires Tesla logging 50,000 miles of autonomous data. If Tesla was confident in its Robotaxi at this point, that shouldn’t be an issue.

While Tesla might scale robotaxi in 1H 2026, Waymo is pulling ahead in reality. Waymo is operating a fleet of 3,000 vehicles and had 127 million miles without a driver in 2025.

Waymo just raised $16B of funding in February and is expanding to 20+ additional cities in 2026. Waymo is only going to get more prominent in the next six months while Tesla continues to work through its Robotaxi struggles.

Part 3: Tesla Needs More Capex for its Ambitions

Robots have similar dynamics to electric vehicles- Tesla will once again have to fend off Chinese competition, only this time with no head start. China is going “all-in” on Robotics with over 140 startups and more than $26B state funding per the WSJ. Robots are already in a price war, with Unitree selling commercial humanoids for $29,000: less than a car.

Like Elon’s other timelines, Optimus keeps slipping. Elon has already set this up on the Q4 earnings call: “We are replacing the S/X line in Fremont with a 1 million unit per year line of Optimus […] and there's 10,000 things that need to go right, it's, you know, it only takes one to be slow to lag that.”

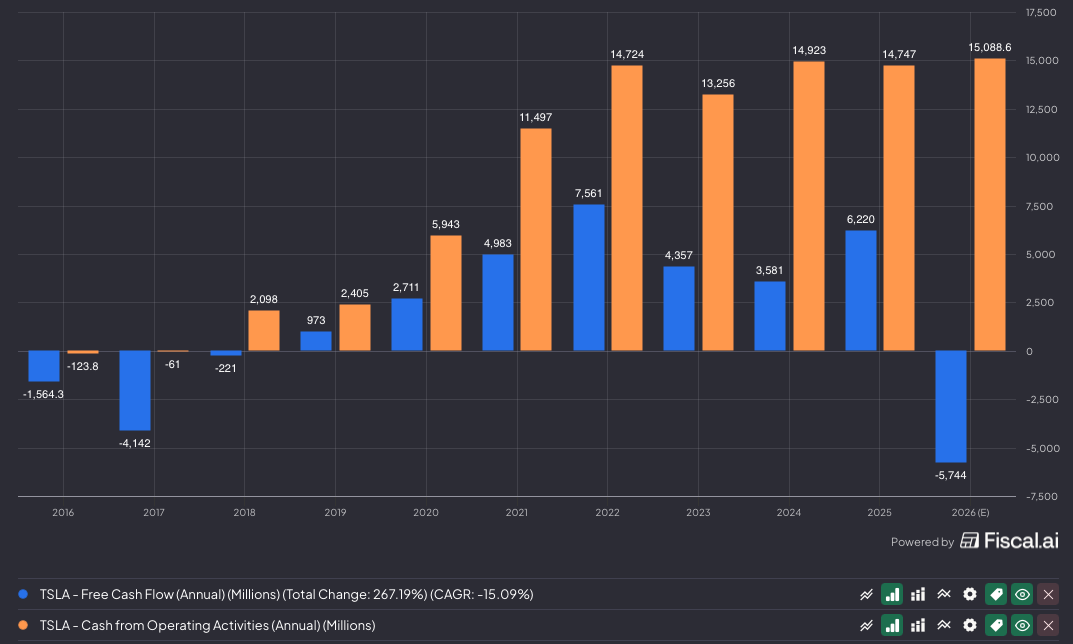

While Tesla has a long-term ambition to scale to 1,000,000 Robotaxis and 1,000,000 Optimus robots (and built into Elon’s incentives), scaling production is also expensive. Tesla is doubling capex to $20B in 2026. Tesla is set to go FCF negative this year, for the first time since 2017.

The one bright spot in Tesla’s operating picture has been energy ($13B revenue up 26% YoY). This was not enough to offset the sales decline in auto.

While utility scale solar (Megapack) is a true opportunity tied to AI capex, the overall outlook for the energy segment is clouded by the end of the tax credit for residential solar (Powerwall). Tesla on Q4 earnings said it expects “margin compression from the increased low-cost competition, impacts to market from policy uncertainty, and the cost of tariffs.”

Part 4: The Elon Proxy Unwind

To recap so far:

Tesla’s valuation is inflated

Tesla’s fundamentals (revenue, margins) have been deteriorating

Tesla’s Robotaxi/Optimus behind schedule

None of this is new. Tesla bears have been making these arguments for years.

So what will be the catalyst that gets Tesla to close the gap? What makes the next six months a window of opportunity?

The Upcoming SpaceX IPO is a Negative Catalyst for Tesla Stock

SpaceX is likely to IPO this year. SpaceX entered a quiet period in December of last year. An internal company memo noted “it’s preparing for a possible public offering in 2026 that would be aimed at funding an “insane flight rate” for its developmental Starship rocket, artificial intelligence data centers in space and a base on the moon.”

Bloomberg reported last week “The Starbase, Texas-based firm expects to submit its draft IPO registration to the US Securities and Exchange Commission in March, the people said. Such a move would keep it on track for a June listing.”

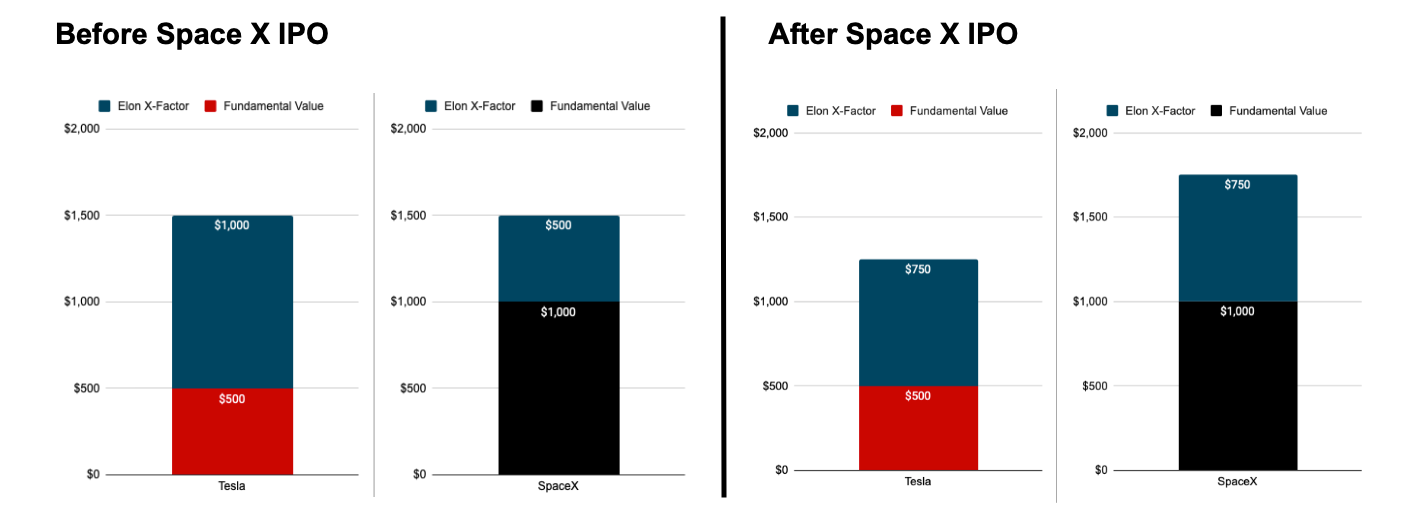

Why is this bearish for Tesla? Let’s start with a simple question: if Elon Musk was not the CEO of Tesla, what market cap would it trade at tomorrow?

Tesla earned ~$4B in net income last year. Even at 125x trailing earnings, a high multiple, Tesla would be worth $500B. A significant portion of its Market Cap is tied to Elon’s time, talent, and even his broader business empire helping Tesla. Let’s call this gap- Elon’s “X-Factor”- as $1T of Tesla’s valuation .

SpaceX wants to IPO at $1.75T, bigger than Tesla. The multiple is lower, but SpaceX earned only ~$8B in profit last year. SpaceX’s valuation also requires Elon’s time, talent, and broader efforts to justify it. There’s only one Elon. Where will he place his focus?

What will happen when SpaceX IPOs? A simple mental model: some of the Elon premium shifts out of Tesla into SpaceX. Tesla’s Market Cap drops from $1.5T to $1.25T (-20%) while SpaceX goes from $1.5T to $1.75T.

Where will Elon spend his time? This was part of the rationale for Elon’s new pay package: “Mr. Musk’s other ventures, including SpaceX, xAI, Neuralink and The Boring Company, which may start to seem more attractive as these other companies continue to drive innovation within their respective industries, including AI.”

The higher SpaceX’s valuation at IPO, the more of Elon’s “X-factor” it absorbs. After all if Elon said he would only spend 10% of his time at SpaceX, it would be hard for SpaceX to justify an IPO valuation at $1.75T.

A direct link is index flows. The Nasdaq is considering letting in mega IPOs (such as SpaceX) into the index, only 15 days after IPO.

Tesla has benefitted from being a top 5 weight in the QQQ from a flow perspective.

Under the fast IPO rules, SpaceX could IPO at $1.5T, trade to $2.5T after 15 days, and get a 5% share of QQQ. The 5% has to come from somewhere. While this would impact all components in QQQ, the other dynamics present, Tesla will be the most affected.

Elon’s pay package will give him an extra 12% of Tesla stock ($1T) if Tesla goes to $8.5T, for a total of 25% ownership and 25% voting control. Sounds like plenty of motivation- except Elon owns 42% of SpaceX today and 79% of voting control! $1T is great but if SpaceX went to $8.5T instead, he’d make $3T!

This also creates dynamics for retail investors to shift flows from Tesla. A retail investor could be more bullish on Elon than Tesla (the car company). Retail investors love space, they love names with defense exposure, and they love AI. The logical answer is at the margin, a significant portion of Tesla’s retail base will switch names if SpaceX and Tesla have the same MC.

Over time, Elon is financially incentivized to prioritize the combined SpaceX/xAI entity, even if at Tesla’s expense. Take Optimus production. Elon has told xAI investors, xAI can “eventually power humanoid robots like Optimus.” If Tesla is selling the robotic body one-time for at/near-cost (5% margins) and xAI is receiving the monthly subscription revenue for the brain, that is not a great scenario for Tesla shareholders.

This is not an outlandish scenario. Elon in the past has moved employees between his various companies and done intra-company deals (Tesla sold $430M in Megapacks) to xAI. This is only about to get worse as SpaceX IPOs and Elon is incentivized to support SpaceX’s price through any lockup period.

Part 5: Price Target + Risks

Tesla has outperformed the Nasdaq by 15% over the last 6 months. There is not a good reason for this. Tesla ran up into good Q3 earnings (+12% rev YoY), but Q4 (-3% YoY) made it clear that Q3 involved significant demand pull-forward.

While Analysts are projecting 8.5% (consensus) revenue growth in 2026, this requires some unlikely assumptions, including ~3% auto sales growth, against last year, which included the expiring tax credit and Model S/X still in the lineup.

If auto sales fall 2% while keeping other analyst assumptions, Tesla’s revenue grows only 6% vs. 8.5% consensus.

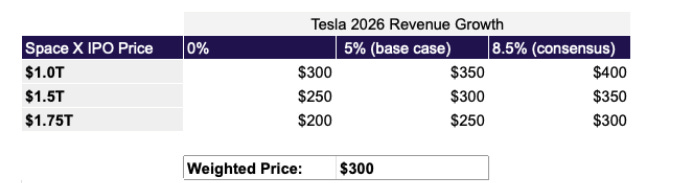

Combined with the SpaceX catalyst, the base case is roughly 30% downside to $300 a share over the next 6 months. One would expect the repricing to begin when SpaceX files in March, ahead of the actual IPO date.

This is in line with where Tesla traded in the 1H of last year. It is becoming clear that the acceleration in the 2H of last year was tied to a tax credit pull forward and the stock price has yet to reflect the deterioration in fundamentals and narrative.

Risks and considerations:

SpaceX IPO moved to 2027: removes immediate downside catalyst

SpaceX IPO does not play out as expected: broader Musk sentiment improves into the IPO (aiding Tesla)

Musk hits a timeline (either on Robotaxi scaling, Optimus production, etc.)

Tesla surprises to the upside on energy

How to short: Tesla’s cost to borrow is low as a highly liquid megacap. Puts are not recommended as Tesla has a high implied volatility. Neither is inverse ETFs (TSLQ). Inverse ETFs are trading instruments and are not designed to be held over time (decay is built-in).

Disclosure: Author is short TSLA shares. Not investment advice - just ideas that seemed brilliant at 2am. Do your own research.